82% of advised investors believe they get good value from financial advice, up 10% from last year

96% of advised clients value their adviser’s accessibility, especially during market volatility

Long-term market confidence is higher among advised investors, showing the benefits of expert financial guidance

People with a financial adviser are more optimistic about their financial future. That’s one of the key findings of a recent Investor Confidence Barometer1. Four in five people (82%) said they get ‘value for money’ from their adviser, a 10% increase on 2023’s survey. Investors said they also feel more confident knowing their financial adviser is available in difficult times, with 96% of advised clients valuing accessibility as much as portfolio performance.

Advisers are more optimistic about the long-term performance of equities than investors, with this confidence rubbing off on their clients. Over five years, 89% of advisers expect markets to rise, compared to 63% of advised investors and 57% of those without advice. Over ten years, 91% of advisers are predicting market growth, versus 68% of advised and 57% of non-advised investors. Greater optimism among advised investors suggests financial advice and long-term planning builds confidence in their future wealth prospects.

Ross Easton, Head of Platform Proposition at Scottish Widows, said, “This survey emphasises the difference that advisers make for their clients, especially when it comes to guiding them through times of market volatility. Our Barometer has consistently found that advised clients are more confident than non-advised investors, setting them up to benefit from market corrections and recoveries when others are more cautious.”

1Scottish Widows, 2025

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. The Financial Conduct Authority (FCA) does not regulate Will writing, tax and trust advice and certain forms of estate planning.

Older borrowers are increasingly taking out ultra-long mortgages, with a 156% rise in the last five years

Half of UK homes saw price increases in 2024, there’s a clear north-south divide in property values

Rent costs for tenants under 45 hit a record £56.2bn due to rising mortgage rates

Retiring with a mortgage

With a rise in ultra-long mortgage terms and deals taken out later in life, the number of people who will be paying a mortgage into their seventies has grown rapidly. Data1 reveals a 156% increase in older borrowers taking out longer loan terms in the last five years.

Regional divide in house prices

Half2 of the UK’s 30 million homes increased in value by 1% or more in 2024, while a third recorded a price decline of 1% or more. The split followed a clear north-south divide, with fewer homes recording price gains in Southern England. Coastal towns in Kent and East Sussex were least likely to see values rise.

Record rent rises

Rents paid by tenants aged under 45 rose by £3.5bn last year, a new survey3 has revealed, pushing their combined rental costs to a record high of £56.2bn. “Higher mortgage rates have clipped the wings of many young aspiring homeowners,” commented Aneisha Beveridge of Hamptons.

50% of salaried employees and 33% of non-salaried workers lack life insurance

Life insurance covers expenses like mortgages, bills and education costs should the worse happen

Policies can start as low as a few pounds a month, offering affordable protection and peace of mind

Taking out life insurance is a crucial step in protecting what matters most — your loved ones and their financial security.

The life insurance gap

Recent research1 highlights a concerning ‘life insurance equality gap’ among UK workers. The survey found that only 50% of salaried employees have life insurance, while an even lower percentage — just 33% — of non-salaried workers, including freelancers, self-employed and those on zero-hour contracts, have cover in place.

The importance of life insurance

Life insurance provides essential financial support for your family in the event of your passing. The payout can help cover major expenses, such as your mortgage, rent, household bills and education costs. Suitable life insurance written in trust can also serve as an effective estate planning tool, as payouts are typically free from Inheritance Tax, allowing beneficiaries to receive the full amount.

Isn’t life insurance expensive?

Despite its benefits, many people hesitate to get life insurance, believing it’s too costly. The survey found that 25% of non-salaried workers and 19% of salaried workers cited high costs as a barrier to obtaining cover. However, this is often a misconception as life insurance policies can start at just a few pounds a month.

Peace of mind for you and your family

Beyond financial security, life insurance is a simple yet effective way to provide lasting protection and peace of mind, helping your loved ones receive the support they deserve. We are here to help you find the right cover for you and your family.

Global economic growth is slowing, with major economies facing tight financial conditions and rising trade barriers

Basic retirement costs have decreased due to lower energy bills, though comfortable living standards are higher than last year

New pension reforms aim to improve returns, merge small pots and support stronger retirement outcomes for savers

‘The global outlook is becoming increasingly challenging’

Global GDP growth is projected to slow to 2.9% this year and next year, according to the latest Economic Outlook released last week by the Organisation for Economic Co-operation and Development (OECD), down from 3.3% in 2024.

The report highlights that barriers to growth, including tighter financial conditions, weakened business confidence and trade barriers, are causing the slowdown, with the United States, Canada, Mexico and China experiencing the biggest downward pressures. The UK is forecast to suffer too, as US tariff barriers and the country’s ‘very thin’ buffer in public finances create a unique set of challenges for Chancellor Rachel Reeves.

‘The global outlook is becoming increasingly challenging,’ the OECD states in its report, as ‘substantial increases in trade barriers, tighter financial conditions, weakened business and consumer confidence, and elevated policy uncertainty all pose significant risks to growth. If these trends continue, they could substantially dampen economic prospects.’

Basic retirement costs lower as energy prices fall

Falling domestic gas and electricity bills have reduced the amount needed for a ‘minimum retirement lifestyle,’ according to a new report released last week by the Pensions and Lifetime Savings Association (PLSA).

The minimum retirement fund required per year for a two-person household to meet a basic standard of living in retirement is now £21,600, the PLSA says, down from £22,400 a year previously, while the equivalent for a one-person household has fallen to £13,400 per year.

Despite the lower threshold for basic living, costs have risen for anyone wanting a more comfortable retirement: a single person wanting to have a ‘moderate’ lifestyle now needs £31,700 a year, the report estimates. Likewise, a couple would need £43,900 to fit into this category, which includes basics like groceries and leisure activities, as well as a week holidaying in Europe, and a long weekend break in the UK.

Pensions boost for millions

Last Thursday, the government published its new Pension Schemes Bill, which it says will ‘tackle schemes delivering poor returns for savers, combine smaller pension pots, and create bigger and better pension funds.’

The Pension Schemes Bill is part of the government’s broader Plan for Change and will assist millions of people planning their retirement to manage and get more from their pension pots. Additionally, the scheme is intended to drive more investment into the UK economy.

Specifically, its key measures include:

Requiring defined contribution (DC) pension schemes to prove they offer good value for money

Creating multi-employer DC scheme ‘megafunds’ managing at least £25bn in assets by 2030

Offering default routes to an income in retirement in all schemes

Bringing together small pension pots worth £1,000 or less into one pension scheme that is certified as delivering good value to savers

Increasing flexibility for defined benefit (DB) pension schemes to safely release surplus worth collectively £160bn.

Commenting on the reforms, Minister for Pensions Torsten Bell said, “Workers deserve to get better bang for each buck saved and these sweeping reforms will make sure they do. Pension saving is a long game, but getting this right is urgent so that millions can look forward to a higher income in retirement.”

Government budget shake-up in latest Spending Review

A major Spending Review, due to be released by Chancellor Rachel Reeves on Wednesday 11 June, will increase the National Health Service budget and clarify government priorities on defence spending and public transport schemes.

The Spending Review sets the budgets for all government departments over the next few years. As the government’s two self-imposed fiscal rules (that day-to-day government spending be paid for with tax revenue and that government debt falls as a share of national income by the end of the current parliament) weigh heavily on Ms Reeves, the margins for action are slim.

Ahead of the release, the government has already announced that spending on defence will rise to 2.5% of GDP by 2027. Similarly, a commitment to give public sector workers in England a pay hike between 3 and 5% in 2025-26 will push spending up. Winter fuel payments will also be made to three quarters of pensioners in England and Wales this year and free school meals will be expanded to 500,000 children whose parents are receiving Universal Credit.

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (11 June 2025)

Research shows a third of European HNWIs are yet to make a financial plan for retirement

80% of survey respondents plan to pass wealth to their children, but only 34% have a plan in place

Over half of respondents are focused on growing their wealth through investing in equities and/or real estate

Many high-net-worth individuals (HNWIs) have yet to establish retirement or succession plans, even though they remain confident about the growth of their personal wealth, according to a study1.

Research shows a third of European HNWIs are yet to make a financial plan for retirement. While those who have started a retirement plan, half said that they do not have a fully formed plan in place. And while 80% of survey respondents plan to pass wealth down to their children, only 34% have a full succession plan in place.

With over three quarters (78%) of HNWIs expecting their personal wealth to rise over the next five years, it’s surprising that many HNWIs fail to have plans in place for their retirement and succession. The study found that multigenerational HNWIs who had inherited wealth were more likely to have at least started planning for retirement than first-generation HNWIs.

Taking a closer look at HNWIs’ investment strategies, over half of respondents are focused on growing their wealth through investing in equities and/or real estate to support this long-term objective.

1BlackRock, 2024

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

6.3 million homes face flooding threats, but the dangers are expected to rise significantly due to climate change

4.6 million properties are at risk of surface water flooding, a 43% increase since 2018

Taking proactive steps, including insurance, is key to protecting against flood damage

A recent report from the Environment Agency has revealed that one in four properties in England are in areas vulnerable to flooding, with millions of homes at risk of being overwhelmed by water from rivers, the sea, or surface water accumulation.

The survey examined 25 million homes across England to evaluate their flood risk. The findings indicate that 4.6 million properties are now susceptible to flooding from surface water – a dramatic 43% increase from the agency’s previous assessment in 2018. Surface water flooding occurs when rainwater fails to drain properly, often due to intense rainfall, waterlogged ground, or overwhelmed drainage systems, leading to flash floods that can develop within minutes.

Climate change and future risks

Currently, 6.3 million homes face flooding threats, but the dangers are expected to rise significantly due to climate change. Projections suggest that, by 2050, the number of at-risk homes could increase to around 8 million. Rising global temperatures contribute to more extreme weather patterns, with heavier rainfall and rising sea levels exacerbating the issue.

Preparedness and mitigation

As flood risks continue to climb, experts are urging homeowners, businesses and policymakers to take proactive steps to mitigate potential damage. Investing in improved drainage infrastructure, implementing sustainable urban planning and increasing public awareness are crucial measures in addressing the growing threat.

Protecting your home

While flooding is a significant risk for millions of homeowners, it’s just one of many potential threats to your property. A comprehensive home insurance policy can provide vital protection against fire, theft, storm damage and other unexpected events. Ensuring you have the right cover in place can give you peace of mind, no matter what challenges arise. Review your policy with us to make sure your home is fully protected.

As a mortgage is secured against your home or property, it could be repossessed if you do not keep up mortgage repayments. Think carefully before securing other debts against your home. Equity released from your home will be secured against it.

UK economic growth has been revised upwards by the International Monetary Fund – 1.2% in 2025 and 1.4% in 2026

The government plans to double £25bn+ pension megafunds to improve retirements and boost UK investment

Retail confidence plunges to a five-year low, with sales falling and businesses bracing for tougher conditions

‘An economic recovery is underway’

The UK economy is expected to grow faster than previously thought next year, according to the International Monetary Fund (IMF), but the government faces growing pressure to balance its books.

In its latest review, IMF forecasts UK growth of 1.2% in 2025, up from April’s 1.1% projection, and 1.4% in 2026, saying ‘an economic recovery is underway.’ The upward revision follows a stronger-than-expected start to the year, helped by rising consumer spending and business investment. Luc Eyraud, IMF’s UK Mission Chief, described growth in the first quarter as “very strong,” though he noted the figures pre-date the impact of new import tariffs and higher employer taxes introduced in April.

The review welcomed recent planning and infrastructure investment reforms, saying they could lift long-term growth if fully delivered. However, IMF cautioned that global instability and tight fiscal conditions would test the Chancellor’s commitment to her tax and spending rules. It recommended cutting the number of annual fiscal assessments by the Office for Budget Responsibility from two to one, to reduce pressure on short-term decision-making.

Despite growing fiscal challenges, the government insists its two core rules – covering everyday spending from tax revenues and reducing debt as a share of GDP by 2030 – remain non-negotiable. Although global trade tensions are expected to weigh on growth, IMF acknowledged the government’s efforts to provide stability through trade deals with the EU, US and India.

On Monday, the government accepted all 62 recommendations from the long-awaited Strategic Defence Review (SDR), including building 12 new nuclear-powered submarines, six new munitions factories and embracing AI.

Government to double pension megafunds by 2030

The government has confirmed plans to double the number of UK pension ‘megafunds’ by 2030, a move which it says will help millions of workers retire with larger pension pots. Megafunds are defined as multi-employer defined contribution schemes or Local Government Pension Schemes managing at least £25bn in assets.

New rules will require all such schemes to operate at megafund scale by the end of the decade. The government says this shift will unlock greater investment opportunities, such as infrastructure and private equity, leading to stronger long-term returns for savers.

Chancellor Rachel Reeves said, “We’re making pensions work for Britain. These reforms mean better returns for workers and billions more invested in clean energy and high-growth businesses — the Plan for Change in action.”

Reforms will be delivered through the upcoming Pension Schemes Bill. The legislation will also introduce clearer value-for-money measures and allow schemes to move savers into higher-performing funds, with protections in place. Funds that already exceed £10bn in assets will be allowed to remain if they present a credible plan to hit the £25bn threshold by 2035.

The shift builds on a recent pledge by pension funds to invest more in UK assets, supported by new local investment targets for LGPS authorities. In total, £50bn has already been committed. According to the government, reforms could also reduce system inefficiencies, saving £1bn annually and potentially adding £6,000 to the average saver’s pension pot.

Retail confidence hits five-year low as sales slide

Retailers are expecting tougher times ahead, according to the Confederation of British Industry (CBI), after the UK retail sector fell sharply in May. Its latest quarterly survey shows confidence among retailers dropping to its lowest level since May 2020, with a net balance of -29% expecting business conditions to deteriorate over the next three months.

Sales volumes also declined more steeply, with the CBI’s monthly gauge falling to -27 in May, down from -8 in April. Looking ahead, expectations for June are even weaker, with a reading of -37, the lowest since February 2024.

The findings point to a growing divide between headline economic data and the day-to-day experience of many high street businesses, as consumer demand remains patchy and cost pressures persist.

“This was a fairly downbeat survey and highlights some of the challenges facing the retail and wider distribution sector,” said Ben Jones, Lead Economist at the CBI. “In contrast to other recent retail data, this survey suggests parts of the sector are still struggling with fragile consumer demand, though online sales seem to be holding up better.”

The pessimism comes despite recent official figures showing a surprisingly strong rise in sales in April.

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (4 June 2025)

GDP unexpectedly rose by 0.7% in Q1 2025, driven by services, production and investment growth

The Bank of England cut interest rates despite inflation jumping to a 15-month high at 3.5%

The UK labour market shows weakness as payrolls drop and unemployment edges up to 4.5%

UK growth beats expectations

First quarter gross domestic product (GDP) data published last month by the Office for National Statistics (ONS) showed the UK economy grew more strongly than had been predicted during the first three months of 2025.

According to the latest GDP statistics, economic output rose by 0.7% between January and March, up sharply from a rate of 0.1% in the final three months of 2024. This figure was also higher than economists had been expecting, with the consensus forecast from a Reuters poll pointing to a quarterly growth rate of 0.6%.

ONS said the economy’s strong first quarter performance was largely driven by the services sector, which includes businesses in areas such as retail, hospitality and finance. The production sector, however, also saw significant growth as firms brought activity forward in order to beat the imposition of US tariffs, while business investment grew strongly too, recording its largest quarterly growth rate for two years.

Updated growth forecasts released towards the end of last month by the International Monetary Fund (IMF) were nudged higher in order to reflect the strong first quarter data. The international soothsayer now predicts the UK economy will expand by 1.2% across the whole of 2025, with growth expected to hit 1.4% next year, in spite of headwinds from US tariffs which are expected to reduce annual output by 0.3%.

Despite the upgrade, the IMF forecast still assumes the strong performance seen early this year will prove short-lived. Survey evidence also points to a sharp second quarter slowdown, with data from the S&P Global UK Purchasing Managers’ Index hinting at a possible second quarter contraction. While last month’s flash Composite Output figure was up on the previous month’s level ‒ suggesting an easing of the downturn in May ‒ it did still remain below the 50.0 threshold that denotes contraction in business activity.

Interest rates down; inflation up

Last month saw the Bank of England (BoE) sanction a further cut in interest rates while data released a couple of weeks after that decision showed the headline rate of inflation now standing at a 15-month high.

Following its latest meeting, which concluded on 7 May, the BoE’s nine-member Monetary Policy Committee (MPC) voted by a 5-4 majority to reduce rates by 0.25 percentage points, taking Bank Rate down to 4.25%. Unexpectedly though, there was a three-way split among policymakers: while two of the four dissenting voices actually voted for a larger half-point reduction, the other two dissenters preferred to leave rates unchanged.

Analysts had not expected any votes to be cast against a rate cut and the fact that two MPC members did, sent a more hawkish message in relation to the speed of any future monetary policy easing. A recent Reuters poll, however, did find that most economists still expect two more cuts this year, with the consensus viewing August as the most likely date for the next reduction.

Commenting after announcing the MPC’s decision, BoE Governor Andrew Bailey also reaffirmed his expectation that rates will continue on a downward trajectory. While Mr Bailey stressed that he was not prepared to “give predictions as to when and how much,” he did state that he was “still of the view that the path, gradually and carefully, is downwards.”

The latest official inflation statistics released two weeks after the MPC meeting, though, showed that the annual headline CPI rate jumped to 3.5% in April from 2.6% in March. This figure was above market expectations and represents the highest reading since January 2024. It also clearly leaves inflation significantly above the BoE’s 2% target, and led some economists to suggest that any future rate cuts may need to be more gradual.

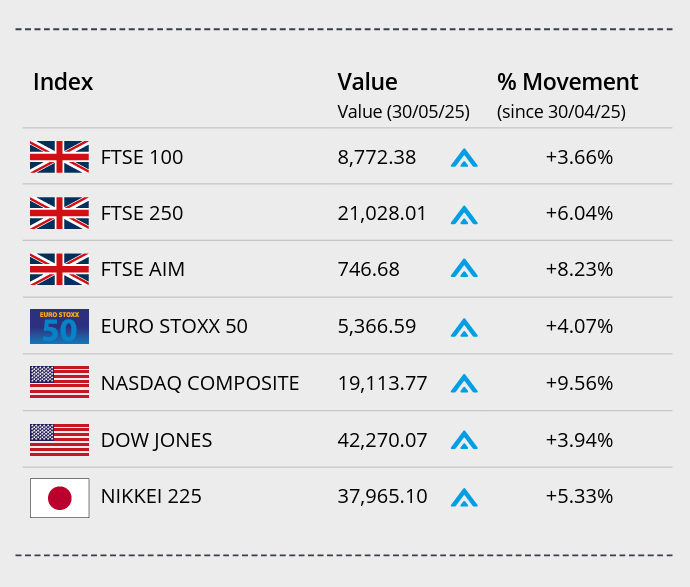

Markets

At the end of May, the FTSE 100 rose while US and Asian stocks fell as investors digested new tariff uncertainty. As the month drew to a close, President Trump accused China of breaking their tariff truce, he was also defending potential roadblocks to his trade policies from the US courts.

In the UK, the FTSE 100 index closed the month on 8,772.38, a gain of 3.66%. The mid-cap focused FTSE 250 closed May up 6.04% on 21,028.01, while the FTSE AIM closed on 746.68, a monthly gain of 8.23%.

The Dow Jones closed May up 3.94% on 42,270.07, while the tech-orientated NASDAQ closed the month up 9.56% on 19,113.77. May marked the best month for the NASDAQ since November 2023.

On the continent, the Euro Stoxx 50 closed May 4.07% higher on 5,366.59. In Japan, the Nikkei 225 ended the month on 37,965.10, a monthly gain of 5.33%.

On the foreign exchanges, the euro closed the month at €1.18 against sterling. The US dollar closed at $1.34 against sterling and at $1.13 against the euro.

Brent Crude closed May trading at around $60 a barrel, a monthly loss of just over 1.00%. The oil price fell at month end pressured by uncertainty over US trade policy developments and expectations of increased supply from OPEC+. Gold closed the month trading around $3,291 a troy ounce, a monthly loss of 0.77%. The price edged lower at month end as traders positioned themselves ahead of the release of US inflation data.

Retail sales growth remains strong

The latest official retail sales statistics showed sales volumes grew strongly in April, while more recent survey evidence points to a pick-up in optimism among the consumer base.

ONS data released last month revealed that retail sales volumes grew by 1.2% in April; this figure was significantly above analysts’ expectations and marked a fourth successive monthly increase in sales volumes. ONS noted that April’s warm weather provided a boost to sales across most sectors with supermarkets, butchers, bakers, alcohol and tobacco stores all enjoying a particularly positive month.

Data from GfK’s most recent consumer confidence survey also offered some cheer to the retail sector, reporting an improvement in consumer morale. Driven by improved optimism in households’ outlook for both their own finances as well as wider economic prospects, May’s headline figure rose to -20 from a figure of -23 the previous month.

Last month’s CBI Distributive Trades Survey, however, did report a sharp decline in confidence among retailers with its gauge of business sentiment dropping to its lowest level since May 2020. CBI Lead Economist Ben Jones described May’s results as “fairly downbeat” adding that some parts of the retail sector were continuing to struggle with “fragile consumer demand.”

More signs of a weakening jobs market

Labour market data released last month revealed further signs of cooling in the UK jobs market, with the number of workers on payrolls and vacancies both declining and the unemployment rate ticking higher.

Provisional tax office statistics published by ONS showed that the number of employees on companies’ payrolls fell by an estimated 33,000 in April following a 47,000 drop in March. The overall level of job vacancies also fell once again, with 42,000 fewer reported in the February to April period; this represents the largest decline in over a year.

The data also revealed an increase in the unemployment rate, which rose to 4.5% in the three months to March; this compares to 4.4% during the previous three-month period. ONS did, however, warn that its unemployment figures still need to be treated with some caution due to increased data volatility stemming from low survey response rates.

A Chartered Institute of Personnel and Development survey released last month also reinforced the picture of a cooling jobs market; the survey’s headline gauge of employment intentions fell to a record low outside of the pandemic, as rising employment costs and uncertainty in the global economy forced many organisations to scale back recruitment.

All details are correct at the time of writing (02 June 2025)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from, taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.

Research highlights key differences in wealth transfer preferences and family financial priorities between men and women

Top financial priorities for 2025 include enjoying life (34%), building emergency savings (30%) and pension saving (11%)

AI now accounts for 42.5% of financial fraud attempts, with cases rising 80% over the past three years

Women put children first in succession planning

Research1 shows that women prioritise their children in succession planning, while men are more likely to focus on their spouse. Among high-net-worth women, 45% prioritise their children, compared to 33% of men. Meanwhile, 37% of men prioritise their spouse, whereas only 17% of women do, highlighting key differences in wealth transfer preferences and family financial priorities.

Personal finance positivity on the up

New research2 reveals that 60% of UK adults feel positive about their finances this year, up from 52% in 2024. Top financial priorities for 2025 include enjoying life (34%), building emergency savings (30%) and pension saving (11%). Despite economic challenges and high inflation, pension-saving attitudes remain steady. Unexpected expenses remain the biggest financial concern (35%). These findings suggest that while financial confidence is growing, many people are focused on balancing short-term enjoyment with long-term security.

AI financial fraud hits 42%

A recent report3 reveals that artificial intelligence (AI) now accounts for 42.5% of financial fraud attempts, with cases rising 80% over the past three years. AI has made fraud easier to carry out, but external factors also contribute to the surge. Meanwhile, banks and financial institutions are leveraging machine learning to detect and prevent fraud, continuously improving their ability to combat evolving threats in an increasingly digital landscape.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. The Financial Conduct Authority (FCA) does not regulate Will writing, tax and trust advice and certain forms of estate planning.

Over 15,000 active customers and £622m in lending recorded in Q4 2024, up from £525m in Q4 2023

A 3.3% increase in UK house prices contributed to larger loan sizes and improved product availability.

A 27% rise in returning customers using further advances shows growing confidence in equity release

Looking at The Equity Release Council’s (ERC) recent data1 for Q4 2024, it highlights that there were over 15,000 active customers in the market during the period, the highest recorded since Q3 2023.

With customers, either agreeing new plans, taking drawdowns from existing plans or agreeing further advances (extensions) to existing plans, total lending in Q4 2024 reached £622m, a significant rise from the £525m recorded in Q4 the previous year.

The report highlights a 3.3% rise in UK house prices, which contributed to larger loan sizes for both drawdowns and lump sum mortgages. It also notes that product availability has improved over the last year. The market also saw a rise in returning customers using further advances, with a 27% increase in Q4, which, according to ERC Chair, David Burrowes, reflects “the confidence that homeowners have in leveraging their property wealth responsibly.”

Confidence returns

Marking a third consecutive quarter of growth, signalling returning consumer confidence, Burrowes commented, “The equity release market has turned a corner and there is cause for optimism. Interest rates have started to settle and if the growth seen in 2024 continues to gain momentum, 2025 will see more customers considering the option to access their housing equity using an increasingly diverse range of innovative products.”

Speaking of customers making use of reserve facilities to manage borrowing efficiently over time, Burrowes said this demonstrates “the versatility of equity release in addressing diverse financial goals, from home improvements to supplementing retirement income.”

1ERC, 2025

As a mortgage is secured against your home or property, it could be repossessed if you do not keep up mortgage repayments. Think carefully before securing other debts against your home. Equity released from your home will be secured against it.