Relying on inheritance to fund retirement is risky as it can’t be guaranteed

Starting early with small, regular pension contributions can help you benefit long-term compounding

Take advantage of employer contributions, combine pension pots and maximise tax relief

Retirement can seem an age away when you’re in your twenties and thirties, but it’s never too soon to start saving for the future. The earlier you start, the bigger the pot when you retire.

Inheritance – no longer a sure bet

Around a quarter of Gen Z and Millennials aren’t thinking about how they will fund their retirement because they expect to inherit money or property in the future, according to recent data1. With higher care costs, longer lifespans, frozen tax thresholds and changing Inheritance Tax rules, this could prove a risky strategy. The timing and value of an inheritance can’t be guaranteed, which could result in a big financial black hole later in life.

Saving doesn’t have to be taxing

Even if you are saving for other big life events, such as buying a new home, see if you can put aside a dedicated amount every month for your pension. Regular contributions over a long period of time soon add up and can benefit from growth over the years to retirement. These regular contributions can be topped up with lump sum payments over the years, such as bonuses. And don’t forget the government’s role – each contribution you make, currently up to 100% of earnings and within the £60,000 Annual Allowance, benefits from tax relief, boosting your savings straight away.

Make your pension work harder

Remember to:

Start early – small, regular contributions benefit long-term from compounding

Max out employer pensions and contributions to boost pension savings

Think about combining small pension pots from previous jobs for easier tracking and potential cost savings

Pensions are long-term investments – don’t panic over short-term dips in performance.

The message is – don’t rely on anyone else to fund your retirement – nothing is guaranteed.

1Standard Life, 2025

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

In a Pre-Budget speech,the Chancellor positioned her fiscal decisions as necessary in light of the UK’s current economic challenges

The Renters’ Rights Bill has received Royal Assent, which is set to change the rights of 11 million private tenants in England

President Trump and Chinese President XI Jinping met in South Korea to discuss ongoing trade tensions

“Each of us must do our bit for the security of our country and the brightness of its future”

Chancellor Rachel Reeves took to the Downing Street podium on Tuesday morning, in a rare pre-Budget speech, during which she said that she would do what is necessary, not popular, to protect the country against high interest rates and inflation.

With the Budget fast approaching on 26 November, while the Chancellor did not announce any spending commitments or specific tax rises during her speech, she did caution of the “challenges” facing the economy.

As speculation intensifies over the likelihood of manifesto tax pledges being broken, Reeves commented, “If we are to build the future of Britain together, we will all have to contribute to that effort. Each of us must do our bit for the security of our country and the brightness of its future.”

The Chancellor positioned the upcoming Budget decisions as necessary in light of the UK’s current economic challenges. She acknowledged that inflation has been slow to fall and productivity is weaker than expected, issues she said were inherited from the previous Conservative government. Rejecting “short-term sticking plaster solutions,” Reeves stressed her commitment to honesty and realism, saying she must “face the world as it is, not as I want it to be.”

She reaffirmed her focus on priorities that she feels matter most to the British people, including reducing national debt, cutting NHS waiting lists and easing the cost of living. Reeves intends that her Budget would drive sustainable growth while keeping “fairness at its heart.”

The influential think tank the Resolution Foundation, released a briefing note on Tuesday morning entitled ‘Black holes and consolidations’ – previewing key Budget decisions, saying tax rises are ‘inevitable.’

They recommend that the Chancellor should focus on not just filling ‘the fiscal ‘black hole’, but to take steps to boost financial-market confidence by doubling the level of headroom held against her fiscal rules to £20bn or at least increasing it to £15bn.’

“An important milestone for the private rented sector”

Last week, the Renters’ Rights Bill received Royal Assent, which is set to change the rights of 11 million private tenants in England. The reforms are expected to take effect over the course of 2026, but the government will confirm details of the roll out in the coming weeks.

A key element of the bill is the long-awaited abolition of Section 21 ‘no fault’ evictions. Landlords will now have to provide a valid reason if they wish to terminate a tenancy. This change is designed to give renters greater security, enabling them to challenge poor housing conditions or unfair rent increases without fear of eviction.

Additionally, all fixed-term contracts will become open-ended, following in the footsteps of Scotland, where this rule was introduced in 2017. Landlords who wish to increase rent will now need to serve a statutory notice, instead of creating a new fixed-term tenancy with a higher amount.

The Bill also tackles rental bidding wars, an increasing common trend in which prospective tenants offer more than the advertised rent to secure a property. Under the new rules, landlords will be prohibited from accepting higher offers, thus helping to control how rents are set.

Chief Executive of the National Residential Landlords Association (NLRA), Ben Beadle, commented, “After years of debate and uncertainty, today marks an important milestone for the private rented sector.” He added, “This is the most significant shake-up of the rental market in almost 40 years, and it is imperative that the new systems work for both tenants and responsible landlords.”

US meets with China

President Trump and Chinese President XI Jinping met in South Korea last week to discuss the ongoing trade tensions between the two nations. As a result, China agreed to suspend its control measures on rare earths, which are essential materials for the US manufacturing industry. In return, the US will reduce some of the tariffs it placed on Chinese goods entering the US. Also, China will immediately start buying large amounts of soybeans, an announcement that is likely to please US farmers who were hit hard by the trade dispute. However, nothing has been committed to paper yet and it may take some time before a formal deal is signed between China and the US.

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (5 November 2025)

Buyers can be swayed by seasonal features depending on when they’re buying

Winter buyers prioritise warmth, so would pay more for a fireplace and insulation

Summer buyers are drawn to gardens, pools and air conditioning when purchasing

Thinking of putting your home on the market? The time of year you do it could affect how well your property sells.

It’s all in the timing

It appears that buyers can be swayed by particular features depending on the season they’re purchasing in. A survey of 1,000 UK homeowners1 found that, in the winter months, 41% would pay more for energy-efficient features. Also, 38% would increase their budget for a traditional fireplace and a quarter (26%) would be convinced by a kitchen with an AGA-style cooker.

A similar trend occurs in summer, with nearly half (49%) saying they would pay more for a home with a garden or air conditioning. The same proportion (48%) would be swayed by a property with a swimming pool during the hot weather.

The desirable winter features

So, as we prepare for winter, which cosy features could contribute the most value to your home? A fireplace is the most sought after, increasing a property’s value by an average of £4,568. This is closely followed by good insulation (£4,356) and underfloor heating (£3,985), showing that warmth takes priority for winter buyers.

1Zoopla, 2025

As a mortgage is secured against your home or property, it could be repossessed if you do not keep up mortgage repayments.

Many UK investors use social media to help make their financial decisions

To protect investors from misleading advice, the FCA is taking decisive action

Professional guidance helps investors make safe, informed decisions and avoid costly mistakes

Social media finfluencers. Internet searches. AI chatbots. A growing number of people in the UK are turning to unregulated – and often unreliable – sources for financial advice.

A recent study1 revealed that 40% of UK investors used social media to inform their financial decisions in the last two years, with 12% specifically turning to finfluencers – or financial influencers – who post on Instagram, Facebook and TikTok.

To protect investors from misleading advice, the Financial Conduct Authority (FCA) is taking decisive action. Last year, it suspended, removed or blocked more than 1,600 websites suspected of promoting financial services without permission.

The regulator has also collaborated with tech giants, such as Google and Apple, to remove more than 50 financial scam apps in a bid to tackle fraud.

Avoid making an expensive mistake

The FCA crackdown targeted authorised firms too, with nearly 20,000 non-compliant financial promotions being amended or withdrawn in 2024 alone, compared with fewer than 600 in 2021. For some, however, the action has come too late. More than half of adults who have made financial decisions based on social media advice have lost money, according to data from one UK bank2.

Scammers now impersonating the FCA

In the first half of the year, the FCA have received 4,465 reports of fraudsters impersonating the regulator, with 480 of the victims losing money3. The advice is clear – be suspicious of unsolicited calls, texts, emails or offers. The FCA would not ask people to send money, bank account details,

passwords or PIN numbers and does not use WhatsApp, other messaging services or automated calls to contact people.

Stay safe, stay informed

With so much unregulated content, advice online and sophisticated scams, even experienced investors can be caught out. You need to be on your guard. We’re here to guide you through and help you make professionally advised, confident, informed choices to benefit, not jeopardise your financial future.

1Fidelity International, 2025, 2TSB, July 2025, 3FCA, 2025

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

UK GDP edged up 0.1% in August, supported by stronger manufacturing output and improving private sector confidence

Inflation held steady at 3.8%, fuelling expectations of another potential interest rate cut by year-end

Global equities rose as US tech earnings impressed and a US-China trade truce boosted market optimism

UK economy returns to growth

Figures published last month by the Office for National Statistics (ONS) showed the UK economy grew slightly in August, while survey data points to a more recent improvement in business conditions.

According to the latest monthly gross domestic product (GDP) statistics, UK output increased by 0.1% in August; this followed a 0.1% contraction in July. August’s principal driver of growth was the manufacturing sector – which expanded by 0.7% – while the larger services sector actually saw no growth at all during the month.

As monthly data can be volatile, ONS is increasingly focusing on growth over a three-month rolling period and, on this measure, the latest figures showed the economy grew by 0.3% in the three months to August. This represents a slight improvement on a growth rate of 0.2% recorded across the previous three-month period.

While the latest GDP figures showed that growth over the summer was relatively modest, new forecasts released last month by the International Monetary Fund (IMF) suggest the UK economy is still likely to outperform most of its peers this year. Indeed, the IMF’s updated projections point to an annual growth rate of 1.3%, which would position the UK as the second-fastest-growing of the world’s most advanced economies in 2025.

The latest evidence from a closely-watched economic survey also provided encouraging news in relation to private sector output, with the preliminary headline growth indicator from the S&P Global UK Purchasing Managers’ Index (PMI) rising to 51.1 in October; this figure was up from 50.1 in September.

Commenting on the findings, S&P Global Market Intelligence’s Chief Business Economist Chris Williamson said October’s data brings hope that “business conditions are starting to improve.” He added, “Output has picked up, with a particularly welcome return to growth for manufacturing, accompanied by an upturn in demand for services, notably among consumers.”

Inflation unexpectedly holds steady

The latest batch of consumer price statistics revealed the UK headline rate of inflation remained stable in September, raising the chances of another interest rate cut within the next few months.

Figures published by ONS showed the Consumer Prices Index (CPI) 12-month rate – which compares prices in the current month with the same period a year earlier – remained unchanged at 3.8% in September. This reading surprised most economists with the consensus view from a Reuters poll predicting the rate would hit 4.0%.

ONS said the largest upward inflation drivers were petrol prices and airfares, while these were offset by lower prices for a range of recreational and cultural purchases including live events. Food and non-alcoholic drinks inflation also eased during September, with prices in this sector actually posting a monthly fall for the first time since May 2024.

Expectations that the Bank of England (BoE) might sanction another reduction in interest rates rose immediately after release of the inflation data. Indeed, markets moved to price in a 75% probability of rates being cut once more by December, a notable jump from a 46% chance before the CPI figure had been released.

Investor expectations, however, did ease back towards the end of last month. The IMF also warned the BoE to be ‘very cautious’ about future rate cuts after publishing its updated economic forecast which predicts the UK will have the highest inflation rate amongst the world’s most advanced economies both this year and next.

A recent Reuters poll also found that a slight majority of economists now expect to see no further rate reductions this year, although a majority are predicting two further cuts by the middle of 2026. The Bank’s interest-rate setting committee has two more meetings scheduled this year, with its next decision due to be announced on 6 November.

Markets

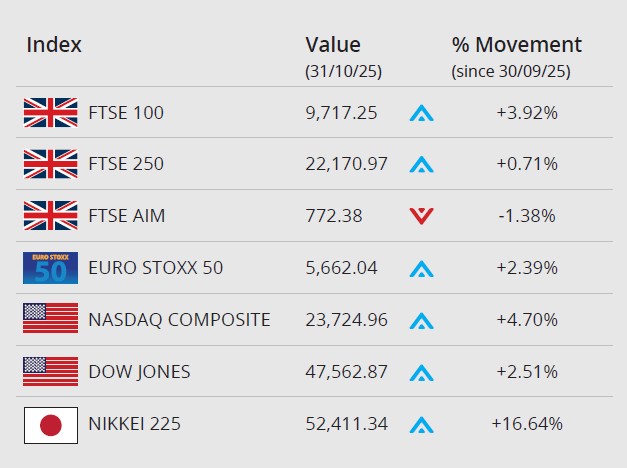

As October drew to a close, tech stocks pushed Wall Street higher as investors embraced strong earnings from some of the ‘Magnificent Seven,’ including Amazon, which helped rekindle optimism for tech mega cap growth.

Relief to businesses and consumers came at month end on the news of a one-year trade truce between the US and China, resulting in lower tariffs and export controls. The Dow Jones closed October on 47,562.87, an increase of 2.51% in the month. The tech-focused NASDAQ closed the month up 4.70% on 23,724.96.

In the UK, the FTSE 100 closed October on 9,717.25, a gain of 3.92%. The mid-cap FTSE 250 gained 0.71% in the month to end on 22,170.97, while the FTSE AIM recorded a 1.38% loss to close October on 772.38. On the continent the Euro Stoxx 50 gained 2.39% during the month to close on 5,662.04. In Japan, the Nikkei 225 gained 16.64% to close the month on 52,411.34, reaching record highs towards month end as investors welcomed the truce between Washington and Beijing.

On the foreign exchanges, the euro closed the month at €1.13 against sterling. The US dollar closed at $1.31 against sterling and at $1.15 against the euro.

Brent Crude closed October at around $64 a barrel, recording a loss of 3.57% in the month. The oil price dipped at month end, ahead of an anticipated increase in output by OPEC and its allies (OPEC+). The gold price rose 3.59% during the month, closing at around $4,009 a troy ounce.

Chancellor facing Budget challenge

Pressure on the Chancellor ahead of the Autumn Budget increased last month, following publication of the latest public finance statistics and a potentially larger-than-expected downgrade to productivity forecasts.

Data released by ONS revealed that government borrowing in September totalled £20.2bn; this was £1.6bn more than the same month last year and the highest September figure since 2020. It left cumulative borrowing across the first six months of the financial year £7.2bn above the monthly profile consistent with the latest Office for Budget Responsibility (OBR) forecast produced in March.

The OBR is currently working on an updated forecast to be unveiled alongside the Budget on 26 November, and last month saw intense speculation that a key productivity forecast will be cut by more than previously expected. While accurately estimating the size of the hit from this potential downgrade is difficult, analysts suggest it could put a £20bn hole in the public finances.

Earlier in the month, the Institute for Fiscal Studies (IFS) also said there was a ‘strong case’ for the Chancellor to increase the amount of fiscal headroom she has built into the system. This, the IFS argues, would bring greater stability and avoid the Chancellor ‘limping from one forecast to the next.’

Retail sales grow for fourth month in a row

Last month’s official retail sales data revealed that volumes rose for a fourth consecutive month, while the latest GfK confidence figures suggest consumer sentiment now stands at its joint-highest level in over a year.

ONS statistics showed that total retail sales volumes rose by 0.5% in September, defying analysts’ expectations of a 0.2% monthly fall. This growth was largely driven by sales of new tech gadgets, including Apple’s iPhone 17 and strong demand for gold from online jewellers. Across the third quarter as a whole, the data release reported sales growth of 0.9%, a notable acceleration from 0.2% in the second quarter.

October’s GfK consumer confidence survey also delivered positive news, with its headline index rising to -17 from -19 in September; this metric was last higher in August 2024. GfK said the rise was primarily driven by a four-point jump in the ‘major purchase’ component, which was boosted by an Amazon Prime sales event and competing offers from other retailers.

The data did, however, show that consumers’ views of their own finances in the year ahead worsened, with GfK noting that consumers and retailers will both be closely watching the Budget for any potential impact on spending ahead of the crucial Black Friday weekend sales.

All details are correct at the time of writing (03 November 2025)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from, taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.

UK inflation holds steady at 3.8%, with food prices easing for the first time since May 2024

Inheritance Tax receipts climb again, with forecasts suggesting record highs by the end of the decade

Consumer confidence rises slightly as shoppers prepare for Black Friday and await the Chancellor’s upcoming Budget

“The Chancellor must use the upcoming Budget to tackle rising prices head on”

The latest inflation figures from the Office for National Statistics (ONS) show that the UKConsumer Prices Index (CPI) rose by 3.8% in the 12 months to September, a lower figure than a Reuters poll of economists had expected (4%) and unchanged from August and July.

Prices are still rising compared with a year ago, but at a slower rate. On a monthly basis, the cost of food and non-alcoholic drinks dipped to 4.5% in September, from 5.1% in August, the first decline since May 2024. Lower prices of bread, vegetables, dairy products, cereals, fish and soft drinks contributed to the decline. ONS said the fall was attributed to increased discounting and promotional activity by retailers.

According to ONS Chief Economist Grant Fitzner, the prime upward contributors came from airfares and petrol prices, this was “partly offset by lower prices for a range of recreational and cultural goods, including live events.” He added that although food prices are still “running high,” the dip is “a little encouraging.”

Still much higher than the Bank of England’s 2% target, Rachel Reeves said last week she was “not satisfied with the numbers.” While, looking ahead to the Budget on 26 November, Dr Kris Hamer, Director of Insight at the British Retail Consortium, commented on the data,“With the IMF warning that UK inflation will be the highest in the G7, the Chancellor must use the upcoming Budget to tackle rising prices head on. Retailers, already operating on tight margins, have been hit with £7bn in additional taxes this year alone – costs they simply can’t absorb. The government must use what levers it has to hold back the rising tide of inflation. Reform of business rates – delivering a meaningful cut for retailers with no shop paying more – would drive and help deliver better value for customers.”

IHT receipts continue to tick higher

The latest data from HM Revenue & Customs shows Inheritance Tax (IHT) receipts continued climbing year-on-year. In the period between April and September 2025, IHT receipts totalled £4.4bn, around £100m more than during the same period in 2024, representing a 2.3% increase. If they continue at the current pace, total receipts for the 2025/26 tax year could reach around £8.8bn, setting yet another record. The Office for Budget Responsibility (OBR) forecasts that IHT revenues will potentially rise to £14bn by the end of the decade.

During the April to September period, gross tax and National Insurance Contributions (NICs) receipts totalled £438.6bn; a £32.1bn increase when compared to the same timeframe the year previously.

Consumer confidence on the up

In the latest reading of GfK’s Consumer Confidence Index, data shows a two-point increase in October, although still registering at minus 17.

The marginal increase in the month can be partially attributed to shoppers looking ahead to the Black Friday sales, despite caution around the Budget.

The rise was mainly driven by a four-point increase in the index’s major purchase measure – a key indicator of confidence in buying big-ticket items – to minus 12, nine points higher than last October. Over the next year, expectations for the general economic situation also improved by two points to minus 30, though this remains two points lower than a year ago. Meanwhile, the outlook for personal finances over the next year edged down one point to +3, still five points stronger than last October.

Consumer Insights Director at GfK, Neil Bellamy commented on the latest dataset, “After several years of high inflation, savvy consumers have adapted their purchasing strategies to make the most of their money when discounts are most attractive. Where possible, many now delay major purchases until one of these sales events – and the biggest of all is Black Friday, on November 28.”

He continued, “Both consumers and UK retailers will be watching closely to see whether the Chancellor’s Budget, to be announced just two days before Black Friday, boosts or dampens spending during that crucial weekend.”

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

Prime yields remain stable at 5.9%, signalling resilience and predictability in a cautious investment environment

Hotel investment surged 28% year-on-year, driven by strong single-asset deals and renewed investor confidence in London

Scottish market investment dipped 21% but quality assets and international buyers continue to drive solid demand

Monthly market update

The latest data from Savills reflects a commercial property market that could either be considered as stable or sluggish.

The figures indicate a commercial market that is holding its ground against a backdrop of ongoing economic and political uncertainty. Since February, the average prime yield has remained steady at 5.9%, suggesting a degree of predictability despite wider market pressures. While four sectors are showing a downward trend, seven sectors have not changed for at least 18 months. While this may spark concern about stagnation, it could also offer reassurance for investors who are prioritising consistency.

There are some positive signs for the market. In the second quarter of this year, commercial property investment reached the second-highest level recorded in the past 13 quarters. Looking ahead, Savills predicts that, by the end of 2025, total investments volumes for office and industrial sectors will exceed the 2024 total.

Increased investment in hotel sector

UK hotel investment showed strong growth in the third quarter of this year according to Savills.

Total hotel investment reached £1.04bn in Q3, marking a 28% year-on-year increase. This growth was largely driven by single asset transactions, which represented 92% of all activity and was nearly 60% above the ten-year average for Q3.

London was the investment hotspot in Q3, with total volumes rising by 42% year-on-year to £697m. Savills suggested that this strong performance was due to the capital’s large share in hotel stock combined with a rebound in investor appetite.

David Kellet at Savills commented, “While the first half of the year was defined by operational and investor uncertainty in the UK hotel market, sentiment has stabilised through Q3.” He added, “We expect the single asset market to remain robust whilst also anticipating more larger portfolios to transact in 2026.”

How’s the Scottish market faring?

Analysis from Knight Frank shows a total of £1.46bn was invested in Scotland’s commercial property market during the first three quarters of 2025.

Although this represents a 21% decline compared with the same period last year (£1.85bn), it remains broadly in line with the average levels for Q3 during 2020-2024.

So far this year, retail is the sector that has attracted the highest volume of investment, totalling £452m. The industrial sector also performed strongly, recording its second-best third quarter since the pandemic, with completed deals worth £153m. International investors are on track to have their highest share in investment since 2022, accounting for 45.9% of deals in the first three quarters of the year.

Alasdair Steele at Knight Frank observed, “Fewer deals are happening, but the assets that are trading hands tend to be higher quality buildings in prime locations and are attracting a good deal of interest.”

The place of AI in commercial property

Artificial intelligence (AI) is being adopted across the commercial real estate sector in a variety of ways, transforming how the industry operates.

The technology is increasingly being used to enhance efficiency and support decision-making. AI systems can analyse years of market data in just minutes, helping underwriters to generate faster valuations and enabling asset managers to assess the potential impact of interest rates and policy changes. This frees up professionals to focus on other tasks, such as client relationships and strategy planning.

AI is not just adopted by market analysts; it can also be used in the commercial properties themselves. For example, smart systems are helping to reduce energy use and improve comfort by automatically adjusting heating and cooling systems based on real-time data. CBRE explained, “By harnessing machine learning, building managers can now see weeks in advance when a system might fail, preventing tenant disruption and lowering costs.”

All details are correct at the time of writing (22 October 2025)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission

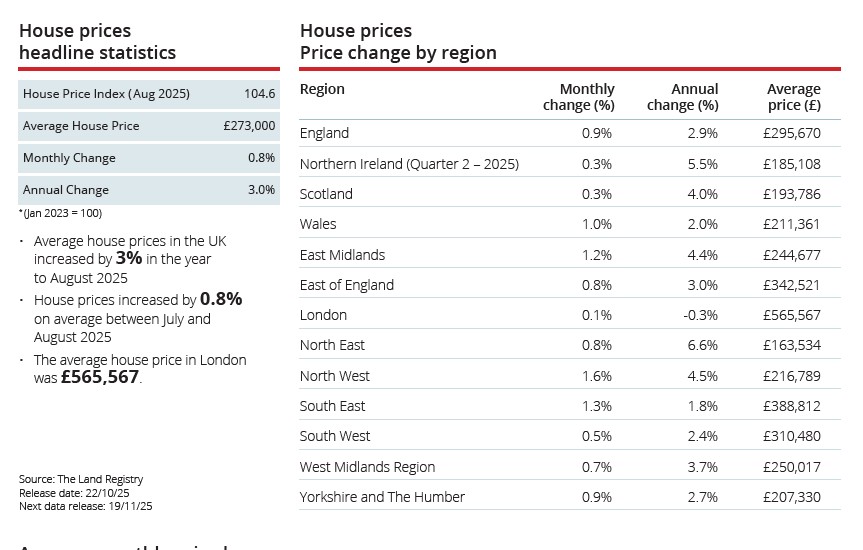

The housing market remains subdued, with buyer demand, listings and sales activity all slipping amid pre-Budget uncertainty

Landlord exits drive a sharp fall in rental supply, prompting RICS to forecast a 3% rent rise next year

The government plans to make reforms to speed home sales and cut fall-throughs, including digital property packs and conditional contracts

Residential market subdued

The housing market showed signs of subdued growth in September, according to the latest UK Residential Market Survey from the Royal Institution of Chartered Surveyors (RICS).

The report revealed that new buyer enquiries fell for the third consecutive month, with a net balance of -19% in September. Sales activity also remained in negative territory at -16%, although this marks an improvement on August’s figure of -24%. Meanwhile, new listings declined for the second month in a row, reaching -15%. This caution among buyers and sellers is likely due to the upcoming Autumn Budget, which has caused widespread uncertainty.

In the rental market, tenant demand remained broadly flat at -1%, however landlord instructions fell sharply to -38%, the lowest level since May 2020. This reflects an ongoing trend of landlords leaving the sector, leading to a continued imbalance between supply and demand. As a result, RICS expects rents to rise by around 3% over the next year.

Government proposes home-buying reform

The government has launched a consultation to overhaul the home buying and selling system.

It currently takes an average of 120 days to complete a transaction after an offer has been accepted, hence the need to make the process simpler, faster and more reliable.

One key proposal is to ensure that comprehensive information about a property is available at the point of listing. The government notes that this approach has helped to deliver ‘faster, more certain transactions in Scotland.’ To support this, there is a proposal for the widespread use of digital property packs, which would store current and historic details about a home.

As things stand, buyers and sellers can withdraw from a transaction at any point up until the exchange of contracts. To reduce fall-throughs, proposed reforms could include the use of conditional contracts, which would make the transaction binding at an earlier stage. If a party withdrew, they would typically face a financial penalty.

Britain’s best new building

Appleby Blue Almshouse in Southwark, south London, has won the 2025 Royal Institute of British Architects (RIBA) Stirling Prize for Britain’s best new building.

Designed by Witherford Watson Mann, the development reimagines the traditional almshouse to address loneliness and provide affordable, high-quality housing for people over 65. The complex contains 59 flats alongside communal areas, including a courtyard, roof garden and community kitchen, all designed to foster connection and wellbeing.

Judges praised the project for ‘setting an ambitious standard for social housing among older people,’ with jury member, Ingrid Schroder, highlighting its “high-quality” and “thoughtful” design that “truly cares for its residents.”

Features such as terracotta-paved hallways with benches and plants, and a central water feature, create what RIBA described as an ‘aspirational living environment’ that contrasts sharply with the ‘institutional atmosphere often associated with older people’s housing.’

All details are correct at the time of writing (22 October 2025)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission

Investors face rapid change due to inflation, geopolitical uncertainty, AI and the energy transition

IMF forecasts global growth of 3% in 2025, but warns of persistent downside risks

Agility, diversification and long-term structural alignment are vital to manage risk and capture growth

Adapting to transformation – investing through global change

As we enter the final quarter of what has been an eventful year so far, investors have had much to navigate. From sharp US policy shifts, geopolitical instability, global trade realignments and a changing labour market, to the energy transition, elevated uncertainty and the prevalence of mega forces such as artificial intelligence. The investing landscape continues to evolve rapidly. What matters now is recognising the defining features shaping this environment as it transforms.

Inflation expectations are no longer anchored at 2% targets, fiscal discipline is under pressure and long-term growth trajectories are shifting. Against this backdrop, markets are reacting more quickly to short-term data, as investors look to interpret what it signals for both near-term performance and longer-term outcomes.

Key policy priorities

The International Monetary Fund’s (IMF’s) latest World Economic Update projects global growth expectations of 3% this year, rising slightly to 3.1% in 2026 – an upgrade on earlier forecasts. The revision reflects front-loading ahead of tariff changes, lower effective tariff rates, improved financial conditions, and fiscal expansion in key economies. While global inflation is expected to ease, it is anticipated to remain above target in some key countries like the US and on home shores. The IMF deduce, ‘Downside risks from potentially higher tariffs, elevated uncertainty, and geopolitical tensions persist. Restoring confidence, predictability and sustainability remains a key policy priority.’

Inflection point

During the World Economic Forum’s Annual Meeting at the start of the year, President and CEO Børge Brende said, “we are at an inflection point,” adding that the forum was taking place during “one of the most uncertain geopolitical and geoeconomic moments in generations.”

Fast forward to their August review and the Forum highlighted how a number of key issues are set to shape the global outlook over the coming months. These include renewed collaboration to tackle conflict and misinformation, large-scale reskilling to meet job transformation, redesigning financial systems for longer lifespans, greater investment in sustainable infrastructure and the energy transition, and accelerating gender parity and digital inclusion.

Together, these areas underline both the challenges and opportunities of this moment – and why, for investors, staying agile, globally diversified and aligned with long-term structural shifts, will be key to capturing growth while managing risk in line with their personal tolerances.

Embracing change

The key is not just to acknowledge this transformation but to see the opportunities it creates. Understanding how these forces interact can help position portfolios to capture growth while protecting against volatility in a changing world. The good news? You’ve got us to help you traverse and capitalise on these driving forces shaping our world.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. The Financial Conduct Authority (FCA) does not regulate Will writing, tax and trust advice and certain forms of estate planning.

The UK economy grew slightly in August, but experts warn of tougher months ahead

The IMF sees steady global growth, with the UK outperforming most G7 nations this year

US-China tensions flare as rare earth export controls spark new tariff threats

“We will continue to prioritise economic and fiscal stability”

Latest data from the Office for National Statistics (ONS) indicates that the economy experienced a slight expansion of 0.1% in August. In the three months to August, GDP increased by 0.3% – this is a slight improvement on the three months to July, which saw expansion of 0.2%.

The services sector was the main driver of economic growth in the three months to August, increasing by 0.4%, due to a strong contribution from human health and social work activities. However, in August alone, services did not see any growth. Construction increased by 0.3% in the three months to August, while production output decreased by 0.3% due to a significant fall in electricity, gas, steam and air conditioning supply.

Some experts predict economic growth to continue weakening in the coming months, as households face higher food costs and businesses feel the effects of tax rises that came into effect in April. If the Chancellor announces more tax hikes in the upcoming Budget, there could be further strain. Speaking on this last week, Rachel Reeves said, “I’ve always been very clear that we will continue to prioritise economic and fiscal stability in the UK.” When asked if taxes will be raised further, she said, “As we get the forecast and as we develop our plans, of course we are looking at further measures on tax and spending, to make sure that the public finances always add up.”

IMF publishes outlook on economic growth

The International Monetary Fund (IMF) has released its latest projections for global growth. From an international perspective, the economy is expected to grow by 3.2% in 2025 followed by expansion of 3.1% in 2026, a slowdown from 3.3% recorded in 2024.

Meanwhile, the UK has reason to be both cautious and hopeful. On the upside, the UK is set to be the second-fastest growing economy out of all the G7 countries this year, with a projected expansion of 1.3%. This has been revised up from April estimates, reflecting strong activity in the first six months of the year and improvements in what IMF calls the ‘external environment,’ including the trade deal with the US announced in May. However, the UK is also forecast to have the fastest rate of inflation in 2025 and 2026, with CPI predicted to rise by 3.4% and 2.5% respectively. However, IMF believes that, by the end of next year, UK inflation will ease to 2% due to ‘a loosening labour market and moderating wage growth’. IMF’s Pierre-Olivier Gourinchas commented, “The path forward for the Bank of England should be very cautious in its easing trajectory and make sure that inflation is on the right track.”

US-China trade war escalates

Trade tensions are mounting again between the US and China. The two countries reached a reciprocal agreement to reduce tariffs in May 2025, but this fragile truce has been disturbed. On 9 October, China announced that foreign companies will need approval from the Chinese government to export products containing rare earths. These materials are essential to the US, being used in technology such as smartphones, electric cars and military equipment. In response, President Trump threatened to impose an additional 100% tariff on Chinese goods starting from 1 November. China’s President Xi Jinping and Trump are set to meet later this month. China processes 90% of the world’s rare earths, so experts believe that its new restrictions might give China leverage to negotiate a more favourable trade deal with the US.

Mortgage rates rise

According to data from Moneyfacts, the average two and five-year fixed mortgage rates have risen for the first time in eight months to 4.98% and 5.02% respectively. Although this may come as a disappointment to borrowers, rates are still notably lower than this time last year, where two and five-year rates were 5.40% and 5.07% respectively. Rachel Springall at Moneyfacts commented, “Volatile swap rates and a cautious approach among lenders have led to an abrupt halt in consecutive monthly average rate falls”.

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (22 October 2025)