“Our reforms deliver smarter regulation of financial services that will unlock growth and opportunity”

Last Friday, as temperatures plummeted, Chancellor Jeremy Hunt announced a package of over thirty UK financial services regulatory reforms, dubbed the ‘Edinburgh Reforms,’ which the government intends will ‘unlock investment and turbocharge growth in towns and cities across the UK.’ A considerable overhaul, the effects will be far-reaching, with the financial services sector contributing £216bn a year to the UK economy.

Speaking at an industry roundtable in Edinburgh, he outlined a series of measures to ‘seize the benefits of Brexit’ establishing the government’s approach to reversing what they regard as ‘burdensome’ elements of EU law.

Measures include establishing new rules governing how senior finance executives are hired and sanctioned, and a commitment to make legislative progress on replacing the rules governing insurers balance sheets, expected to unlock over £100bn of private investment.

Mr Hunt commented, “We are committed to securing the UK’s status as one of the most open, dynamic and competitive financial services hubs in the world.”

Andrew Griffith, Economic Secretary to the Treasury added, “The UK is a financial services superpower – and we have long benefited from, and are committed to, high quality regulatory standards… Our reforms deliver smarter regulation of financial services that will unlock growth and opportunity in towns and cities across the UK.”

GDP update

As the country ground to a halt, grappling with a combination of heavy snowfall and strike action, news came on Monday that the UK economy contracted by 0.3% in the three months to October as soaring prices took their toll on households and businesses. Over the period, economic activity slowed across all primary sectors including services, construction and production. However, in October, GDP is estimated to have grown by 0.5% following a fall of 0.6% in September. Growth in October was driven by the services sector.

Household confidence on the ropes

The recently released Q3 Household Finance Review from UK Finance has revealed that consumer confidence has continued to fall below current record lows, due to a combination of factors including rising energy prices and inflation, the ongoing conflict in Ukraine, plus the fallout from September’s Growth Plan. Confidence regarding the general economic situation reached an all-time low of -62. Key points from Q3 included:

- Although inflation masked weaker activity in some sectors, spending remained relatively strong overall, with card spending defying weak consumer sentiment for both the value and number of transactions

- Personal loan borrowing to fund larger purchases subsided in the quarter, following strong growth during H1 2022

- House purchase activity aligned with pre-pandemic levels during Q3, but weakness is anticipated as the labour market softens into 2023 and affordability issues come to the fore

- Refinancing held firm in Q3 due to a strong maturity schedule, but it is strongly anticipated that inflation and interest rate rises will prove challenging for the 1.8 million fixed rate loans set to mature in 2023.

“A new era for UK coinage”

On Thursday, almost five million new 50p coins bearing the image of King Charles III entered circulation via Post Offices across the UK this month. It is expected that a total of 9.6 million of the coins will enter circulation in line with demand. Rebecca Morgan, Director of Collector Services at The Royal Mint, spoke on the launch of the new coin last week, “Today marks a new era for UK coinage, with the effigy of King Charles III appearing on 50ps in circulation… We anticipate a new generation of coin collectors emerging, with people keeping a close eye on their change to try and spot a new 50p that bears the portrait of our new King.”

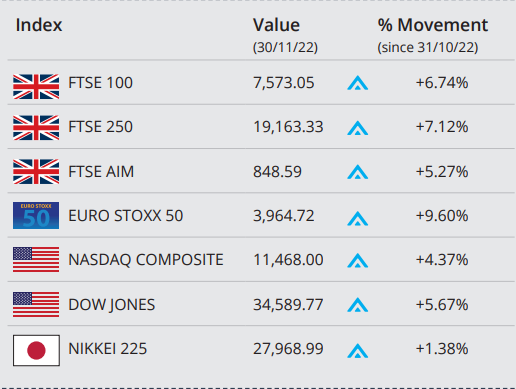

Markets

At the tail end of last week, UK stocks made some modest gains on the back of the Chancellor’s reforms to overhaul financial services regulations, with UK insurers, banks and asset managers among the companies lifting the FTSE 100 higher. Enter the new week and London’s markets sustained losses on Monday after falls on the back of a sharp rise in natural gas prices, but on Tuesday, the FTSE 100 advanced 0.7% as gains in energy stocks outpaced weakness in consumer staples and news of slowing US inflation filtered through.

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. All details are correct at time of writing (14 December 2022)