Owning a home can create significant long-term savings when compared with renting

Renters in London and Bristol are missing out the most on savings opportunities

Despite challenges, many younger renters are optimistic about owning their first home

Research1 has compared the average cost of buying versus renting, highlighting the investment opportunities that homeowning can offer.

By the second year of homeownership, buyers are likely to be saving about £99 when compared with renters. The gap in wealth creation only widens over time, with homeowners potentially saving around £12,157 by the tenth year. This rises to £206,031 over 30 years. If homeowners decided to invest their savings, their returns could grow even more.

The report showed that the wealth created from homeowning varies depending on the region. Renters in London are potentially missing out on £540,687 over 30 years of homeownership. The gap is wider in Bristol, where homeowners could save £573,110.

Barriers to homeownership

Although owning a home comes with benefits, many renters do not believe it is attainable. Two thirds (65%) of those renting hope to buy, with the same proportion (64%) recognising that homeowning offers more long-term financial security. However, a quarter (27%) of renters don’t think they could ever afford their own home. Meanwhile, only 8% say they prefer the flexibility that comes with renting.

High property prices seem to be the most common barrier to homeownership, with 61% of renters citing this as an issue. Some 56% said that saving for a deposit was a challenge, followed by 32% pointing to income insecurity.

Reasons to be optimistic

Promisingly, only 11% of 25 to 34-year-olds thought that homeownership was out of reach for them. This proportion went down to just 7% for 18 to 24-year-olds. Also, 56% of tenants would consider buying if their monthly mortgage repayments were the same price as their rent. In some regions of the UK, this is becoming feasible, so this may help renters to grow in confidence in the coming years.

It’s right to be optimistic – we’re here to help turn your homeownership dreams into a reality.

1MAB, 2025

As a mortgage is secured against your home or property, it could be repossessed if you do not keep up mortgage repayments.

Gifting can reduce IHT, but poor record-keeping could cause the exemption to be rejected

Gifts with reservation (e.g. continuing to benefit from gifted assets) often trigger unexpected IHT bills

With frozen thresholds and pensions joining IHT, careful planning is more important than ever

With pensions set to join the list of assets liable for IHT, for many families, this ends a major tax break and makes effective planning essential. One of the most powerful tools is gifting. However, when done incorrectly, it can wipe out the benefit entirely.

Getting gifting right

Some gifts are exempt straight away, like the £3,000 annual allowance or small gifts under £250. Larger gifts, known as Potentially Exempt Transfers (PETs) escape IHT if you live for seven years after making them. Regular gifts from surplus income can also be tax free, provided they don’t reduce your standard of living and you keep detailed records.

Detailed record-keeping includes evidence of:

• What was given, when, and to whom

• The value of the gift at the time

• The source of the funds (especially for gifts from income)

• Proof that the gift did not reduce your normal standard of living.

This might include bank statements, written notes of intention, valuations and a spreadsheet tracking dates and amounts. Without this paper trail, HMRC could reject the exemption.

The trap – gifts with reservation

The most common pitfall is the ‘gift with reservation of benefit’ – where you give something away but keep using it. For example, transferring your holiday home to your children, but continuing to use it rent-free will keep it in your estate for IHT. Hundreds of families fall foul of this each year, with surprise bills running into tens of thousands.

Protect your legacy – speak to us today

With thresholds frozen and pensions entering the IHT net, please get in touch to review your plans and avoid your gifts backfiring, to make sure your wealth passes on the way you intend.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. The Financial Conduct Authority (FCA) does not regulate Will writing, tax and trust advice and certain forms of estate planning.

Global growth is set to cool as tariffs bite, though resilient economies and easing inflation support longer-term stability

UK conditions remain mixed, with modest growth, persistent inflation pressures and regional housing markets moving at varied speeds

Construction output weakens sharply while long-term energy network investment pushes household bills higher over the coming years

‘The global economy has proved more resilient than expected this year’

The Organisation for Economic Co-operation and Development (OECD) has released its latest Economic Outlook, setting out projections for global growth over the coming years.

According to the report, global economic growth is expected to slow from 3.2% in 2025 to 2.9% in 2026 due to higher tariff rates temporarily impacting trade and investment. However, once economies have adjusted to this change, GDP growth is forecast to pick up slightly to 3.1% in 2027, supported by stronger financial conditions. Inflation is expected to return to target in most major economies – in the G20 countries, it should ease from 3.4% in 2025 to 2.5% on average in 2027.

Overall, the OECD noted that, ‘The global economy has proved more resilient than expected this year, supported by improved financial conditions, rising AI-related investment and trade and macroeconomic policies. However, underlying fragilities are increasing.’

Emerging Asian economies are set to be key drivers of global growth in 2026; India is projected to lead the way with growth of 6.2%, followed by Indonesia at 5.0%.

In the UK, GDP growth is expected to slow to 1.2% next year, held back by ongoing economic uncertainty and tight government budgets. While fiscal policy is set to remain restrictive, growth is forecast to slightly increase to 1.3% in 2027, supported by business investments and exports. Inflation is set to remain high at 2.5% in 2026 – the second highest in the G7 countries. It should ease to 2.1% in 2027, but this is still just above the Bank of England’s target of 2%. The Outlook noted, ‘Continuing to ensure that consolidation is carefully timed, given substantial downside risks to growth and upside risks to inflation, and well-calibrated, with a combination of revenue-raising measures and spending cuts, is essential.’

The OECD also set out a series of recommendations to policymakers worldwide. These include working together to ease trade tensions, staying vigilant to shifts in inflation dynamics and strengthening financial stability frameworks.

House prices unchanged in November

The latest data from Halifax shows that house prices were flat in November with a monthly change of 0.0%, following an increase of 0.5% in October. Meanwhile, annual growth slowed to 0.7% – this is down from 1.9% in the 12 months to October and the slowest rate since March 2024. Despite this slow growth, the average property price is now £299,892, which is approaching a new record high.

The statistics indicate that the North/South divide in house prices persists. In England, the North West was the strongest performing region in November (+3.2%), followed by the North East (+2.9%). On the other hand, house prices fell by 1% in London and by 0.3% in the South East. The capital remains the most expensive region in the UK, with the average property costing £539,766.

Amanda Bryden, Head of Mortgages at Halifax, commented on November’s data, “While slower growth may disappoint some existing homeowners, it’s welcome news for first-time buyers. Comparing property prices to average incomes, affordability is now at its strongest since late 2015.”

Construction sector shrinks significantly

New research shows that, in November, the UK’s construction sector contracted at the fastest pace since the pandemic. The S&P Global UK Construction Purchasing Managers’ Index was at 39.4 last month – this is down from 44.1 in October and the lowest recording since May 2020. It also marks the eleventh consecutive month recording lower volumes of construction output. The significant drop was driven by sharp downturns in housing activity, commercial construction and civil engineering, which the report attributed to ‘fragile market confidence, delays with the release of new projects and a general lack of incoming new work.’

Energy bills set to increase

UK households will see an increase in energy bills in the coming years. Energy regulator Ofgem has approved a five-year plan to improve the UK’s electricity and gas grids. In order to fund this £28bn investment, household energy bills will increase by an estimated £108 by 2031. However, Ofgem said that, in the long run, the population will save more money as the project will make wholesale energy cheaper.

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (10 December 2025)

Women are less likely than men to hold life insurance or understand its benefits

Many women have not been educated about life insurance and believe they can’t afford it

Life insurance provides financial support to loved ones if the policyholder dies during its term

Women are falling through the cracks when it comes to life insurance. According to a new report, a third of women do not have a life insurance policy compared with 16% of men1. So, women are twice as likely not to have a life insurance than men – that’s a huge variation.

The report also revealed that 29% of women have never been educated about life insurance, versus 18% of men. This lack of education might explain why double the number of women believe they can’t afford life insurance compared with men.

For those women who do have life insurance, 29% are unsure how their policy would benefit loved ones in the event of their death.

Financial support in time of need

Life insurance can provide partners and families with vital financial support in the form of a lump sum or regular payments if the policyholder dies during its term with premium payments up to date. Life insurance claimants received a total of £4bn in payouts last year2.

The amount of money paid out depends on the level of cover that you purchase. This needs to be aligned with your personal requirements, it’s not a ‘one size fits all’ approach. Other protection policies which provide financial support if you are unable to work due to a critical illness or injury are also worth considering. People often take out a life insurance policy at the same time as a mortgage, with some providers making it a condition of the loan.

Don’t risk being uninsured or under-insured. It’s a small price to pay for the peace of mind you’ll benefit from.

1Life Insurance Index, 2025, 2Association of British Insurers and Group Risk Development

Financial protection policies typically have no cash in value at any time and cover will cease at the end of the term. If premiums stop, then cover will lapse.

More families now prioritise intergenerational planning, driven by record IHT receipts and policy changes

Only half of advised clients have IHT solutions in place, showing a clear advice-action gap

Women are set to control 60% of UK private wealth by 2025 but remain under-advised

The Great Wealth Transfer is happening, with the UK expected to see a significant shift in assets passed down to younger generations over the next 30 years. This is perhaps why more people are showing an interest in intergenerational financial planning.

A survey1 of financial advisers found that 80% of clients are now concerned about intergenerational planning, compared with 75% in 2022. Clients seem to be recognising this area as an increasing priority, with 39% seeing it as ‘highly important,’ up from 34% three years ago.

This growing focus is likely due to changes announced in last year’s Autumn Budget, which have prompted more advisers to use trusts when IHT planning. Also, record IHT receipts have probably encouraged people to take action to minimise their estate’s tax liabilities.

Who’s getting advice?

Intergenerational planning advice is more in demand, with 68% of clients discussing IHT with their adviser. However, only 47% of advised clients actually have solutions in place to reduce the IHT on their estate. Despite this advice-action gap, there’s a near-universal agreement that intergenerational planning matters, with 98% of advisers saying it is important to their clients.

The gender gap

Research2suggests that women are at the centre of the Great Wealth Transfer as they are 45% more likely to have inherited assets than men. This puts them on track to control 60% of UK private wealth by the end of 20253. Despite inheriting more, women do not hold as many long-term income generating assets. This could be because 69% of women said they haven’t received financial advice before.

It’s time to start a conversation about intergenerational planning. Preparation is essential to ensure wealth is passed smoothly and efficiently across the generations.

1HSBC Life (UK), 2025, 2Unbiased, 2025, 3CEBR, 2025

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. The Financial Conduct Authority (FCA) does not regulate Will writing, tax and trust advice and certain forms of estate planning.

The Budget included a number of tax and spending measures, estimated to raise £26bn in taxes by 2029/30

Key announcements included changes to Dividend Tax and changes to salary-sacrificed pension contributions

An extension of the freeze on Income Tax and secondary NIC’s thresholds until April 2031 was also announced

“This Budget will bring down inflation and provide immediate relief for families”

The Chancellor delivered her second Budget last Wednesday, which included a number of tax and spending measures, estimated to raise £26bn in taxes by 2029/30. In her opening remarks, Rachel Reeves said “This Budget will bring down inflation and provide immediate relief for families,” before adding that she was choosing to deliver“a Budget for fair taxes, strong public services, and a stable economy.”

Ms Reeves confirmed the Budget will see an expansion of the buffer for meeting the government’s fiscal targets, with the amount of headroom more than doubling from last year’s figure of £9.9bn to £21.7bn.

Turning her attention to the Office for Budget Responsibility’s (OBR’s) fiscal outlook, she announced an upgrade to economic growth forecasts for this year from 1.0% to 1.5%. Growth is then expected to be 1.4% next year and 1.5% across each of the following four years. OBR calculations show CPI inflation will average 3.5% this year, tempering to 2.5% next year, although still above the Bank of England’s 2% target. Inflation is then expected to reach target in 2027.

Some of the key measures announced included:

The lifting of the two-child limit on welfare payments from next April, allowing families on Universal Credit and tax credits to receive payments for all children

Properties in England valued at over £2m will face a new Council Tax surcharge of £2,500, with an annual levy of £7,500 owed for homes worth £5m plus, from April 2028

A new mileage-based road tax for electric and plug-in hybrid vehicles will be introduced from 2028

The first £2,000 of salary-sacrificed pension contributions will remain exempt from National Insurance contributions (NIC’s), but any amount above that will attract both employer and employee NICs from April 2029

The State Pension will increase by 4.8% from 6 April 2026.

And on personal taxation, key announcements included:

From April 2026, Dividend Tax will increase by two percentage points for basic and higher rate taxpayers. From April 2027, savings and property income will follow suit

An extension of the freeze on Income Tax and secondary NIC’s thresholds until April 2031

The annual Cash ISA allowance will be cut to £12,000 for those under 65 from April 2027, with the remaining £8,000 only permitted to be invested in stocks and shares ISAs.

Responding to the Budget, Helen Miller, Director of the Institute for Fiscal Studies (IFS) commented, “This was a big Budget, but not in the way people were necessarily expecting. Yes, there was a big tax rise… Yes, there was an increase in ‘headroom’… but there was also a sizeable increase in borrowing in the short term… To bear down on borrowing in later years and deliver that increase in ‘headroom’, the Chancellor is relying heavily on tax rises towards the back end of the Parliament. More borrowing for the next few years, then a sharp adjustment.”

Retail sentiment weakens but Black Friday should provide a boost

Retail sentiment has fallen at its fastest pace in 17 years, as more firms anticipate a deterioration in trading conditions over the next quarter, according to the CBI’s latest Distributive Trades Survey. Sales volumes dropped sharply in the year to November, extending a period of weakness that began in mid-2023. Retailers expect demand to stay subdued into December, with sales likely to fall again, though at a slower rate.

Ongoing weak demand and rising uncertainty ahead of the Budget prompted retailers to scale back both hiring and investment. Alpesh Paleja, Deputy Chief Economist at the CBI said, “Retailers continue to grapple with a long spell of weak demand, as households remain cautious around day-to-day spending.”

However, as the dust settled on the Budget, Black Friday saw UK shoppers spending an average of £430 each, £91 more than last year, according to Barclays. This brings total predicted expenditure of over £10.2bn. The research shows 43% of adults sought deals, with participation being highest among Gen Z, with 76% planning to shop. Rohan Kumar, Head of Barclays Spend Insights said, “Our historicaltransaction data proves that Black Fridayremains a vital retail milestone… October’sslowdown was potentially a signal thatthis year’s sale will outperform 2024, aftershoppers held out for discounts and deals.”

Here to help Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (3 December 2025)

ONS data reveals the UK economy barely expanded across Q3, with the economy contracting by 0.1% in September alone

The Monetary Policy Committee voted to leave Bank Rate on hold by a 5–4 majority in November

The headline index from last month’s GfK consumer confidence survey fell two percentage points

OBR downgrades UK growth forecasts

New projections from the Office for Budget Responsibility (OBR) predict the UK economy is set to grow at a slower rate than previously expected.

The independent fiscal watchdog’s latest economic assessment was produced for the Autumn Budget which Chancellor Rachel Reeves delivered on 26 November. During her speech, the Chancellor noted that the OBR had increased this year’s growth estimate to 1.5% from March’s figure of 1.0%, with the upgrade reflecting stronger-than-expected activity during the first quarter of the year.

Over each of the remaining five years of the forecast period, however, the updated figures suggest the economy will grow by 1.5% on average, a 0.3 percentage point reduction from the OBR’s previous assessment due to reduced expectations for productivity growth.

Prior to the Budget, Office for National Statistics (ONS) data revealed that the UK economy barely expanded across the third quarter, with the economy actually contracting by 0.1% in September alone. While this latter figure was impacted by a marked decline in motor vehicle production due to the Jaguar Land Rover cyber-attack, the data did confirm the sharp slowdown in activity that has been evident as the year has progressed.

Survey evidence also highlights a more recent loss of momentum with the preliminary headline growth indicator from the latest S&P Global UK Purchasing Managers’ Index (PMI) falling from 52.2 in October to 50.5 last month; this reading was below all predictions in a Reuters poll of economists.

S&P Global Market Intelligence’s Chief Business Economist Chris Williamson said November’s survey suggests the economy “has stalled,” with the flash data implying “a meagre 0.1%” quarterly pace of growth in the fourth quarter so far. While acknowledging that some of the malaise may have been caused by delayed spending ahead of the Budget, Mr Williamson added there was “a real chance this pause may turn into a downturn.”

Interest rates held; but more cuts expected

Although last month did see the Bank of England (BoE) maintain interest rates at their current level of 4.0%, a tight vote and policymaker comments after the announcement suggest further rate cuts are likely in the coming months.

At its latest meeting, which concluded on 5 November, the BoE’s Monetary Policy Committee (MPC) voted to leave Bank Rate on hold by a 5–4 majority, with all four dissenting voices preferring to see an immediate quarter-point reduction. This close vote, along with signs that BoE Governor Andrew Bailey might be persuaded to switch allegiance and join those seeking a cut, however, did raise the prospect of further easing soon.

Speaking after announcing the decision, Mr Bailey reiterated his view that Bank Rate remains on a “gradual downward path.” He also suggested current market pricing – which implies two or three quarter-point cuts by the end of next year – was a “reasonable view” for the future path of interest rates. Despite feeling inflation has now peaked, though, the Governor said he saw “value in waiting for further evidence” of slowing price growth before reducing rates again.

Two weeks after the MPC meeting, ONS published October’s official inflation statistics which revealed an annual headline CPI rate of 3.6%. This reading was down from September’s 3.8% figure, with prices in October increasing at their slowest pace for four months, raising hopes that inflation has now peaked.

Analysts typically expect to see a further cooling of inflationary pressures over the next few months, which could then pave the way for more interest rate cuts. Indeed, a recent Reuters poll found that 80% of surveyed economists are now forecasting a quarter-point rate reduction at the MPC’s next meeting on 18 December, with a majority of respondents predicting a similar-sized cut during the first quarter of next year too.

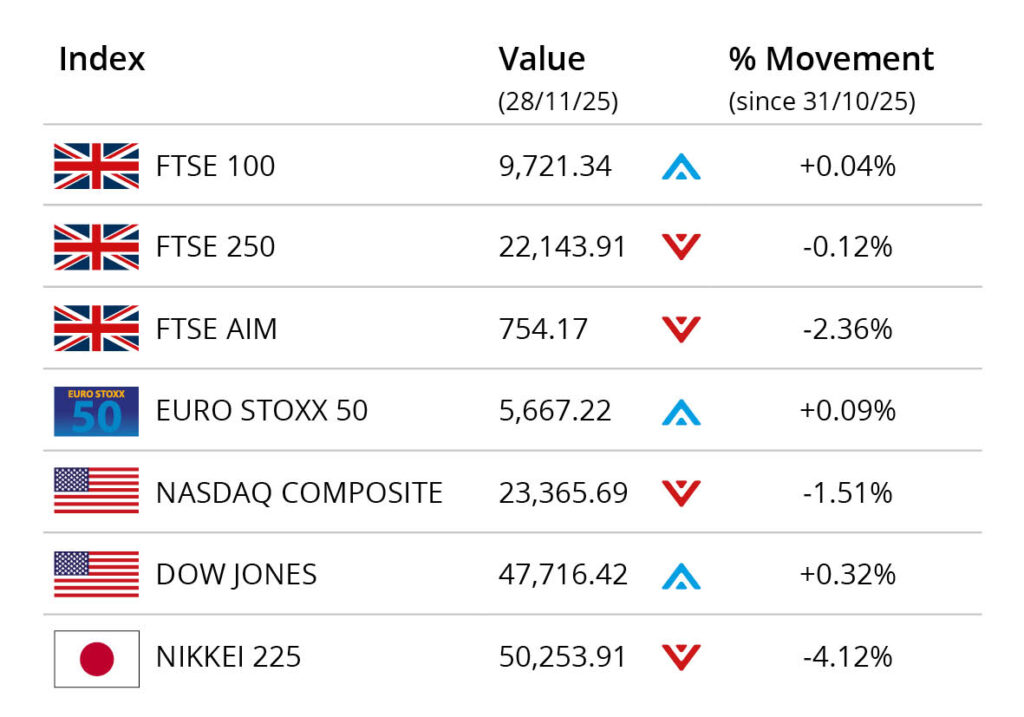

Markets

At the end of November, global stocks ticked higher as Black Friday sales continue to provide support and traders focus on the Federal Reserve’s upcoming December meeting, as hopes of an interest rate cut intensifying. Optimism around AI helped drive tech stocks before the US market closed for the Thanksgiving holiday.

In the UK, the blue-chip FTSE 100 closed the month on 9,721.34, a small gain of 0.04%. The mid-cap FTSE 250 recorded a small loss of 0.12% in November to end on 22,143.91, while the FTSE AIM registered a 2.36% loss to close the month on 754.17. On the continent the Euro Stoxx 50 gained 0.09% during November to close on 5,667.22. In Japan, the Nikkei 225 finished the month 4.12% lower to close on 50,253.91,

The Dow Jones closed the month on 47,716.42, a small increase of 0.32% in the month. The tech-focused NASDAQ closed the month down 1.51% on 23,365.69.

On the foreign exchanges, the euro closed the month at €1.14 against sterling. The US dollar closed at $1.32 against sterling and at $1.15 against the euro.

The gold price rose 5.28% during November, closing at around $4,221 a troy ounce, with expectations of a Fed rate cut in December providing support. Brent Crude closed the month at around $63 a barrel, recording a loss of 1.26% in the month. The oil price recorded a fourth consecutive monthly loss, as over supply concerns weigh.

Jobs market continues to weaken

Official labour market statistics released last month revealed a further cooling in the UK jobs market, with the unemployment rate up, the number of payrolled employees down and wage growth also edging lower.

According to the latest ONS figures, the UK rate of unemployment stood at 5.0% between July to September 2025; this represents a notable jump from a figure of 4.8% across the previous three-month period. The increase was above analysts’ expectations and left the unemployment rate at a post pandemic high.

In addition, a further fall in employee numbers was also revealed in the data, with estimates suggesting the total number of payrolled employees fell by 32,000 in October. This drop followed a similar-sized fall in September, resulting in the largest recorded two-month decline since late 2020.

The release also showed that the annual rate of growth in employees’ average regular earnings stood at 4.6% in the third quarter. While this was in line with analysts’ expectations, it did represent a slight dip from 4.7% during the three months to August. Commenting on the month’s data as a whole, ONS Director of Economic Statistics Liz McKeown said, “Taken together, these figures point to a weakening labour market.”

Retailer and consumer sentiment both down

The latest official retail sales statistics revealed a decline in sales volumes during October, while surveys reported a drop in both retailer and consumer morale ahead of the Autumn Budget.

Data recently published by ONS showed that total retail sales volumes fell by 1.1% in October. This represents the first month-on-month sales decline since May and surprised economists with a Reuters poll predicting sales would be flat. ONS noted that supermarket, clothing and mail order sales all fell in October, which some retailers attributed to delayed spending ahead of November’s anticipated Black Friday discounts.

More recent survey data also suggests the retail environment remains tough. The headline index from last month’s GfK consumer confidence survey, for instance, fell two percentage points to -19, with the company’s consumer insights director Neil Bellamy describing November’s figures as “a bleak set of results.”

In addition, the latest CBI Distributive Trades Survey reported the steepest fall in retailer sentiment for 17 years, with November’s sales typically judged to be “poor” by seasonal norms and demand expected to remain subdued heading into December. Alpesh Paleja, the CBI’s Deputy Chief Economist, said retailers continued to grapple with “weak demand” as households remain “cautious around day-to-day spending.”

All details are correct at the time of writing (01 December 2025)

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for information only. We cannot assume legal liability for any errors or omissions it might contain. No part of this document may be reproduced in any manner without prior permission.

Buyers are willing to pay a premium for a home with a sea view

One million UK homes have risen in value by at least 50% since 2020

6.5 million homeowners in the UK have some regrets about the property they bought

Buyers pay more for a sea view

Buyers are willing to pay a premium for a home with a sea view, with these properties costing £88,106 more1. Even homes in coastal areas are not priced as high if they aren’t in sight of the sea. Buyers will pay the most for a sea view in the East Midlands region (including Lincolnshire coast), where this feature could add 68% to the price. The area with the most sea view properties on the market is Torbay in Devon.

The homes that have risen in value by 50%

Analysis2 has found that one million homes in the UK have risen in value by at least 50% since 2020. Most of these properties are in the North West, Yorkshire and the Humber, and Wales. The growth is likely because these regions have become more attractive to buyers facing affordability challenges. On the other hand, half of homes in southern England have increased by 20% or less since the pandemic.

6.5 million regret their house purchase

According to research3, 37% of homeowners in the UK have some regrets about the property they bought. This feeling is more prevalent among young homeowners, as 63% of 18 to 34-year-olds wish they had done things differently. The top regret for this age group is budgeting issues, with 29% wishing they had fully considered the cost of buying or renovating.

More first-time buyers are purchasing homes later in life to manage affordability challenges

Longer mortgage terms help keep monthly payments manageable but extend debt into later years

Professional guidance can help buyers select the most suitable mortgage for their circumstances

Getting onto the property ladder has become harder in recent years and that’s had a noticeable impact. People are now buying their first homes later in life and they’re choosing longer mortgage terms to make monthly payments more manageable.

According to research1, in 2019-20 just 3.6% of first-time buyers (FTBs) with a mortgage were aged 45 or older. By 2023-24, this figure had nearly tripled to 11.5%. Also, more borrowers are opting for longer mortgage terms. Around 84.9% of FTBs are taking out mortgages that are 25 years or more, while nearly one in three are signing up for 35 years or longer. This means that about 547,000 of those who stepped onto the property ladder in 2024 will still be paying off their mortgage in their 60s.

More mortgages for lower incomes

Longer terms are increasingly common because they’re often the only way that people can afford to buy a home. In July, the Bank of England advised that lenders can offer more mortgages that are over 4.5 times a borrower’s income. HM Treasury expects this to create up to 36,000 additional FTB mortgages over the first year.

What’s right for you?

We can advise you on the most suitable mortgage for your individual circumstances. It’s a big step and a major expense in your life, we can provide the knowledge and support you need to make the right decision for you.

1Sprive, 2025

As a mortgage is secured against your home or property, it could be repossessed if you do not keep up mortgage repayments.

Growth forecasts rise to 1.5% this year, with steady medium-term expectations supporting economic stability and resilience

Income tax, NICs and IHT thresholds remain frozen to 2031, increasing the long-term tax burden on households

Cash ISA limits fall to £12,000 for under 65s but overall allowance remain the same

“We are rebuilding our economy”

Chancellor of the Exchequer Rachel Reeves delivered her second Budget on 26 November, declaring “We are rebuilding our economy.” The fiscal update includes a series of new tax and spending measures – some of which had been announced or trailed prior to Budget day – described as “the right choices for a fairer, a stronger and a more secure Britain.” In total, the Budget will raise £26bn in taxes by 2029/30.

Economic forecasts

Ms Reeves began her statement by acknowledging the Office for Budget Responsibility’s (OBR’s) technical error in releasing its Economic and Fiscal Outlook earlier than planned. The document’s accidental release effectively detailed the Budget’s key contents before the Chancellor stood at the dispatch box to deliver her statement, a move Ms Reeves described as “deeply disappointing.”

The Chancellor then confirmed that the Budget will see an expansion of the buffer for meeting the government’s fiscal targets, with the amount of headroom more than doubling from last year’s figure of £9.9bn to £21.7bn. During her speech, Ms Reeves also noted that the Budget kept “every single one” of Labour’s manifesto pledges on tax, with both her fiscal rules maintained without the need for “austerity” or “reckless borrowing.”

While the Chancellor noted that the OBR’s economic growth forecast for this year had been increased from 1.0% to 1.5%, growth is expected to be 1.4% in 2026, and 1.5% across each of the following four years. In terms of consumer prices, the Chancellor noted thatOBR calculations show “inflation is coming down faster” and, “as a direct result of this Budget,” will be “a full 0.4 percentage points lower next year.” The OBR predict CPI inflation of 3.5% this year and 2.5% in 2026.

Personal taxation, savings, wages and pensions

The government is maintaining the Income Tax Personal Allowance at £12,570 and higher rate threshold at £50,270, for an additional three years to April 2031. National Insurance thresholds are also frozen until 2031

The starting rate of Income Tax for savings will be retained at £5,000 for 2026/27 and will stay at this level until 5 April 2031. The tax rate on savings income will increase by two percentage points across all bands from April 2027 but current £1,000/£500 Personal Savings Allowances continue

Separate rates of Income Tax will apply for property income. From April 2027, the property basic rate will be 22%, the property higher rate will be 42% and the property additional rate will be 47%

Inheritance Tax thresholds (IHT) – The IHT nil-rate bands are already set at current levels until April 2030 and will stay fixed at these levels for a further year until April 2031. The forthcoming combined allowance for the 100% rate of agricultural property relief and business property relief will also be fixed at £1m for a further year until 5 April 2031. This will be legislated for in Finance Bill 2025/26 and take effect from 6 April 2030

The ordinary and upper rates of tax on dividend income will increase by two percentage points from April 2026. There is no change to the dividend additional rate or the £500 annual (non-ISA) Dividend Allowance

A High Value Council Tax Surcharge on owners of residential property in England worth £2m or more will start in 2028/29, with local authorities collecting revenue on behalf of central government. The charge will start at £2,500 a year and rise to £7,500 for properties valued above £5m

From 6 April 2027 the annual Individual Savings Account (ISA) cash limit will be reduced from £20,000 to £12,000. Annual subscription limits will remain at £20,000 for ISAs until 2031, meaning you can invest the full amount in a Stocks & Shares ISA, or you can invest £12,000 in a Cash ISA, plus £8,000 in a Stocks & Shares ISA. Savers over the age of 65 will be able to save up to £20,000 in a cash ISA each year

Annual subscription limits remain at £4,000 for Lifetime ISAs and £9,000 for Junior ISAs and Child Trust Funds until 5 April 2031

To reform the Lifetime ISA, the government will publish a consultation in early 2026 on the implementation of a new, simpler ISA product to support first time buyers to buy a home. Once available, this new product will be offered in place of the Lifetime ISA

The Help to Save scheme is to be made permanent

The Venture Capital Trust (VCT) and Enterprise Investment Scheme (EIS) investment limits are increasing to £10m and £20m for Knowledge Intensive Companies (KICs) and the lifetime company investment limit is increasing to £24m and £40m for KICs. The VCT Income Tax relief will decrease to 20%. These changes will be legislated in Finance Bill 2025/26

As recently announced, the government will increase the National Living Wage by 4.1% for individuals to £12.71 an hour. The National Minimum Wage for 18 to 20-year-olds will also increase by 8.5% to £10.85 per hour and for 16 to 17-year-olds and apprentices by 6.0% to £8.00 per hour

Working age benefits will be uprated in line with the September CPI inflation of 3.8% from April 2026

As previously announced, the government has committed to maintain the State Pension Triple Lock for the duration of this Parliament, meaning that the basic and new State Pensions will increase by 4.8% in April 2026, in line with earnings growth. This means £241.30 a week for the full, new flat-rate State Pension (for those who reached State Pension age after April 2016) and £184.90 a week for the full, old basic State Pension (for those who reached State Pension age before April 2016)

There are to be changes to salary sacrifice arrangements for pension contributions, with the amount that can be sacrificed without paying NICs capped at £2,000 per employee from 2029

Members of the Pension Protection Fund (PPF) and Financial Assistance Scheme (FAS) will be protected against the impact of inflation by introducing CPI-linked increases, capped at 2.5% a year, on pre-1997 pension accruals where their original schemes provided this benefit, from January 2027.

Business measures

In her speech, Ms Reeves said, “We are sending a simple message to the world: If you build here, Britain will back you,” before making the following announcements:

A new UK Listing Relief will provide a three-year exemption from Stamp Duty Reserve Tax for companies listing in the UK

Visa reforms to help UK businesses access global talent

The British Business Bank’s (BBB’s) new five-year plan will invest at least £5bn in growth-stage funds and scale-up companies. The BBB will launch VentureLink to help pension funds invest in venture capital

Company eligibility limits for the Enterprise Management Incentives scheme will rise, giving more scale-ups the chance to join tax-advantaged share schemes

Business rates in England to be updated from April 2026, including permanently lower multipliers for retail, hospitality and leisure

The government has published a Call for Evidence (to close on 28 Feb 2026) seeking views on how the UK can provide better support to entrepreneurs

More than £1.5bn invested through the Youth Guarantee and Growth and Skills Levy to strengthen the pipeline of skilled labour, including fully funded SME apprenticeships for under-25s.

Housing and infrastructure

Announcements included:

£1.3bn from the National Housing Delivery Fund devolved to major combined authorities to unlock housing, regenerate sites and support local growth

Planning reforms, including changes to the National Planning Policy Framework (NPPF), alongside skills reform and pensions reform expected to unlock £50bn for business and infrastructure

New infrastructure projects including £890m for the Lower Thames Crossing.

Education and the NHS

Ms Reeves then turned her attention to education, noting, “this is a government on the side of our kids, who will back their potential.” Pledges include:

Free breakfast clubs expanded, with 2,000 additional schools joining the scheme in 2026/27

£18m over two years to renew up to 200 playgrounds across England

£5m for libraries in secondary schools, building on the £10m committed for primary school libraries earlier this year.

Ms Reeves also announced 250 new Neighbourhood Health Centres delivered through public investment and a new public-private partnership model, as well as £300m in digital technology upgrades to improve NHS productivity and enhance patient outcomes.

Other key points

Removal of the two-child limit in Universal Credit (UC) Child Element – from April 2026

Changes to taxation of electric vehicles – including a new Electric Vehicle Excise Duty (eVED) of 3p per mile for electric cars and 1.5p per mile for plug-in hybrid cars, with effect from April 2028

Tobacco Duty rates – to increase by RPI inflation +two percentage points from 6pm on Budget day

Alcohol Duty rates – will increase in line with RPI inflation from 1 Feb 2026

Remote Gaming Duty – will increase from 21% to 40% from April 2026 and a new Remote Betting Rate at 25% within General Betting Duty will be introduced from April 2027

Student Loans – the Plan 2 repayment threshold will be frozen for three years from April 2027

Air Passenger Duty (APD) rates – uprated in line with RPI from 1 April 2027

Devolved government funding – Scottish government to receive £820m, the Welsh government £505m and the Northern Ireland Executive £370m

Defence spending – the UK to spend 2.6% of GDP on defence in 2027

Rail fares freeze – applicable to all regulated rail fares in England for one year starting from March 2026 (announced previously)

Energy prices – a package of measures to reduce average household energy bills by £150 across Great Britain from April 2026

Prescription costs – NHS prescription in England frozen at £9.90.

Closing comments

Rachel Reeves signed off her Budget saying, “In the face of challenges on our productivity, I will grow our economy through stability, investment and reform. I’ve met my fiscal rules and built our economic resilience for the future. I have asked everyone to contribute… for the security of our country and the brightness of its future, but I have kept that contribution as low as possible by reforming our tax system… making it fairer and stronger for the future.”

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding of the Budget taxation and HMRC rules and can be subject to change in future. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK; please ask for details. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are believed to be correct at the time of writing (26 November 2025)