Retailers

report sales growth

Online discounts and the hot summer weather have encouraged an uplift in retail

sales, with the latest official statistics showing a rise in July and survey

data pointing to further growth in August and September.

Data released by the Office for National Statistics (ONS) revealed that total retail sales

volumes rose by 0.3% in July; this was the

first increase in three months and confounded economists’ expectations of a

small monthly decline. Growth was largely driven by a surge in online and mail

order sales, which recorded their sharpest rise since December.

July saw

Amazon hold its annual Prime Day promotion, although ONS did say that greater spending was seen across a number of online retailers, with sales figures boosted by ‘a range of offers

and promotions.’ The British Retail Consortium also noted that ‘the summer sunshine’ had provided a boost to the figures, with sales

of ‘summer clothing, air conditioning appliances and outdoor foods’ all

benefitting from record temperatures.

Evidence

from the latest CBI Distributive Trades Survey also suggests the retail sector enjoyed a further uplift in sales last month, with the net balance of retailers reporting year-on-year sales

growth jumping to +37 in August from -4 in July; this represents the

strongest reading in nine months. In addition, retailers said they expect to see

another rise in sales this month.

The CBI survey did, however, note an air of

pessimism when it comes to the future business

outlook. Other data released last month also highlighted growing concerns across the UK household sector, with

GfK’s long-running Consumer Confidence Index falling to a low of -44 in August. Measures of households’ assessment of

the general economic situation and their personal finances both declined last

month, which GfK said reflected ‘acute concerns as the cost-of-living soars.’

In early August, the largest increase in interest rates for more than a quarter of a century was sanctioned by the Bank of England

(BoE) as it continues its efforts to contain the rate of inflation.

At a meeting which concluded on 4 August, the BoE’s nine-member Monetary Policy Committee (MPC) voted by a

majority of eight to one to raise Bank Rate by half a percentage point to

1.75%. This was the sixth increase since

December and took rates to their highest level since late 2008.

Minutes to the meeting noted that inflationary pressures had ‘intensified

significantly’ since the previous meeting held in mid-June, largely due to the impact of Russia’s

invasion of Ukraine on energy prices. A readiness to ‘act forcefully’ to indications of more

persistent inflationary pressures was again reiterated, but the minutes also stressed that the MPC would assess its next move as events unfolded and that policy was ‘not on a

pre-set path.’

When announcing the

rate decision, the Bank also provided an update of its view on the

future path of inflation, warning that it now expects the

Consumer Prices Index (CPI) to peak at ‘just over 13%’ in the final quarter of this year. It then expects inflation to remain at ‘very elevated levels’ throughout

much of next year before returning to its target level of 2% in 2024.

Meanwhile,

the latest data released by ONS showed that soaring food costs pushed the rate of

inflation into double digits for the first time since 1982. In the 12 months to

July, the CPI rate jumped to 10.1%, a sharp increase from June’s 9.4% figure and above all forecasts submitted in a Reuters poll of economists. This rise further fuelled expectations of another interest rate hike when the MPC next convenes in mid-September.

Markets (Data

compiled by TOMD)

Global markets largely closed August in negative territory. Many indices

moved into the red at month end as investors digested hawkish comments from Federal Reserve

Chairman Jerome Powell, where he cautioned that the US Fed would act “forcefully”

to control inflation though it would result in “some pain to households

and businesses.” Inflation will require continued aggressive global

policy, with eurozone inflation data also weighing on market sentiment at month

end.

The Fed’s next

meeting, where interest rates will be addressed, takes place on 21 September, with

markets having several key economic reports to consider over the next few

weeks. Looking at US

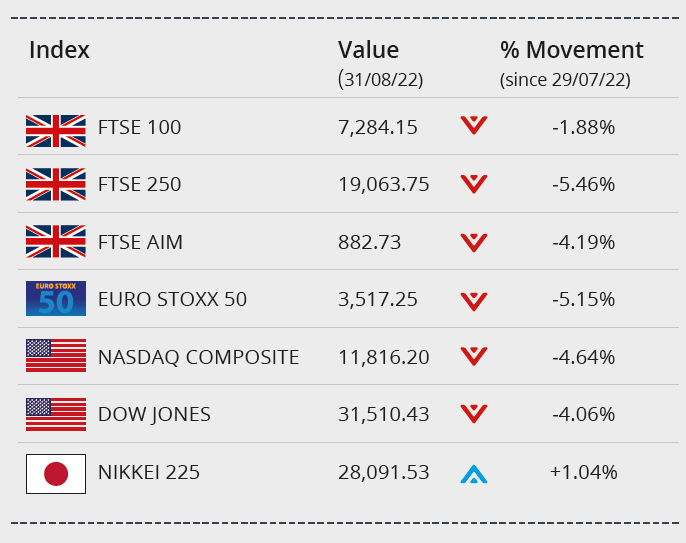

markets, the Dow closed the month down 4.06% on 31,510.43. The tech-heavy Nasdaq, which tends to be more

sensitive to Fed policy, closed August on 11,816.20, down 4.64%.

In the UK, the FTSE

100 closed August down 1.88% on 7,284.15, while the midcap-focused FTSE 250

registered a loss of 5.46%. The AIM recorded a loss of 4.19% in the month. The Euro Stoxx 50 closed

the month down 5.15% on 3,517.25. In Japan, the Nikkei 225 closed

August on 28,091.53, up 1.04%.

On the foreign exchanges, sterling closed the month

at $1.16 against the US dollar. The euro closed at €1.15 against sterling and

at $1.00 against the US dollar.

Gold is currently trading at around $1,715 a troy ounce, a loss of 2.14% on the month. The hawkish Fed comments indicating more interest rate rises, combined with solid US labour statistics, impacted the gold price. Brent Crude closed the month trading at around $95 a barrel, a drop of around 9.5%. Oil prices traded lower as concerns over global economic growth and renewed restrictions in China weighed.

Despite economic output falling by less than feared in June, the UK economy still contracted over the second quarter as a whole, with experts typically predicting an increasingly gloomy outlook.

As expected, the latest growth statistics released by ONS revealed that output

fell in June, partly due to the month unusually containing two bank holidays to celebrate the Queen’s Platinum

Jubilee. However, a 0.6% contraction was less severe than the consensus 1.3% decline predicted

by economists in a Reuters poll. June’s figure did though mean the economy

shrank by 0.1% in the second quarter of this year.

Economists are divided over third quarter prospects, with some

predicting a second successive quarterly contraction – which would meet the

technical definition of a recession. Although others are forecasting a small rebound in growth between July

and September.

The BoE’s latest assessment predicts the UK

economy will next contract in the final quarter and then keep shrinking until

the end of 2023. While this would represent a relatively long downturn, the

Bank’s calculations suggest a 2.1% peak-to-trough fall in output, far less than

the economic hits from COVID and the 2008-09 global financial crisis.

Signs of cooling labour market

While the latest batch of employment statistics do suggest the overall picture

in the jobs market remains positive, there are early signs that things may be starting to cool.

Figures

released last month by ONS showed that the rate of unemployment in the three

months to June was unchanged at 3.8%, close to a half-century low. The data

also revealed further strong growth in the number of people in work – rising by

160,000 across the April to June period – although this increase was considerably less than the 256,000 rise analysts had predicted.

In terms of

job vacancies, the data revealed that the total fell by 19,800 in the May to July period. While this still

leaves the overall number of vacancies close to a record high at 1.274 million, it was the

first reported decline in this figure since mid-2020.

Survey evidence released early last month also points to signs of cooling

in the labour market. Although data from the latest UK Jobs Survey conducted by

KPMG, and the Recruitment and Employment Confederation, shows the jobs market ‘remains

solid,’ it also found that businesses are becoming more cautious, with the

slowest increases in both permanent staff appointments and temp billings for 17

months.

It is

important to take professional advice before making any decision relating to

your personal finances. Information within this document is based on our

current understanding and can be subject to change without notice and the

accuracy and completeness of the information cannot be guaranteed. It does not

provide individual tailored investment advice and is for guidance only. Some

rules may vary in different parts of the UK. We cannot assume legal liability

for any errors or omissions it might contain. Levels and bases of, and reliefs

from, taxation are those currently applying or proposed and are subject to

change; their value depends on the individual circumstances of the investor. No

part of this document may be reproduced in any manner without prior permission.