| The Bank of England cut rates to 3.75%, signalling cautious easing as inflation pressures continue to recede | Farmers gain relief as the government raises Inheritance Tax thresholds following industry backlash and sustained protests | UK markets opened 2026 strongly, with Boxing Day footfall rising and the FTSE surpassing 10,000 |

“We still think rates are on a gradual path downward”

During the Monetary Policy Committee’s (MPC’s) final meeting of 2025 on 18 December, the members voted to reduce Bank Rate to 3.75%, though it was a close call. Five of the nine members voted to reduce the rate, while four wished to retain it at 4%.

The reduction was widely expected following inflation data which showed a slowing to 3.2% in the year to November. While still well above the 2% target, the Bank of England (BoE) expects inflation to move towards target faster than previously outlined. Minutes of the latest MPC meeting state that, ‘the risk from greater inflation persistence has become somewhat less pronounced,’ but medium-term risks to inflation due to weaker demand are still present. Moving forward, it was highlighted that any potential further monetary policy easing will be dependent on the inflationary outlook.

After the announcement, BoE Governor Andrew Bailey commented, “We still think rates are on a gradual path downward but with every cut we make, how much further we go becomes a closer call.”

The first MPC meeting of 2026 is scheduled to conclude on 5 February.

Changes to Inheritance Tax (IHT) for farmers

On 23 December, the government issued a press release outlining an increase in the Agricultural and Business Property Reliefs threshold from £1m to £2.5m, with effect from April 2026. The U-turn comes on the back of protests by farmers, following the announcement in the Autumn Budget 2024 to impose a 20% tax on inherited agricultural assets worth more than £1m from April 2026, bringing an end to 100% tax relief. Environment Secretary Emma Reynolds commented on the change, “We have listened closely to farmers across the country and we are making changes to protect more ordinary family farms.” She continued, “It’s only right that larger estates contribute more, while we back the farms and trading businesses that are the backbone of Britain’s rural communities.”

The release states that the change to the threshold will allow ‘spouses or civil partners to pass on up to £5m in qualifying agricultural or business assets between them before paying Inheritance Tax, on top of existing allowances.’

President of the Country Land and Business Association believes the government’s change will “come as an enormous relief to thousands of family farms across the country who faced seeing their businesses taxed out of existence” However he did caution that while a positive step, it only “limits the damage – it doesn’t eradicate it entirely,” especially for families who own “enough expensive machinery and land… valued above the threshold” but who operate on narrow profit margins, making the tax burden still “unaffordable.”

Spring Forecast date announced

Just before the festive break, Rachel Reeves announced the date of the Spring Forecast – 3 March 2026. As usual with key fiscal events, the Chancellor has asked the Office for Budget Responsibility (OBR) to prepare an economic forecast for publication alongside the statement in early spring. This will provide an interim update on public finances and the economy, not a measure of the government’s performance versus the fiscal mandate. The government were keen to reiterate that, they are committed to delivering one major fiscal event each year – at the Budget, typically held in October or November, they say this approach provides businesses and families with ‘the stability and certainty they need,’ whilst also supporting the government’s agenda for growth.

Boxing Day footfall on the up

Figures from MRI software, retail tech experts, show Boxing Day performance was robust, with footfall up 4.4% year-on-year, the strongest increase in over a decade. Footfall in retail parks was strongest, with an 8.8% uptick, high streets followed with a 3.6% increase and shopping centres 2.1%. An increase in footfall does not necessarily equate to an increase in consumer spending.

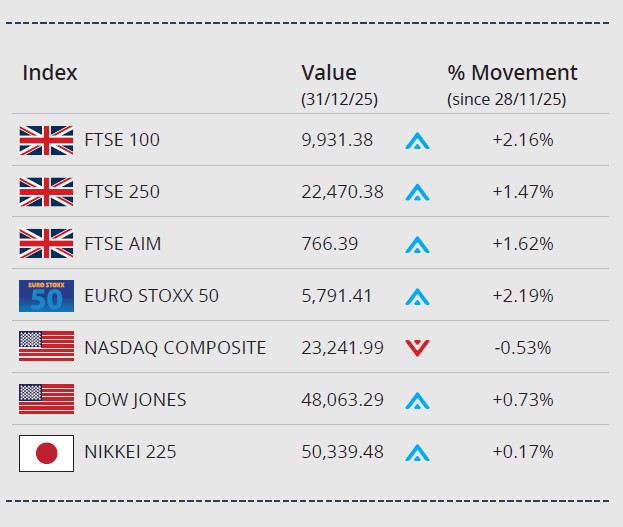

FTSE pushes through 10,000 mark

Following solid annual gains in 2025, where the FTSE 100 ended the year over 20% higher, the index passed through the historic 10,000 mark on the first day of trading in 2026 (2 January) but failed to close above it. However, on Monday the index closed above the 10,000 for the first time, on 10,004.57.

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (7 January 2026)