Figures from the Equity Release Council revealed a 10% annual increase in borrowing in Q2 2025.

In H1 2025, making home adaptations or improvements was the top reason for using equity release.

More homeowners are taking out a lifetime mortgage to fund day-to-day living, highlighting cost of living pressures.

From property renovations to dream holidays, homeowners are increasingly using equity release to help fund later life choices.

Figures from the Equity Release Council revealed a 10% increase in borrowing in the second quarter of 2025 compared with the previous year1. Equity release enables homeowners aged 55-plus to cash in on the wealth tied up in their property.

In the first half of 2025, making home adaptations or improvements was the top reason (43%) for taking out a lifetime mortgage, followed by clearing an existing mortgage (27%), according to one customer survey2. The previous year, the results were the other way round, showing a shift in borrowers’ priorities.

Sharing the gift of property wealth

The number of homeowners taking out a lifetime mortgage to fund day-to-day living increased from 20% in 2024 to 27% last year, highlighting the impact of the cost-of-living crisis on older adults. Funding holidays (25%) and making gifts to family and friends (22%) also featured in 2025’s top five reasons.

1ERC, 2025, 2Canada Life, 2025

As a mortgage is secured against your home or property, it could be repossessed if you do not keep up mortgage repayments. Think carefully before securing other debts against your home. Equity released from your home will be secured against it. Equity release may reduce the value of your estate and affect your entitlement to meanstested benefits

77% of high-net-worth individuals began making significant charitable donations after surpassing £2m in personal wealth

High-net-worth individuals want their money to carry meaning, so philanthropy is becoming integral to wealth planning

Inheritance Tax receipts continue rising, with forecasts suggesting revenues could reach £14bn by 2030

Wealth milestones trigger significant giving

A study from Barclays Private Bank and Wealth Management1 found that for high-net-worth individuals (HNWIs), reaching certain wealth milestones often triggers charitable giving. Based on responses from 500 HNWIs, 77% began making significant charitable donations after surpassing £2m in personal wealth, while 51% started giving before reaching £1m. With a third of respondents expecting inheritances of £1m or more, philanthropic activity is likely to accelerate in the years ahead.

Head of Philanthropy at Barclays Private Bank and Wealth Management, Juliet Agnew, commented on the findings, “The view of philanthropy amongst HNW individuals in the UK is shifting to become an integral part of wealth planning. As the research shows, once individuals reach key milestones in their wealth journey, they increasingly want their money to carry meaning as well as value.”

IHT receipts continue their upward climb

Inheritance Tax (IHT) receipts show no signs of slowing, with the latest HM Revenue & Customs2 data revealing continued year-on-year growth. Between April and September 2025, IHT receipts totalled £4.4bn, around £100m more than during the same period in 2024, representing a 2.3% increase. If the current pace continues, total receipts for the 2025/26 tax year could reach approximately £8.8bn, setting yet another record. Looking ahead, the Office for Budget Responsibility (OBR) forecasts that IHT revenues could potentially rise to £14bn by the end of the decade.

1Barclays, 2025, 2HMRC, 2025

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. The Financial Conduct Authority does not regulate Will writing, tax and trust advice and certain forms of estate planning.

The Chancellor saidthe government will plot a course through the current uncertainty and “secure the economy”

Growth for this year has been revised down to 1.1%, from a prediction of 1.4% in November 2025

OBR project inflation will fall from 3.4% in 2025, to 2.3% in 2026 and then to 2% from 2027 onwards

On Tuesday 3 March, Chancellor of the Exchequer Rachel Reeves delivered her Spring Forecast, unveiling updated economic forecasts from the Office for Budget Responsibility (OBR). The Chancellor opened her statement by saying, “This government has the right economic plan for our country,” which was “even more important in a world that in the last few days has become yet more uncertain,” pointing to events in the Middle East.

She said the government will plot a course through the current uncertainty and “secure the economy through shocks.”Referring to what she described as the largest increase in defence spending since the Cold War, she reiterated her commitment to defence, providing reassurance in the light of global developments. She specifically referenced a £650m commitment made in January to upgrade Typhoon fighter jets, a new Royal Navy frigate launched in February and a recent £1bn helicopter deal.

One fiscal event

Reiterating the government’s intention to hold one key fiscal event each year – the Budget in the Autumn – Reeves said, “Stability is the single most important precondition for economic growth… limiting major policy changes to the Budget and giving businesses and households the certainty they need.”

Economic forecasts

The Chancellor outlined the OBR’s latest assessment of the UK economy, with the independent forecaster predicting continued economic expansion, but at a slower pace than previously forecast. Growth in 2026 is now expected to be 1.1%, down from a prediction of 1.4% in November 2025, before averaging 1.6% a year over the rest of the forecast period.

Unemployment

The OBR projects unemployment to peak at 5.3% later in 2026, before gradually falling throughout the forecast period and ending the Parliament at around 4.1%. The Chancellor then turned specifically to youth unemployment, saying that “this government will not leave an entire generation of young people behind.” She confirmed that the government is currently taking action by reforming apprenticeships and delivering a Youth Guarantee, with more plans to be set out in the weeks ahead.

Borrowing

In its Economic and Fiscal Outlook, the OBR forecasts that public sector net borrowing will fall from 5.2% of GDP in 2024/25 to 4.3% of GDP this year, and then to 1.6% of GDP in 2030/31. This is a slightly faster pace of decline than in the November forecast, with borrowing revised down by £8bn in 2030/31 compared to November, largely due to an improved receipts forecast.

Inflation

Setting out more of Labour’s economic record, the Chancellor said the OBR projects that inflation will fall from 3.4% in 2025 to 2.3% in 2026, and then to 2% from 2027 onwards. It also forecasts that the 2% target for the UK inflation rate will be met towards the end of 2026.

This would mean the UK meets its target sooner than originally predicted following the November Budget, where the OBR had forecast a rate of 2.5% in 2026, then 2% in the following three years.

Looking ahead

In two weeks’ time, at the Mais Lecture, the Chancellor has said she will set out “three major choices” set to determine the future course of the economy, including strengthening global relationships, breaking down trade barriers and harnessing the power of AI.

The Chancellor closed her statement saying, “If we stay the course and stick to our plan, and our debt interest rates return to the G7 average, we will have £15bn a year more for the priorities of working people and to make working people better off – that is the prize on offer, that is the prize within our grasp.“

Business response

Responding to the Chancellor’s Spring Forecast, Shevaun Haviland, Director General of the British Chambers of Commerce, said that it confirmed the Uk economy is “heading in the right direction, but further acceleration is needed. With GDP expected to grow well below 2% a year until 2030, unemployment set to rise in the near term and net trade remaining anaemic, there is more to do.”

She added, “Crucially, the OBR’s inflation forecast does not take into account the widening conflict in the Middle East and increasing disruption to oil and gas supplies and shipping. That inevitably adds a fresh element of uncertainty on prices and government borrowing.“

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are believed to be correct at the time of writing (4 March 2026)

Financial inequality leaves many women with fewer financial resources and less security in later years

One of the most significant drivers of the gender wealth gap is the difference in pension savings

There are opportunities at every stage to strengthen financial wellbeing and close the gender wealth gap

Despite decades of progress, financial inequality between men and women still exists. Differences in earnings, pensions, career breaks and investing habits can build up over a lifetime, leaving many women with fewer financial resources and less security in later years. International Women’s Day on 8 March is a powerful reminder not only to recognise these challenges, but also to take practical steps towards greater independence, confidence and control.

Financial empowerment isn’t tied to age. Whether at the beginning of a career, balancing family commitments, planning for retirement or already enjoying later life, there are opportunities at every stage to strengthen financial wellbeing and close the wealth gap.

Protecting earning power over a lifetime

Income is the foundation of financial independence, yet women often face barriers that affect their long-term earning potential. Career breaks, part-time work, caring responsibilities and health changes can all impact salary progression and pension contributions. Even today, pay inequality persists and time away from work can have a lasting effect on lifetime earnings. In fact, data from the Office for National Statistics (ONS) shows that mothers lose an average of £65,618 in pay by the time their first child turns five and are 15% less likely to be in paid employment 18 months after having a child1.

There are ways to stay in control and maintain earning power – including regularly reviewing career goals, keeping skills up to date and planning for potential life changes. Even small decisions such as returning to work part-time rather than stepping away entirely, or continuing pension contributions during career breaks, can make a meaningful difference over time.

Building retirement security early and consistently

One of the most significant drivers of the gender wealth gap is the difference in pension savings. Women tend to contribute less over their lifetimes, often due to lower earnings or time away from the workplace. Figures2 show that the pension contribution gap increases the closer you get to retirement – for women aged 40 to 44, it’s 25% and by the time you reach 55 to 59, it’s risen to 38%. As a result, many face a greater risk of financial pressure in retirement.

The key message is simple: it’s never too early, or too late, to take action. Checking for gaps in National Insurance contributions, reviewing workplace and private pensions, and understanding how much income will be needed later in life are all valuable steps. Even modest increases in contributions can grow significantly over the years.

Retirement planning isn’t just about covering basic needs. It’s about maintaining independence, enjoying hobbies and travel, and having the resources to adapt to life’s changes, from home improvements to healthcare needs.

Taking control of personal wealth

Financial independence is about more than income and pensions. It’s about having a clear picture of your overall financial position and building resources in your own name. Life can be unpredictable, and having access to savings and investments provides security if circumstances change, such as relationship breakdown, illness or bereavement.

Across all life stages, women are increasingly taking ownership of their financial futures. More are seeking professional advice, managing investments and building personal safety nets. Tax-efficient savings vehicles and long-term investment strategies can help grow wealth steadily, while protection policies can offer peace of mind.

Becoming a more confident investor

Investing remains an area where many women feel less confident, often choosing traditional savings accounts instead. More than half (52%) of UK women have never held an investment product, compared to only a third (34%) of men3.

While caution is understandable, particularly when planning for later life, leaving money in low-interest accounts can mean it loses value over time due to inflation.

Learning the basics of investing and developing a balanced approach to risk can help money work harder. Confidence tends to grow with knowledge; taking time to understand options can open up opportunities for long-term growth.

Planning for the future and for others

Financial planning is not just about the present. Thinking ahead about inheritance, later-life care and passing on wealth can help protect loved ones and ensure personal wishes are honoured. Updating wills, discussing plans with family members and understanding potential tax implications can all make a lasting difference.

Knowledge is power

Across every stage of life, the most powerful step women can take is to stay informed and engaged with their finances. From boosting earning potential and strengthening pensions to investing and planning ahead, each action builds towards greater independence.

International Women’s Day is a moment to celebrate progress, but also to recognise the importance of continued action. By building confidence, seeking advice and taking ownership of financial decisions, women can shape stronger, more secure futures for themselves and for the generations that follow.

1ONS 2Aviva 3 LV

This article provides general information only and does not constitute financial advice.

Office for National Statistics reported subdued late-2025 growth, but PMI signals stronger first-quarter expansion

Inflation fell to 3.0%, raising expectations that Bank of England may cut rates soon

FTSE 100 reached record highs as public finances posted a surprise January surplus

Survey highlights signs of encouragement

Although Office for National Statistics (ONS) figures released last month did reveal that the UK economy barely grew in the fourth quarter of 2025, a closely-watched survey suggests the economy has enjoyed a more encouraging start to this year.

The latest gross domestic product (GDP) statistics showed that UK economic output rose by 0.1% in the final three months of last year, the same lacklustre pace of growth as recorded during the third quarter. This figure was just below the consensus forecast from a Reuters poll of economists, with the underperformance partly reflecting a downward revision to November’s previously published monthly growth rate.

ONS described the overall picture of growth towards the end of last year as ‘subdued,’ noting there was no quarterly growth at all in the dominant services sector for the first time in two years. The construction sector was also weak, suffering its worst quarterly performance in four years, with the small overall fourth-quarter GDP increase driven entirely by growth from the manufacturing sector.

Evidence from a recently released economic survey, however, revealed signs of growing economic momentum across the first two months of this year, with the preliminary headline growth indicator from February’s S&P Global UK Purchasing Managers’ Index (PMI) rising to 53.9. This was a slight improvement on January’s final reading and the highest recorded level since April 2024.

S&P Global Market Intelligence’s Chief Business Economist Chris Williamson said, “The early PMI data for February bring further signs of an encouraging start to the year for the UK economy. A solid rise in output across manufacturing and services has been reported in both January and February, with the rate of expansion gaining pace. The survey data so far this year are consistent with GDP rising by just over 0.3% in the first quarter if this performance is sustained into March.”

Inflation decline boosts rate cut hopes

Release of the latest consumer price statistics showed UK headline inflation is now sitting at a 10-month low, adding to expectations that Bank of England (BoE) policymakers will sanction another reduction in interest rates soon.

Data published last month by ONS revealed the Consumer Prices Index (CPI) 12-month rate – which compares prices in the current month with the same period a year earlier – fell to 3.0% in January. While this did represent a sizeable drop from December’s figure of 3.4%, the decline was actually in line with analysts’ expectations.

ONS said January’s slowdown was partly driven by a decrease in motor fuel prices, while the food and non-alcoholic drink sector also provided downward pressure, as did airfares, with prices in this category falling back after rising in December. The data also showed that these factors were partially offset by an increase in the cost of hotel stays and takeaways.

The latest inflation figures, along with other data released last month highlighting further jobs market weakness, increased the prospect of another reduction in interest rates when the BoE’s Monetary Policy Committee (MPC) next convenes later this month. At its previous meeting, which concluded on 4 February, the nine-member panel voted to leave rates on hold, as had been widely expected. Analysts noted, however, that the narrow five to four majority was a dovish surprise.

Minutes to February’s meeting also stated that Bank Rate ‘is likely to be reduced further’ and, in recent comments to the Treasury Committee, BoE Governor Andrew Bailey confirmed that a cut in March was a possibility if further evidence of easing inflation emerges. The outcome of this month’s MPC meeting will be announced on 19 March, with a recent Reuters poll showing a majority of economists expects policymakers to vote in favour of another quarter-point cut to Bank Rate.

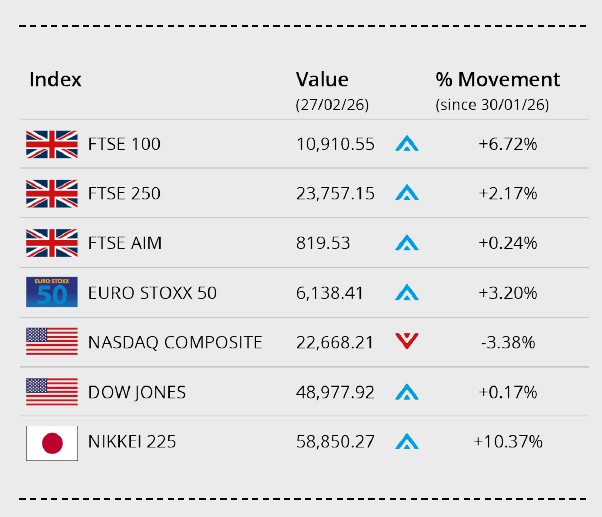

Markets

At month end, the UK blue chip FTSE 100 index outperformed US and European counterparts, closing a record-breaking week at another new high. The index closed the month up 6.72%, on 10,910.55.

Also in the UK, the mid-cap focused FTSE 250 ended February 2.17% higher on 23,757.13 and the FTSE AIM recorded a small 0.24% gain to close the month on 819.53. The Euro Stoxx 50 closed the month over 3% higher on 6,138.41. In Japan, the Nikkei 225 closed out February on 58,850.27, gaining over 10% in the month, supported by renewed optimism surrounding the Japanese economy and corporate sector.

US markets ticked lower at month end as a jump in wholesale prices fuelled concerns over a stubborn inflationary environment. The Dow Jones closed the month up around 0.17% on 48,977.92. The NASDAQ registered a monthly loss of 3.38% to close on 22,668.21.

On the foreign exchanges, the euro closed the month at €1.13 against sterling. The US dollar closed at $1.34 against sterling and at $1.18 against the euro.

Gold closed February trading around $5,251 a troy ounce, a gain of over 6% in the month, as investors seek safe haven assets – with US / Middle East developments keeping markets on edge. Brent Crude closed the month at around $72 a barrel, recording a monthly gain of over 10%. Tension between the US and Iran has heightened fears of disruption to oil flows through the Strait of Hormuz.

Public finances post record monthly surplus

The latest public sector finance statistics revealed a higher-than-expected budget surplus providing a boost for the Chancellor as she prepares to deliver her Spring Forecast.

ONS data showed that UK public sector net borrowing (the gap between the country’s overall income and expenditure) recorded a record monthly surplus of £30.4bn in January 2026. This figure, which topped all forecasts in a Reuters poll of economists, was double last January’s surplus, as stronger Income Tax, employers’ National Insurance contributions and Capital Gains Tax receipts, as well as lower debt interest payments, buoyed the government’s finances.

As a result, total borrowing across the first ten months of the current financial year now stands at £112bn, almost £15bn less than the same period last year. This figure is also significantly below the Office for Budget Responsibility’s (OBR’s) November forecast of £120bn for the same period.

On 3 March, the Chancellor will provide an update on the country’s finances in her Spring Forecast. A new OBR forecast for economic growth and the public finances will be published alongside her forecast, although the OBR will not provide a formal assessment of whether the Chancellor is on track to meet her fiscal rules.

Retail sales rise strongly in January

While the latest official retail sales statistics revealed stronger-than-expected growth in sales volumes during the first month of this year, survey data continues to highlight a relatively tough environment for the retail sector.

Recently published ONS data showed that total retail sales volumes grew by 1.8% in January, a significant improvement on December’s 0.4% rise and much healthier than the 0.2% median forecast from a Reuters poll of economists. The release also revealed that sales volumes rose by 4.5% over the year to January; this represents the fastest annual growth rate in nearly four years.

ONS noted that January’s sales jump was driven by strong auction demand for artwork and antiques as well as a further rise in sales at online jewellers, both linked to the recent spike in gold and silver prices. An increase in demand for sports supplements driven by healthy new year’s resolutions also provided a boost to January’s figures.

The latest CBI Distributive Trades Survey, however, continues to highlight ‘gloomy sentiment’ across the retail and broader distribution sector. Indeed, data from last month’s survey suggests sales volumes fell back sharply in February, with retailers saying the unusually persistent wet weather discouraged shoppers from visiting stores.

All details are correct at the time of writing (02 February 2026)

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for information only. We cannot assume legal liability for any errors or omissions it might contain. No part of this document may be reproduced in any manner without prior permission.

Rents across Britain have hit record highs, now consuming 44% of the average wage

People overestimate the cost of life insurance, leading them to delay taking out protection

Many manual workers are missing out on protection despite the risk of workplace accidents

Rents eat up 44% of average wage

Recent data1 shows that rents across Britain have hit record highs. The average advertised rent in London has risen to £2,736 per month, up 1.6% from 2024, while rents outside the capital now average £1,385 a month, a 3.1% increase, which is the smallest annual rise since 2020. Despite slower growth, tenants face continued pressure, with rents now consuming 44% of the average wage.

Life insurance misunderstood – costs overestimated

A recent survey2 reveals that people overestimate the cost of life insurance by 184%, guessing an average monthly premium of £79.50 – while the actual average policy is just £27.95. This misperception leads many to delay protection until major life events like marriage or homeownership, even if those milestones occur later or not at all.

Over a quarter of respondents said cost is their main barrier, illustrating a major disconnect between perceived and real affordability.

Manual workers missing out on income protection

A survey3 of 5,000 UK adults has uncovered a stark protection gap – while nearly a quarter of manual workers believe they’ll suffer a workplace accident within three years, only 4% hold income protection policies and just 1% have accident-only cover. Many haven’t even considered how they’d cope financially after injury. Clear advice is essential to help workers understand and access suitable protection.

As a mortgage is secured against your home or property, it could be repossessed if you do not keep up mortgage repayments. Financial protection policies typically have no cash in value at any time and cover will cease at the end of the term. If premiums stop, then cover will lapse.

Latest ONS data shows the Consumer Prices Index fell to its lowest level since last March

ONS retail data shows sales volumes rose by 1.8% in January – the strongest monthly growth since May 2024

President Trump said he intends to impose global tariffs of 15%, escalating his response to a Supreme Court ruling

“Inflation fell markedly in January”

The latest inflation data from the Office for National Statistics (ONS) for January shows the Consumer Prices Index (CPI) fell to its lowest level since last March. In the 12 months to January, CPI increased by 3.0%, down from 3.4% in the 12 months to December, in line with expectations from a Reuters poll of economists.

Although the inflation rate is tempering, prices are rising at a slower pace. Chief Economist at ONS Grant Fitzner commented on the latest dataset, “Inflation fell markedly in January… driven partly by a decrease in petrol prices.” The reduction can also be attributed toa lowering in airfares, as prices fell back after festive increases in December. Food and non-alcoholic drink also helped the rate tick lower as prices increased at a slower pace, although lower costs for meat, cereals and bread were partially offset by the cost of takeaways and hotel stays.

The fall in CPI has heightened expectations of an interest rate cut, especially when combined with the news of a slowdown in wage growth. Suren Thiru, Economics Director of the ICAEW feels an interest rate in the spring is now almost a given, saying prices took “a decisive turn for the better in January… these figures make a spring interest rate cut look almost assured, though a lingering question among policymakers will be whether to pull the trigger in March or April as some may want slightly more evidence of easing inflation before reducing rates.”

January retail sales jump on fitness and gold demand

Retail data from ONS shows sales volumes rose by 1.8% in January, beating expectations and marking the strongest monthly growth since May 2024. Demand for sports supplements, likely linked to New Year’s resolutions, helped drive the increase. Strong online jewellery sales, supported by higher gold prices, also contributed.

Analysts caution the uplift may prove short-lived. Sales were close to flat over the three months to January, and signs of a softer labour market may weigh on consumer confidence.

Trump and tariffs

Last week, President Trump said he intends to impose global tariffs of 15%, escalating his response to a Supreme Court ruling that struck down his previous import taxes. The court ruled 6–3 that he had overstepped his authority under a 1977 emergency powers law. Trump had initially proposed a 10% levy on all imports, due to take effect on 24 February, but later said he would raise this to 15%. The temporary measure can last around five months without congressional approval, creating uncertainty for the US’s global trading partners. The 10% levy came into effect on Tuesday.

Downing Street representatives have said no retaliatory action is ‘off the table’ if the US fails to honour its tariff agreement with the UK, though it stressed that ‘no one wants a trade war.’ The Prime Minister’s spokesperson said most elements of the UK-US deal, including arrangements covering steel, cars and pharmaceuticals, are not expected to change. However, they described the situation as ‘evolving,’ with discussions between the two governments continuing. The EU has paused its own tariff agreement with the US.

World Cup leads to late night pub opening

Pubs in England and Wales will be permitted to open later for any home nation knockout matches during this summer’s men’s World Cup, set to be held in the US, Canada and Mexico. Kick off times will be at least five hours behind the UK. The government had initially proposed extended hours for the semi-finals and final only, but this has now been widened to cover all knockout fixtures involving England, Scotland and Wales or Northern Ireland (qualification permitting).

Under the temporary measures, pubs in England and Wales can open until 01:00 for knockout matches, and until 02:00 for 22:00 kick-offs, with later games able to apply for temporary licences. Licensing remains devolved in Scotland and Northern Ireland, where local authorities will determine their own arrangements.

According to the British Beer and Pub Association, the news is “a win for pubs, jobs and community spirit,” with major football fixtures delivering substantial uplifts in footfall and drink sales.

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (25 February 2026)

February is the best time to put your home on the market according to Rightmove research

The government’s Warm Homes Plan was launched in January with a £15bn investment

Leading housebuilders have met with ministers to discuss planning reforms and the housing market

The best month to sell your home

February is the best time to put your home on the market, according to research from Rightmove.

The study analysed property listings between 2014 and 2024 (excluding 2020 due to the pandemic). It found that 68.9% of homes put up for sale in February go on to secure a buyer, the highest success rate of any month. January and March followed very closely, with 68.8% of homes listed in these months successfully attracting a buyer. This suggests that the first quarter of the year is an optimum time for sellers.

While February listings see the highest proportion of successful sales, January listings sell the fastest, taking an average of 47 days to find a buyer. Colleen Babcock at Rightmove commented, “Sellers who are yet to act but are considering a 2026 move might consider coming to market soon to take advantage of the increase in home-buyer activity.”

Warm Homes Plan launched

In January, the government launched the Warm Homes Plan, a £15bn investment aimed at upgrading British homes and reducing energy bills.

Key measures in the Warm Homes Plan include a commitment to triple the number of homes with solar energy by 2030 and deliver over 450,000 heat pump installations each year. Also, £2.7bn will be invested into the expanded Boiler Upgrade Scheme, meaning eligible households can apply for a grant to replace their fossil fuel heating system with a heat pump or biomass boiler. Overall, the initiative is expected to create 180,000 new jobs in energy efficiency and clean heating.

Ed Miliband, Secretary of State for Energy Security and Net Zero, said, “this is a landmark plan to make the British people better off, secure our energy independence and tackle the climate crisis.” But some experts are concerned that the cost of implementing the plan will be more than the allocated £15bn.

Ministers discuss housing progress

In January, leading housebuilders met with ministers to discuss planning reforms and the current state of the housing market.

Housing Secretary Steve Reed chaired the roundtable, which was attended by major developers including Vistry, Taylor Wimpey and Barratt Redrow. Discussions focussed on the government’s target to deliver 1.5 million homes, which has been supported by the New Homes Accelerator announced in August 2025. Reed said, “Thanks to our changes to planning laws we’re now seeing the green shoots of recovery – with an 18% increase in work starting on new homes compared to the previous year.”

Industry figures have weighed in on the discussion. Steve Turner at the Home Builders Federation welcomed the progress thus far but called for further action: “With no government-backed scheme in place for the first time in decades, many first-time buyers are locked out of the market, suppressing demand and limiting the ability to increase supply.”

Housing market outlook

Colleen Babcock, Property Expert at Rightmove

“It’s a tight contest, but on average February is the best month to get your home sold, followed by further strong months during the upcoming and very important Spring home-moving season. Sellers who are yet to act but are considering a 2026 move might consider coming to market soon to take advantage of the increase in home-buyer activity.”

High demand for office space – research shows office space is currently the most in-demand commercial property asset class

London offices update – office take-up in the capital marks London’s strongest performance since 2019

The (in)efficiency of commercial buildings – analysis indicates 81% of UK city commercial buildings have a low EPC rating

High demand for office spaces

Recent data shows that office space is attracting the highest level of investor interest in England.

Research from BPS London shows that office space is currently the most in-demand commercial property asset class, with 30.5% of office opportunities either under offer or sold subject to contract. This indicates that businesses are shifting back to office-based working after the pandemic. Retail spaces are a close second with 30.2% of opportunities under offer, followed by industrial and warehouse opportunities at 27.5%. Meanwhile, investor demand is much weaker in the leisure and hospitality sectors, with only 16.1% of opportunities attracting an investor.

Investors are showing particularly strong interest in office spaces in the West Midlands (39.0%) and the South East (36.6%). London offices are attracting lower levels of interest (21.6%) – this is likely due to oversupply, with offices representing 71.0% of all available commercial rental stock in the capital.

London offices update

Research from Knight Frank offers an insight into the current state of the London office market.

Office take-up in the capital reached 12.1 million sq. ft across 1,400 deals in 2025, marking London’s strongest performance since 2019. This was partly driven by a notable rise in demand for larger spaces, with around 70% of major corporate lettings in Central London expanding their office footprint last year.

However, supply of prime space is limited; vacancy rates for new, high-spec offices in the City Core are now at 0.3%. Competition is likely to intensify in the coming years, as up to 50 million sq. ft of London office leases are due to expire between now and 2030. Philip Hobley at Knight Frank commented, “London’s business sector’s growth urgently requires new supply to be unlocked in all of its key submarkets in order to meet structural demand over the next five years.”

The (in)efficiency of commercial buildings

Analysis by the British Property Federation (BPF) shows that 81% of commercial buildings in major UK cities have an EPC rating below B.

The research analysed commercial buildings across all asset classes in London, Birmingham, Bristol, Leeds, Liverpool, Manchester and Newcastle. It found that only 3% of buildings have an EPC rating of A, while 16% are rated B. Manchester has the most energy-efficient buildings, with 22% of commercial properties rated A or B. London follows closely at 21%.

In 2021, the government launched a consultation into minimum energy efficiency standards for non-domestic buildings. It proposed a target of EPC C by 2027 and EPC B by 2030, however these measures are yet to be officially implemented. Rob Wall, Assistant Director at BPF, urged the government to take action, saying “Clarity on future standards is critical to increasing demand, attracting investment and building green skills and supply chains.”

Scottish market temperature check

The latest commercial property survey from the Royal Institution of Chartered Surveyors (RICS) suggests that Scottish respondents are cautiously optimistic about the year ahead.

In Q4 2025, a net balance of 12% of respondents reported an increase in occupier demand for Scottish commercial property. Performance varied across subsectors; a net balance of 39% reported a rise in demand for the industrial sector, while -12% noted a drop in demand for retail space.

The outlook for capital values is generally positive, with a net balance of 9% expecting to see a rise at an all-sector level over the next three months. This increases to 21% when considering expectations for capital values over the next 12 months. In terms of rent, a net balance of 18% of Scottish respondents anticipate a rise in Q1 2026.

Tarrant Parsons at RICS commented on the findings, “The Q4 results suggest the UK commercial property market is beginning to find its footing after a prolonged period of adjustment.”

As life expectancy increases, workers are abandoning the idea of spending a whole career with one company

More workers are embracing non-linear career journeys by retraining, switching industries and taking extended breaks

As working lives become more fluid and career paths less predictable, seeking financial advice is essential

More than four in 10 Brits expect to pursue multiple careers if life expectancies continue to rise, research1 shows. As the traditional work trajectory dies out, what will the financial impacts be and how should you prepare?

Multiple careers

Amid longer lives and more opportunities to retrain, workers are abandoning the idea of spending a whole career with one company – or even within one industry. A quarter of respondents expect to switch industries, according to the research, while a fifth plan to try a new profession. More than one in 10 will return to education to support a career shift, the survey revealed. Remarkably, young employees aged 18 to 25 have already worked for an average of six employers, the research found, the same number as those aged 65 to 74.

Reinforcing the takeover of flexibility, some 26% of respondents have taken some form of extended leave, while 65% think we must dispense with the idea that learning, working and retiring is a linear path.

Sound financial guidance throughout the journey

As working lives become more fluid and career paths less predictable, seeking financial advice throughout your journey can make all the difference.

We can help you adapt your financial strategy to each new phase – whether you’re retraining, taking time out or pursuing a passion project – ensuring you stay on track to meet your goals. By planning proactively and making informed decisions about savings, pensions and investments, you can build the freedom to live well at every stage, whatever direction your working life takes. Flexibility may define the future of work, but sound financial guidance remains the key to making it sustainable.

1Canada Life, 2025

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. The Financial Conduct Authority does not regulate Will writing, tax and trust advice and certain forms of estate planning.