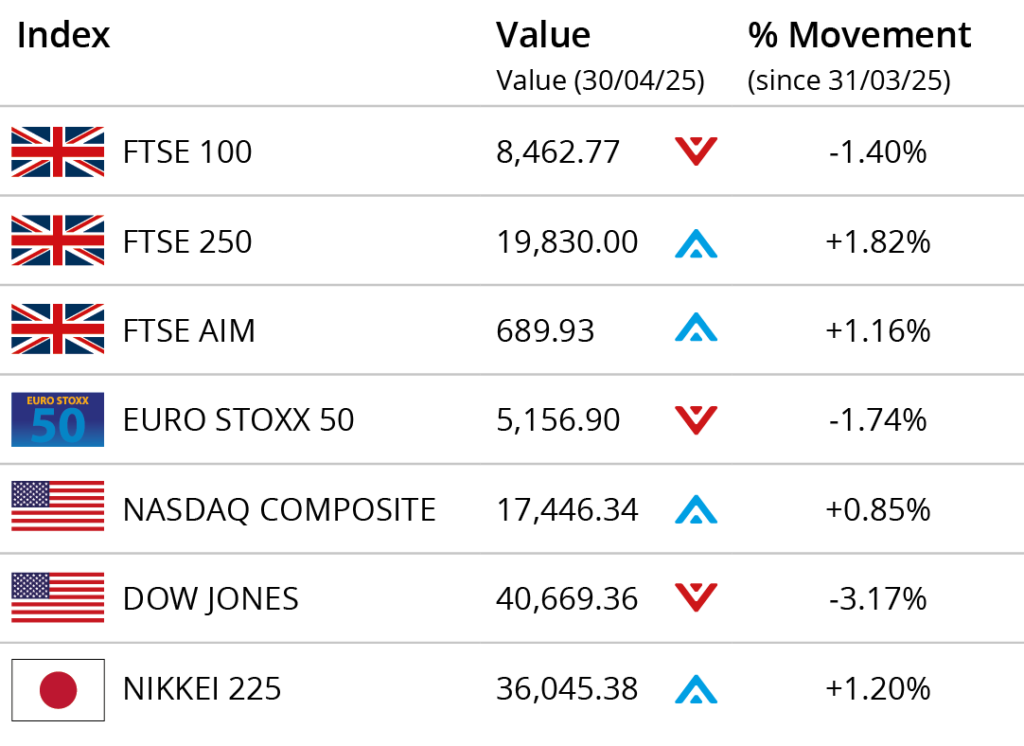

| UK house prices fell by 0.6% in April following a rush in March to beat Stamp Duty changes. Despite the drop, prices remain 3.4% higher than a year ago | US GDP shrank by 0.3% in Q1 2025—its first contraction in three years—due to reduced government spending and a surge in imports ahead of tariffs | Ukraine and the US have signed a new deal to share energy and mineral profits and establish a reconstruction investment fund, aiming to boost Ukraine’s recovery |

“Activity is likely to pick up steadily as summer progresses”

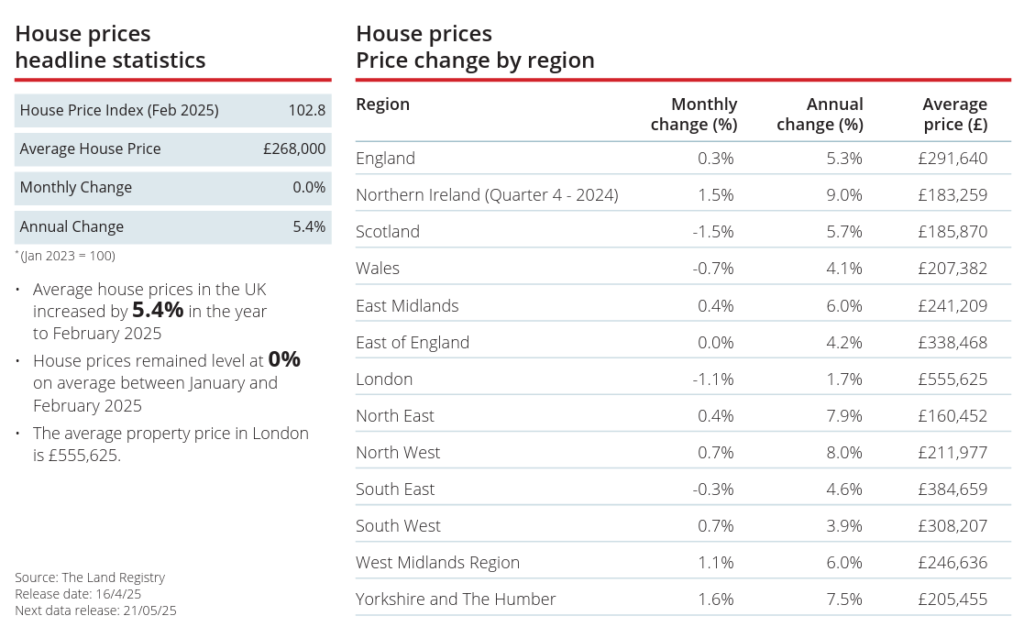

UK house prices fell by 0.6% in April, according to new data from Nationwide, marking the first monthly decline since August 2024. This dip follows a surge in transactions during March, as buyers rushed to complete purchases ahead of Stamp Duty changes introduced on 1 April. While the slowdown was anticipated, annual house price growth remains positive, with homes still 3.4% more expensive than a year ago and the average property price now standing at £270,752.

Nationwide’s index fell from 542.4 in March to 539.3 in April, reinforcing the short-term impact of fiscal policy on buyer behaviour. Looking ahead, market activity is expected to gradually improve.

Nationwide’s Chief Economist, Robert Gardner, explained that the market softness is typical following changes to Stamp Duty, with many buyers bringing forward purchases to avoid higher charges. Looking ahead to the summer months he said, “Activity is likely to pick up steadily as summer progresses, despite wider economic uncertainties in the global economy, since underlying conditions for potential home buyers in the UK remain supportive.”

The latest Money and Credit statistics from the Bank of England (BoE) released last week show net residential mortgage borrowing increased significantly by £9.7bn to £13.0bn in March. Gross lending also saw a sharp uptick to £39.9bn in the month, from £24.9bn in February, and was the highest in almost four years (since June 2021).

On 8 May the main focus will be on the BoE announcement, where the Monetary Policy Committee is expected to vote to lower interest rates by a quarter point. Economists polled by Reuters expect quarter-point rate cuts every three months throughout the year – taking interest rates to 3.75% by the end of 2025.

US economy dips in Q1

The US economy shrank at an annual rate of 0.3% in Q1, marking the first quarterly contraction in three years. The contraction followed growth of 2.4% in the previous quarter (Q4 2024) and was largely attributed to falling government spending and a sharp rise in imports, as businesses rushed to bring goods into the country ahead of tariffs. While imports count negatively toward GDP, economists noted that such swings are not necessarily indicative of a broader economic downturn and may be reversed in subsequent quarters.

President Trump responded to the data by deflecting blame, saying, “This is Biden” and reiterating his belief that tariffs would ultimately lead to stronger domestic investment. The White House called the GDP figure a ‘backward-looking indicator,’ insisting the fundamentals remain strong. “The underlying numbers tell the real story of the strong momentum President Trump is delivering,” said Press Secretary Karoline Leavitt.

Ukraine / US deal struck

Last week, after months of negotiations, Ukraine signed a deal with the US to share future profits from its energy and mineral reserves, aiming to support the region’s economic recovery and incentivise continued US investment in defence and reconstruction. The agreement also established a new US-Ukraine Reconstruction Investment Fund, recognising America’s aid since Russia’s invasion. US Treasury Secretary Scott Bessent said the deal reflects a joint commitment to peace, growth and rebuilding.

Support pledged for UK businesses

Chancellor Rachel Reeves has pledged stronger support for UK businesses by addressing unfair trade practices, such as the import of cheap goods which undercut domestic producers. Measures include empowering the Trade Remedies Authority (TRA) and reviewing customs rules on low value imports. Retailers argue this loophole allows foreign competitors to unfairly underprice UK businesses.

William Bain of the British Chambers of Commerce (BCC) welcomed the move, saying, “There are still many twists and turns to go in the trade war between the US and China. It remains to be seen whether cheap Chinese goods will flood the UK as a result, but the risk is present. It is sensible for the TRA to have all the necessary tools and resources to take action to prevent the UK being swamped with unfairly cheap products.”

He continued, “If domestic production suffers from a surge in imports or dumping of goods it is right that business has clearer access to make their case to the TRA. It must have the resources it needs to enforce a level playing field.”

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (7 May 2025)