Many UK adults don’t feel confident their family would be financially secure if they unexpectedly died

Women were less certain about their family’s financial resilience and 45-54-year-olds were the least confident age group

A survey found that only four in 10 working people aged 60-69 feel ready for retirement

Would your family be financially resilient without you?

Only one in five people in the UK feel very confident their family would be financially secure if the unexpected were to occur, according to new research1 that warns of a lack of financial resilience. Some 35% believe their family could ‘manage for a while,’ the research revealed, but almost a quarter weren’t confident at all that their loved ones would cope.

Women (49%) were less certain their family would be secure than men (67%), while employees at large companies were more confident than their peers at small businesses. The least confident age cohort were those between 45 and 54, of whom one in three said their family would not manage financially.

Older workers ‘not prepared’ for retirement

What steps do you need to take before starting your retirement? Does it still feel like an uphill battle to get everything ready? If so, you’re not alone: only four in 10 working people aged 60-69 feel ready for retirement, a new survey2 has found.

Of the more than three million workers in that age bracket, more than a third say they do not feel prepared. Currently, one in three people aged 65 to 69 are yet to retire, of whom 31% still feel unprepared, the survey found. Preparing for life after work brings many challenges and can feel like a series of difficult decisions. Choosing when to retire and managing the transition to your new lifestyle are both significant choices.

1The Exeter, 2025, 2Just Group, 2025

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. The Financial Conduct Authority does not regulate Will writing, tax and trust advice and certain forms of estate planning.

In its first meeting of the year, the Monetary Policy Committee voted to retain Bank Rate at 3.75%

According to Halifax, the average house price has surpassed £300,000 for the first time

S&P Global data shows that the UK services sector experienced strong growth in January

“We now think that inflation will fall back to around 2% by the spring”

In its first meeting of the year, the Monetary Policy Committee (MPC) voted to retain Bank Rate at 3.75%. The MPC was split over the decision, with five members opting to hold the rate and four voting to reduce it to 3.5%.

A rate reduction was last made in December 2025, so many analysts were not anticipating a further reduction this month. Andrew Bailey, Governor of the Bank of England (BoE), commented on the decision, “We now think that inflation will fall back to around 2% by the spring. That’s good news. We need to make sure that inflation stays there, so we’ve held interest rates unchanged at 3.75% today. All going well, there should be scope for some further reduction… this year.”

The BoE expects subdued economic growth in 2026, revising its predictions for UK GDP growth down from 1.2% to 0.9%. Additionally, the unemployment rate is expected to weaken this year due to loosening labour market conditions.

The European Central Bank (ECB) also held interest rates last week. Policymakers for the eurozone have not needed to make cuts since June 2025 due to better-than-expected economic growth and easing inflation. In a press conference, ECB President Christine Lagarde said, “We are in a broadly balanced situation at the moment.” Lagarde was not concerned about the depreciating dollar; she noted that it has been fluctuating since the summer, so the impact of the foreign exchange rate is incorporated in the baseline.

Average house price ticks above £300,000

Data from Halifax shows that the average UK house price has risen above £300,000 for the first time. In January, property prices increased monthly by 0.7%, following a dip of 0.5% in December. Meanwhile, annual growth increased from 0.4% to 1.0%, bringing the average UK property to £300,077.

Halifax noted that the regional difference in house prices has become more distinct. In northern parts of the UK, demand and house price growth remain strong, but prices have slightly dropped in southern regions where buyers continue to face higher borrowing costs. Head of Mortgages at Halifax, Amanda Bryden, commented, “Affordability is still a challenge, but stronger wage growth and falling mortgage rates have helped relieve some of the pressure in recent years. We expect that improvement to continue in 2026, meaning that with the right support and advice, home ownership should become a realistic prospect for more would-be buyers.”

UK services sector strengthens

The UK services sector showed strong growth in January, according to S&P Global. The UK services PMI business activity index increased to 54.0 last month, up from 51.4 in December. This is positive news as any reading above 50.0 indicates the sector is growing. It’s also the fastest rate of growth since August 2025. The report noted that ‘higher levels of business activity were linked to greater confidence among clients, new project starts and a post-Budget improvement in investment sentiment. However, there were also many reports that geopolitical uncertainties and fragile consumer demand had weighed on growth in January.’

Business confidence improves

A survey by the Institute of Directors (IoD) found that confidence among businesses improved significantly in January. Optimism about prospects for the UK economy rose to -48 last month; while this is still in negative territory, it is a notable increase from -66 in December 2025. Business leaders’ confidence in their own organisation also improved, rising monthly from -4 to +14. Anna Leach, IoD Chief Economist, commented, “After record weakness last year, January saw a welcome – and fairly chunky – rise in the confidence of business leaders.” She added, “Overall, there’s a sense that, while revenues and general conditions have stabilised, businesses are not yet ready to increase either their capital or labour costs materially.”

Japan markets rally

Japan’s stocks surged after Sanae Takaichi secured a historic election victory, boosting investor confidence. Markets reacted positively to expectations of economic continuity and pro-growth policies, with analysts saying the result reduced uncertainty and supported optimism about Japan’s financial outlook.

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (11 February 2026)

Landlords face reduced rental profitability as Income Tax on property earnings rises by two percentage points

The Lifetime ISA will be phased out and replaced by a simpler product

High-value homeowners may reconsider property decisions as new Council Tax surcharges target homes over £2m

Although November’s Budget announcements may now feel like a distant memory, several measures introduced at the time remain highly relevant as we enter 2026. Here’s a reminder of the key changes that could affect you:

Landlords – new rental income rules

Landlords will see additional pressure from tax changes. From April 2027, Income Tax on rental earnings will go up by 2 percentage points across the board, raising the basic, higher and additional rates on property income to 22%, 42% and 47% respectively. For many buy-to-let investors, this will reduce after-tax rental yields, adding to the ongoing cost pressures.

Lifetime ISA to be replaced

The government has announced its intention to reform the Lifetime Individual Savings Account (LISA). A consultation on reforms is due in early 2026, with the aim of implementing ‘a new, simpler ISA product to support first-time buyers to buy a home.’ This marks a significant change for first-time buyers, who have relied on the LISA’s tax-benefits and the government bonus as a route to home ownership.

Council Tax changes

This has been dubbed by some as a ‘mansion tax’ and will apply from April 2028 to homes worth £2m or more in 2026. Owners (rather than tenants, who remain liable for Council Tax) of such properties will face a High Value Council Tax Surcharge (HVCTS) of £2,500 per year, rising to £7,500 for properties worth £5m or more.

Only a small fraction, around 0.5% of homes nationwide, are expected to be directly affected, with the greatest concentration in London and the South East. The measure may, however, have some impact on the wider market.

As a mortgage is secured against your home or property, it could be repossessed if you do not keep up mortgage repayments.

This article provides general tax information, tax treatment depends on individual circumstances and may change in the future.

Even small increases in pension contributions can substantially enhance retirement savings through compound investment growth

Modest, consistent contributions over a career significantly boost long-term financial security and quality of retirement life

Do your future self a favour with a one-off lump sum payment or incremental monthly increases.

Everyone knows that a healthy pension pot is crucial for a comfortable retirement. For some workers, however, saving for retirement can seem like a low priority compared to making mortgage payments, saving for a house deposit or keeping up with monthly bills.

Small gains

New research1shows how even a small uptick in pension contributions can go a long way to improving your quality of life in retirement. Modest increases in pension savings, combined with the power of compound investment growth, can soon add up.

For example, the research highlights – if a 22-year-old with a salary of £25,000 were to pay the minimum auto-enrolment contributions (5% employee, 3% employer) throughout their career, they could build an inflation-adjusted pension pot of around £210,000 by the time they turn 68. In this scenario, if monthly contributions were increased from 5% to 7%, come retirement age, they would have a pot of £262,000, a boost of over £50,000.

A gift to your future self

More than three in 10 UK adults are already increasing their workplace pension contributions beyond the minimum level. Meanwhile, one in ten have made a one-off lump sum payment. Whether monthly or ad hoc, boosting your pension savings is worthwhile – your future self will thank you.

1Standard Life, 2025

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

Figures are examples only, based on assumptions. Actual outcomes will differ and are not guaranteed

Keir Starmer claims China visit successful in rebuilding ties and securing visa-free travel and whisky tax cuts

The government has revised its business rates following a backlash from pubs and music venues

The Lifetime ISA is expected to be replaced by a new product due to launch in April 2028

“China is a vital player on the global stage and it is vital that we build a more sophisticated relationship”

Keir Starmer visited China last week, becoming the first British Prime Minister to meet with President Xi Jinping in eight years. Britain’s relationship with China has been strained over the last decade, but Starmer is one of many European leaders currently seeking to rebuild ties.

US President Trump’s policies are causing some uncertainty in Europe; as China is the world’s second-largest economy, Starmer’s meeting with President Xi is an attempt to regain some stability for the UK. During the meeting, Starmer told President Xi, “China is a vital player on the global stage and it’s vital that we build a more sophisticated relationship where we can identify opportunities to collaborate, but of course, also allow a meaningful dialogue on areas where we disagree.”

Starmer was positive about the meeting’s outcome, announcing that UK citizens will be able to travel visa-free to China for up to 30 days. Additionally, Import Tax on whisky sold from the UK to China will halve from 10% to 5%, plus AstraZeneca confirmed plans to invest $15bn in China by 2030. These developments are expected to support UK economic growth and improve business opportunities in China. However, the visit has drawn criticism from some Conservative MPs who have raised concerns about China’s human rights record and its support for Russia.

The latest on US interest rates

Last week, the US Federal Reserve voted to hold interest rates, which currently stand in a range between 3.5% and 3.75%. It is the first time since July that there has not been a cut to rates. The US Central Bank has been under pressure from President Trump to rapidly cut rates, but policymakers have raised concerns about elevated inflation. In a press conference, the Fed’s Chair, Jerome Powell, stressed the importance of the central bank maintaining its independence.

Powell’s term is due to end in May, so Trump has nominated Kevin Warsh to replace him. Warsh is a former Federal Reserve Governor who has openly criticised the central bank, calling for a “regime change.” He also appears to be more supportive of lower interest rates.

U-turn on business rates for pubs

The government has revised its business rates reforms following backlash from pubs and music venues. In the Autumn Budget 2025, Chancellor Rachel Reeves announced major increases to business rates. UKHospitality identified that pubs would be disproportionately affected by the revaluation, with the average pub’s rates projected to be £4,500 higher in 2027/28. In response to this, the government has announced a support package for pubs and music venues, granting them a 15% discount on their business rates bill from April.

Adult cash ISA balances surge

Research from Paragon Bank indicates that UK savers were increasingly making use of their cash Individual Savings Account (ISA) in 2025. Between January and October 2025, collective cash ISA balances increased by £51.4bn to £430.1bn. This is likely in response to expectations that the cash ISA allowances would be reduced in the Autumn Budget, suggesting that Brits were aiming to protect their tax-efficient savings before changes come into effect.

Meanwhile, non-ISA balances fell by £8.7bn to £838.8bn between January-October 2025. Head of Savings at Paragon Bank, Andrew Wright, commented that this “reflects a growing awareness that relying on the Personal Savings Allowance alone is no longer enough for many people, especially as rates remain elevated.”

Consultation into new Lifetime ISA

The government is currently reviewing the existing Lifetime ISA (LISA) with a replacement product expected to launch in April 2028. The details are yet to be announced, but it is anticipated that the new LISA will be aimed specifically at first-time buyers (FTBs), a move away from the current design, which is intended for both FTBs and retirement savers. At the moment, the government pays LISA savers a 25% bonus on monthly contributions, up to £1,000 annually. However, the new model would likely change to a single lump sum bonus paid on completion of the house purchase. There are also discussions about removing the penalty for withdrawing money that does not go towards a property.

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (4 February 2026)

Check your home is protected against bad weather, such as freezing temperatures, high winds and heavy downpours

Insurers paid out £585m for weather-related damage to homes and possessions in 2024, so check you’re adequately covered

Make sure your boiler is serviced annually, identify fire hazards in your home and test smoke alarms.

Frozen pipes. Blocked gutters. Damp rooms. The winter months can take their toll on your home – and your health. Here are some top tips to keep you and your property safe.

Weather the storm

Make sure your home is protected against bad weather, such as freezing temperatures, high winds and heavy downpours. Watch out for a build-up of debris in gutters and drains, insulate any outdoor taps and pipes, and safely store garden items.

Insurers paid out a record £585m for weather-related damage to people’s homes and possessions in 20241, so check you have adequate cover. Fences and gates are not always covered for storm damage, so make sure they are secured. Be prepared for floods and power cuts. You can report a power outage by calling 105 and sign up to flood alerts online.

Feel the heat

Boiler breakdowns are often excluded from standard home insurance policies, so it’s important to keep them well maintained with an annual service. If you’re concerned your boiler might not make it through the winter, then home emergency cover could provide added protection.

Try to heat your home to at least 18°C – especially if you are 65-plus or have a chronic health condition or reduced mobility. A warm, ventilated home can also help to prevent condensation and damp building up during winter months.

Don’t play with fire

A log burner or open fire can add a touch of magic to a cold dark night but remember to get your chimney swept once a year to prevent any blockages. If you use portable heaters or candles, keep them away from soft furnishings.

Take a moment to test your fire, smoke and carbon monoxide alarms to ensure they’re working properly. You could also complete an online home fire safety check to identify any hazards in your home – see your local fire brigade’s website for more details.

Make sure your home is properly insured

Winter can bring unexpected damage, having the right level of cover can save you from costly surprises. Adequate home insurance not only provides financial security but also peace of mind, so you can focus on staying warm and well, knowing your home is protected whatever the weather.

1ABI, 2025

As a mortgage is secured against your home or property, it could be repossessed if you do not keep up mortgage repayments. Financial protection policies typically have no cash in value at any time and cover will cease at the end of the term. If premiums stop, then cover will lapse.

Only 40–50% of UK’s Baby Boomers are on track to maintain their current lifestyle in retirement

Only 6% of Gen X have a written retirement plan, despite nearing the end of their working lives

Whatever your level of wealth, expert advice can help bridge the gap between retirement hopes and financial reality

The start of a new year is an ideal time to assess how ready you are for retirement, and recent research into the UK’s Baby Boomer generation (born 1946–1964) offers a timely reminder of the value of planning ahead.

The study1 found that only 40–50% of Baby Boomers are on track to maintain their current lifestyle or achieve a moderate standard of living in retirement. However, it also revealed a clear divide between those who receive financial advice and those who don’t.

Advised Baby Boomers are significantly more retirement-ready, with 83% on track to reach the Pensions and Lifetime Savings Association’s ‘comfortable’ living standard (around £50,900 a year pre-tax budget for an individual, rising to £67,500 for a couple), compared with just 68% of their non-advised peers.

Middle-income earners were found to be particularly vulnerable to falling short, while wealthier Boomers who sought professional advice were best positioned to meet their future spending needs.

Adding to concerns about inadequate retirement planning among those nearing the end of their working lives, a separate study2 found that only 6% of Gen X (born 1965–1983) have a written retirement plan, while 13% have one that isn’t documented. The vast majority admit to having only a vague plan or none at all.

Whatever your level of wealth, the findings underline a simple truth: expert advice can help bridge the gap between retirement hopes and financial reality. In an ever-changing economic landscape, regular reviews and tailored guidance remain key to ensuring lasting financial confidence.

1Vanguard, 2025, 2Just, 2025

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

UK economic momentum strengthened into 2026, with GDP rebounding and business surveys signalling improving private sector confidence

Inflation ticked higher in December, but economists expect the rise to fade as temporary factors unwind

Markets delivered solid January gains despite volatility, while labour demand softened and consumer confidence edged higher

UK growth rate stronger than expected

Official figures released last month by the Office for National Statistics (ONS) showed the UK economy bounced back strongly in November, while survey data points to a further rise in economic momentum at the start of this year.

According to the latest monthly gross domestic product (GDP) statistics, UK output rose by 0.3% in November, following a decline of 0.1% in October. This rebound, which beat economists’ expectations of a 0.1% rise, was driven by an increase in industrial output following Jaguar Land Rover’s return to full production after its cyberattack and stronger than anticipated growth from the services sector.

As monthly figures can be volatile, ONS prefers to focus on growth across a three-month rolling period and, on this measure, the latest GDP data showed the economy grew by 0.1% in the three months to November. This performance was significantly better than the 0.2% contraction economists had forecast in a Reuters poll, reflecting not only November’s upside surprise but also an upward revision to September’s growth rate.

The latest evidence from a closely-watched economic survey also provides signs of growing economic momentum, with the preliminary headline growth indicator from S&P Global’s UK Purchasing Managers’ Index (PMI) jumping from 51.4 in December to 53.9 in January. This represents the fastest overall rate of private sector expansion for just under two years.

Commenting on the survey’s findings, S&P Global Market Intelligence’s Chief Business Economist Chris Williamson said the data suggests UK businesses “kicked up a gear” in January, with firms demonstrating “encouraging resilience in the face of recent geopolitical tensions.” Mr Williamson also noted that January’s flash PMI data was indicative of “robust quarterly GDP growth approaching 0.4%” and that the survey puts optimism about the business outlook at its highest level since before the 2024 Autumn Budget.

Inflation rise likely to be temporary

Although recently published ONS data did show that the headline inflation rate rose for the first time in five months, economists do still typically expect price growth to slow sharply across the next few months.

The latest official inflation statistics revealed that the Consumer Prices Index (CPI) 12-month rate – which compares prices in the current month with the same period a year earlier – stood at 3.4% in December. This reading was up from 3.2% in November and slightly higher than the consensus view from a Reuters poll of economists.

ONS noted that tobacco and airfares were the biggest contributors to December’s rise. In both cases, though, the change in prices was largely driven by one-off factors like an increase in duty charged on tobacco products forcing the CPI rate higher.

Despite December’s rise, most economists expect inflation to slow sharply over the coming months. Indeed, Bank of England (BoE) Governor Andrew Bailey has previously stated his belief that the headline CPI rate is likely to be sitting close to the Bank’s 2% target by April or May this year.

Not all members of the BoE’s nine-strong interest-rate-setting Committee, however, agree with the Governor’s analysis. Megan Greene, for example, recently reiterated that she remains concerned about how much businesses might raise wages this year and the challenge that could pose to the Bank hitting its inflation target.

The outcome of the BoE’s next interest rate deliberations is due to be announced on 5 February. A recent Reuters poll found that an overwhelming majority of economists expect Bank Rate to be held steady at that meeting; a slim majority of respondents though did predict a further 25 basis point cut to be sanctioned at the Committee’s following meeting in March.

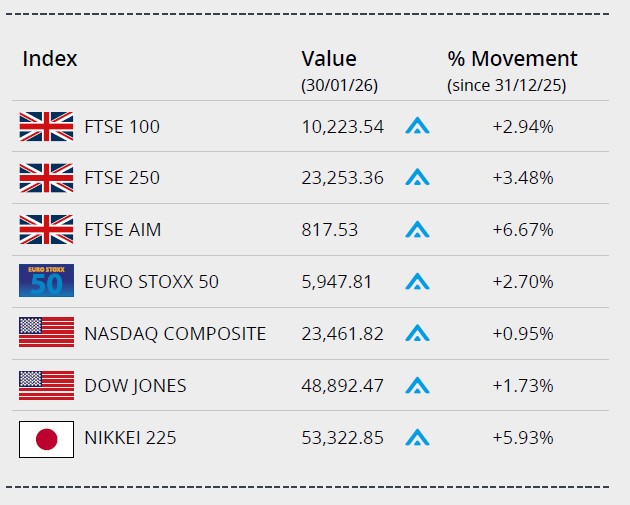

Markets

Global indices closed the month in positive territory, despite some volatility at month end.

On 30 January, President Trump nominated former Federal Governor Kevin Warsh to succeed Jerome Powell as Chairman. The news prompted the price of metals to trade sharply lower as investors repriced their outlook for monetary policy. US equities, which reached highs earlier in the week, also pulled back on the news.

The Federal Reserve voted to retain rates in the last week of the month. Expectations are for further cuts as the year progresses.The Dow Jones closed up around 1.73% on 48,892.47. The NASDAQ registered a modest monthly gain of 0.95% to close on 23,461.82.

In the UK during January, the FTSE 100 passed the 10,000 mark for the first time and closed the month almost 3% up – on 10,223.54. Meanwhile, the FTSE 250 ended January 3.48% higher on 23,253.36 and the FTSE AIM registered over 6.6% to close the month on 817.53.

Data published at month end showed economic growth at the end of 2025 in the eurozone had surpassed expectations and unemployment fell. The Euro Stoxx 50 closed January 2.7% higher on 5,947.81. In Japan, the Nikkei 225 ended January on 53,322.85, gaining over 5.9% in the month.

On the foreign exchanges, the euro closed the month at €1.15 against sterling. The US dollar closed at $1.37 against sterling and at $1.18 against the euro.

Brent Crude closed January at around $65 a barrel, recording a monthly gain of over 7%. Concerns around heightened geopolitical tensions have provided support, although the price retreated at month end. Gold closed the month trading around $4,936 a troy ounce, a gain of over 13% in January. The price slid at month end as the news of Warsh’s nomination weighed on the precious metal and the stronger dollar impacted.

Jobs market remains subdued

The most recent set of labour market data has provided more evidence of a softening in the UK jobs market, with the number of employees on firms’ payrolls falling and pay growth edging lower.

Statistics released last month by ONS showed demand for workers continues to wane, with provisional tax data for December revealing a 43,000 monthly fall in the number of people in payrolled employment; this follows a 33,000 drop in November. ONS noted that this decline was concentrated in retail and hospitality reflecting “’weak hiring activity’ in these sectors.

The data release also revealed a further slowdown in wage growth with average weekly earnings, excluding bonuses, rising at an annual rate of 4.5% in the three months to November, a slight dip from 4.6% in the previous three-month period. This easing was entirely due to a sharp slowdown in private sector pay increases, which dropped to their lowest level in five years.

Survey evidence also points to more recent weakness. Data from Adzuna’s latest survey, for instance, showed that ‘competition for roles intensified and hiring slowed’ across many sectors in December, while UK PMI data suggests ‘the pace of job losses accelerated’ across the private sector in January.

Surprise rise in retail sales

Last month’s official retail sales statistics revealed an unexpected rise in sales volumes, while survey evidence shows consumer confidence edged up to its highest level since August 2024.

The latest ONS data showed total retail sales volumes grew by 0.4% in December, surprising economists who had predicted a slight fall. This rise represents the first monthly increase since September and marked a brighter end to an otherwise disappointing final quarter, with volumes falling by 0.3% across the last three months of 2025 compared to the previous quarter.

ONS said internet retailing performed well in December, with online jewellers enjoying a particularly strong month boosted by high demand for gold and silver, while there was also a small rise for supermarkets and sales of automotive fuel. Non-food stores, such as department, clothing and household stores, fared less well though, with sales across this sector down 0.9%.

Encouragingly for retailers, last month’s GfK survey did report further improvement in consumer morale, with its headline sentiment index rising one point to -16. January’s data did, however, mark ten years since consumer confidence was last in positive territory, and GfK Director Neil Bellamy admitted, “we remain a long way from consumers feeling that better days are around the corner.”

All details are correct at the time of writing (02 February 2026)

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for information only. We cannot assume legal liability for any errors or omissions it might contain. No part of this document may be reproduced in any manner without prior permission.

Start thinking about making the most of tax-efficient opportunities before the end of the 2025/26 tax year

You can contribute as much as you like into your pension, but there’s a limit on the amount of tax relief you will receive each year

You can make gifts worth up to £3,000 in each tax year, these gifts will be exempt from IHT on your death, even if you die within 7 years

As the end of the 2025/26 tax year approaches, it’s the ideal time to ensure you’re making the most of tax-efficient opportunities before the new financial year begins on 6 April 2026. Here’s a reminder of three of the main tax planning opportunities:

Your Individual Savings Account (ISA)

The ISA allowance is £20,000 for the 2025/26 tax year. You can put all the £20,000 into a Cash ISA (until the allowance is cut in 2027), or invest the whole amount into a Stocks and Shares ISA. You can also mix and match as long as the combined amount doesn’t exceed your annual ISA allowance. Junior ISAs work in the same way but the maximum annual investment is £9,000 per child.

Your pension

You can contribute as much as you like into your pension, but there is a limit on the amount of tax relief you will receive each year. The Annual Allowance is currently £60,000. An individual can’t use the full £60,000 Annual Allowance where ‘relevant UK earnings’ are less than £60,000, although your employer still could. You may be able to carry forward unused allowances from the past three years, provided you were a pension scheme member during those years. For every £2 of adjusted income (total taxable income including all pension contributions) over £260,000, an individual’s Annual Allowance is reduced by £1 until the minimum Annual Allowance of £10,000 is reached.

Gifting for IHT purposes

You can make gifts worth up to £3,000 in each tax year. These gifts will be exempt from IHT on your death, even if you die within seven years. You can carry forward any unused part of the £3,000 exemption to the following year but if you don’t use it in that year, the exemption will expire. Certain gifts don’t use up this annual exemption, however, there is still no IHT due on them e.g. wedding gifts of up to £5,000 for a child, £2,500 for a grandchild (or great grandchild) and £1,000 to anyone else. Individual gifts worth up to £250 per recipient per tax year are also IHT free. Under current HMRC rules, gifts outside the above categories normally cease to count for IHT purposes upon the donor’s survival for seven years, with reductions in the event of death after at least three years.

And don’t forget about Capital Gains Tax (CGT) and your Divided Allowance! Time for an end of tax year review?

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

Trump “won’t use force” to seize Greenland –which came as a relief to global leaders and markets, after a challenging period

With geopolitical risk dominating, WEF President cautioned that tensions could have a detrimental effect on global growth

Price pressures are set to ease noticeably this year, particularly as the impact of last year’s energy and utility price hikes fades away

“Europe needs to adjust to the new security architecture and realities that we are now facing”

Last week, global leaders met in Davos for the World Economic Forum Annual Meeting 2026. Talks were focused on rising geopolitical and economic tensions, including the Russia-Ukraine conflict and the fast-moving situation in Greenland.

On Wednesday 21 January, President Trump delivered a special address, touching on US economic growth, immigration and Greenland. He stated that he is “seeking immediate negotiations to… discuss the acquisition of Greenland by the United States.” Trump had previously threatened to use military force to take control of the island, however he said that he “won’t use force,” which came as a relief to global leaders and markets, after a challenging few days.

Trump also launched his ‘Board of Peace’ initiative, to oversee peace efforts in Gaza. The Board now appears to have a broader goal of resolving conflict across the globe. Israel, Argentina and Hungary are among the countries who have signed up, while several countries have declined their invitations, including France, Norway and the UK.

European leaders emphasised the importance of unity in response to US policy shifts. French President Emmanuel Macron expressed concern over the rise of unilateralism. Meanwhile, Ursula von der Leyen, President of the European Commission said, “I believe Europe needs to adjust to the new security architecture and realities that we are now facing.” She added, “Europe must speed up its push for independence – from security to economy, from defence to democracy.”

President Zelenskyy criticised European leaders, urging them to act boldly instead of relying on US leadership. With geopolitical risk dominating discussions, World Economic Forum President Børge Brende cautioned that these tensions could have a detrimental effect on global growth. Meanwhile, AI was another key theme, with BlackRock CEO Larry Fink warning about the impact of technological advancements on the global workforce.

Inflation ticks higher

According to the Office for National Statistics (ONS), inflation rose annually by 3.4% in December 2025, up from 3.2% in November. The increase was largely driven by a sharp rise in airfares, which climbed by 28.6%. However, the ONS noted that this was mainly due to the timing of the festive period. Food prices were also an upward driver, rising by 4.5% in the 12 months to December 2025.

Lead Economist at CBI, Martin Sartorious, commented, “Inflation edged up slightly in December, broadly in line with consensus expectations. However, we anticipate that this increase will prove to be temporary. Price pressures are set to ease noticeably this year, particularly as the impact of last year’s energy and utility price hikes fades away.”

This is the final inflation figure before the Monetary Policy Committee’s next meeting on 5 February.

Gold reaches record highs

This week gold surged above $5,000 an ounce for the first time, extending a historic rally after rising over 60% last year. The latest gains come amid heightened geopolitical uncertainty, including tensions between Nato and the US. Precious metals are often viewed as safe-haven assets during periods of instability. Strong demand has been driven by persistent inflation, a weaker US dollar, increased buying by central banks and expectations that the US Federal Reserve will cut interest rates again later this year.

Consumer confidence update

According to GfK’s index, consumer confidence rose by one point in January to -16. Attitudes about personal finances over the last 12 months rose by three points to -3 (seven points higher than January 2025). Meanwhile, the measure for the country’s economic situation over the last year decreased by five points to -45 (one point higher than January 2025).

Consumer Insights Director at GfK, Neil Bellamy, said, “January 2026 brings an unwanted anniversary, marking 10 years since consumer confidence was last in positive territory. Even with a one-point increase in headline confidence this month to -16, we remain a long way from consumers feeling that better days are around the corner.”

Government borrowing falls

ONS data shows that UK government borrowing decreased in December. Public spending was estimated to be 3.5% higher than in December 2024, but this was offset by the government receiving 8.9% more in taxes. Borrowing therefore totalled £11.6bn last month, which is lower than expected and down 7.1% on the previous year.

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (28 January 2026)