Interest rates rise again

In February, the Bank of England’s Monetary Policy Committee (MPC) announced

an increase in its main interest rate for the second meeting in a row as the

Bank continues to grapple with a rapid rise in the cost of living.

At its latest meeting held in early

February, the MPC sanctioned a quarter of a percentage point rate rise taking

Bank Rate to 0.5%. In what was a surprise split decision, however, four of the

nine-member committee voted for a larger hike, seeking to raise rates by half a

percentage point.

The decision to increase rates is

designed to contain the country’s spiralling rate of inflation, which the Bank

now expects to peak at around 7.25% in April. This would represent the fastest

rate of consumer price growth since 1991 and would leave inflation

significantly above the Bank’s 2% target level.

Data subsequently released by the Office

for National Statistics (ONS) showed that inflation, as measured by the

Consumer Prices Index, rose to 5.5% in the 12 months to January, putting the

cost of living at a near 30-year high. This figure was above most predictions

in a Reuters poll of economists, with the consensus suggesting the rate would

hold steady at the previous month’s level of 5.4%.

The latest inflation statistics appear to

have reinforced the chances of a third consecutive rate rise at the conclusion

of the MPC’s next meeting on 17 March. The minutes from February’s meeting

acknowledged that the Bank expects ‘further

modest tightening in monetary policy’ to be appropriate ‘in the coming months’ and, according to

a Reuters poll, most economists now predict a quarter percentage point rise in

March. Furthermore, almost half of respondents also forecast a similar hike at

May’s meeting.

Signs of economic resurgence

The latest gross domestic product (GDP)

statistics show the UK economy suffered a smaller than expected economic hit in

December while more recent survey evidence points to a sharp acceleration in

growth during February.

Data released last month by ONS revealed

that UK economic output fell by 0.2% in December as people increasingly worked

from home and avoided Christmas socialising due to the spread of the Omicron

variant. This contraction, however, was less severe than many had feared, with

a Reuters poll of economists having predicted a 0.6% monthly fall.

Despite December’s decline, GDP data

covering the whole of last year showed the UK economy experienced a sharp

rebound in 2021, following the dramatic pandemic-induced collapse in output

recorded during the previous year. In total, the economy grew by 7.5% across

2021, the UK’s largest annual rate of growth since 1941.

More recent survey data also suggests

there has been a swift rebound in economic activity following the disruption

caused by Omicron at the turn of the year. The preliminary headline reading of

the closely monitored IHS Markit/CIPS composite Purchasing Managers’ Index, for

instance, rose to 60.2 in February from 54.2 in January.

This represents the fastest pace of

growth in private sector output since last June, with a strong recovery in

consumer spending on travel, leisure and entertainment fuelling the pickup in

activity. IHS Markit’s Chief Business Economist Chris Williamson said the data

pointed to a “resurgent economy in February” as COVID containment measures were relaxed.

Mr Williamson

did though add a note of caution, saying

that “indications of a growing plight for

manufacturers” needed to be watched. He added, “Given the rising cost of

living, higher energy prices and increased uncertainty caused by the escalating

crisis in Ukraine, downside risks to the demand outlook have risen.”

Markets (Data

compiled by TOMD)

The Russian invasion of Ukraine has understandably

impacted global markets. Due

to the uncertain nature of the fast-evolving situation, global markets

initially reacted with many stocks moving into the red and the oil

price pushing beyond the $100 milestone as supply concerns intensified.

Markets reacted

accordingly on the last trading day of the month following news that Vladimir

Putin had placed the nuclear deterrent on high alert the previous day. A raft of

economic sanctions against Russia are being imposed, including a

move designed to cut off Moscow’s major financial institutions from Western

markets. Chancellor Rishi Sunak said the sanctions “demonstrate

our steadfast resolve in imposing the highest costs on Russia and to cut her

off from the international financial system so long as this conflict

persists.”

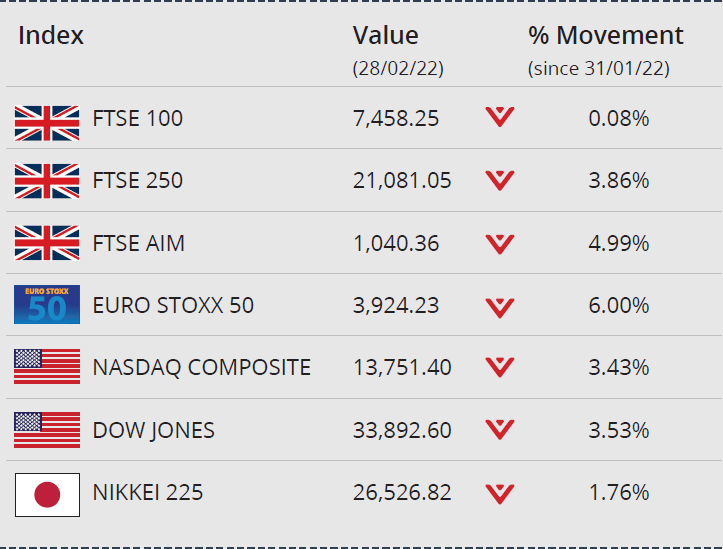

At the

end of February, major global markets largely closed in negative territory as

investors pensively monitored developments. In the UK, the FTSE 100 closed the

month down 0.08% on 7,458.25, the FTSE 250 and AIM also both lost ground to

close the month on 21,081.05 and 1,040.36, losses of 3.86% and 4.99%

respectively.

In Japan, the Nikkei 225 ended

the month on 26,526.82, down 1.76%, and the Euro Stoxx 50 closed February down

6.00% on 3,924.23. Stateside, the Dow Jones closed

February down 3.53%, while the NASDAQ closed down 3.43%.

On the foreign exchanges, sterling closed the month at $1.34 against the

US dollar. The euro closed at €1.19 against sterling and at $1.12 against the

US dollar.

The oil price moderated at month end with Brent Crude closing the month trading at around $98 a barrel, a gain of over 9%. Investors flocked to gold, which is currently trading at around $1,903 a troy ounce, a gain of over 6% on the month.

Pay levels fall in real terms

While the latest set of earnings statistics did report relatively

strong growth in nominal wage levels, the data also showed that pay growth is

now lagging the rapidly rising cost of living.

ONS figures released last month showed

that average weekly earnings, excluding bonuses, rose at an annual rate of 3.7%

in the final quarter of last year. This exceeded market expectations and was

also higher than Bank of England forecasts.

However, although the rate remains

relatively high in comparison to levels witnessed over the last decade, pay

growth is now failing to keep up with the spiralling rate of inflation. Indeed,

in real terms, regular earnings fell by 0.8% compared to Q4 2020.

In early February, after announcing the

latest interest rate rise, Bank of England Governor Andrew Bailey called on

workers to rein in pay demands or risk a wage-inflation spiral. The tight

labour market, however, means employers are increasingly having to offer higher

salaries to retain existing workers and attract new staff. Early ONS estimates

suggest these pressures are driving wage growth, with median earnings for

workers on payrolls in January 6.3% higher than the same month last year.

Government debt costs rising

The latest public sector finance statistics show borrowing remains

below forecast, although rising inflation is pushing up the cost of servicing government

debt.

January is typically a strong month for

public finances due to seasonal inflows of Income Tax and this year ONS data

revealed a £2.9bn surplus. While this was a distinct improvement on last year’s

£2.5bn deficit, it was below market expectations and £7bn less than January

2020’s pre-pandemic surplus.

While year-to-date borrowing remains

significantly ahead of Office for Budget Responsibility forecasts prepared for

the last Budget, higher inflation has started to push up interest payments via

its impact on index-linked debt. Economists expect this to limit the

Chancellor’s room for manoeuvre when he delivers a fiscal update on 23 March.

Isabel Stockton, a Research Economist at

the Institute for Fiscal Studies, commented, “Borrowing remains likely to

come in below that forecast in the Budget. This will doubtless be good news for

the Chancellor as he prepares for his Spring Statement. But borrowing still

remains high by historical standards and while he is currently meeting his

fiscal targets, Mr Sunak has left himself with very little wriggle room.”

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from, taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.