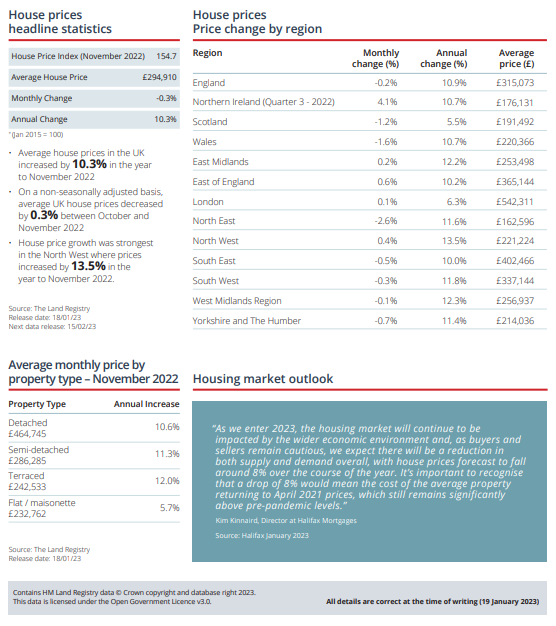

Housing market slowing but far from stopped

Supply and demand both fell in November 2022, according to the latest UK Residential Survey from the Royal Institute of Chartered Surveyors (RICS), though sales completions remained high for the month.

Transactions rose by 2.9% in November, although this is likely to include many mortgage agreements from before the September ‘mini-budget’, the RICS survey notes. Analysts expect transactions to remain at reduced levels throughout 2023.

Separate figures from the Bank of England for November 2022 show mortgage approvals 28.6% below the 2018-19 monthly average. As 2022 drew to a close, activity was falling on both sides with new instructions (-7.5%) and sales agreed (-11.5%) both below their 2018–19 average, according to TwentyCi.

Record-breaking Boxing Day sales set tone for 2023

New sellers coming to market on Boxing Day climbed by 46% year-on-year, according to Rightmove figures, with a group of motivated sellers hoping to start the new year by finding a buyer.

Valuation requests, the first step for many future sellers planning to put their house on the market, also soared after the Christmas festivities. The week commencing 26 December was the busiest week for valuation requests since early September and 29% higher than at the same time last year.

Post-Christmas clicking jumped too, a positive sign that demand for these newly-listed properties could be strong following the Christmas lull. In total, the number of views of homes for sale on Rightmove jumped by 20% between the week commencing 19 December and week commencing 26 December.

Tim Bannister from Rightmove said, “Boxing Day is traditionally the start of activity ramping up into January and the spring selling season after Christmas, as people return to their search or consider a new year move. We’ve seen some promising activity and familiar patterns over the festive period this year, which are good signs for the year ahead. After such frenetic market conditions over the last few years, this year’s calmer market will better suit measured movers who prefer to take their time to find the right property.”

Landlords still optimistic despite tougher market

More than half of UK landlords feel optimistic about the future, despite 49% admitting that market conditions have become harder in the past year, a new survey from Aldermore reveals.

In total, 54% remain optimistic for the year ahead, while 66% think that being a landlord is still a good way to make money.

Inflationary pressures, cost-of-living difficulties and housing market volatility are creating a challenging environment for landlords, analysts say.

The survey revealed that 48% have been unable to expand their property portfolio and 42% have considered downsizing if market conditions continue as they are. Significant rent rises could be on the cards as well, with 62% of landlords now saying they’ll have no choice but to put up rents by at least 10% if market conditions don’t change in the next 12 months.

Energy Performance Certificates (EPC) remain a key concern in the current market, with 58% saying that the sustainability and energy efficiency of their property portfolio is a priority.

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from, taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.