Average asking prices hit record highs, but growth is slowing, as analysts suggest we’re in a buyers market

Moving costs have risen sharply across the UK due to changes in tax and associated fees

First-time buyers see improved affordability supported by flexible mortgage products

As summer begins, the housing and mortgage markets are experiencing a mix of milestones and shifts offering both opportunities and challenges for buyers and movers.

House prices at a new high

The average asking price of a property coming to the market climbed to a record high of just under £380,000 in May1. However, the annual pace of growth appears to be slowing and many analysts suggest we are now in a buyers’ market.

The cost of moving also rises

Across the UK, the average cost of moving home has surged by 13% over the last year alone2. In England, this is largely linked to changes in Stamp Duty Land Tax (SDLT) from 1 April. Taking into account initial costs including a deposit, Stamp Duty, conveyancing, mortgage costs and removals, one estimate3 puts the cost of moving in England at nearly £52,000. This compares to £34,429 in Wales (where Land Transaction Tax applies rather than SDLT), £32,172 in Scotland (where Land and Buildings Transaction Tax applies rather than SDLT) and £31,353 in Northern Ireland. So, whichever nation you live in, upgrading or relocating has become more financially challenging for many households.

First-time buyer affordability at 10-year high

However, despite rising property prices and increased initial costs, there is promising news for first-time buyers as affordability for this group has reached its best level in a decade4, helped by a combination of wage growth, stabilising property values and more accessible mortgage options.

Low and no deposit options on the rise

Lenders are increasingly catering to new buyers with limited savings. The number of low-deposit mortgages is at a 17-year high5, reflecting greater flexibility in the lending market. Furthermore, 100% mortgages, which require no deposit, have made a cautious return.

Looking ahead

While high asking prices and moving costs present clear hurdles, improved affordability and expanded lending options offer hope for first-time buyers. As the summer unfolds, the market seems to be recalibrating, potentially paving the way for a more balanced housing landscape.

Summer is the ideal time to review financial goals and investment strategies

Utilising tax allowances now can protect your wealth from future policy changes

Long-term investing remains key, even amid short-term market volatility

Summer should bring a welcome shift in pace: longer days, warmer evenings, time off and the chance for some well-earned rest and recuperation. Whether you’re planning a trip abroad or staying closer to home, it’s a good time to take stock of life, this extends to your finances too.

Take this year’s Autumn Budget, where there’s a good chance the Chancellor will announce new changes to tax rules and allowances. So now might be the right time to prepare for what’s likely further down the line and maximise current opportunities.

Long-term thinking

It’s been a challenging year for investors, with uncertainty weighing on markets, but short-term fluctuations don’t change the case for long-term investing. And besides, opportunities often present when markets are under pressure.

Revisiting your investment goals

Reviewing your portfolio to check it still reflects your risk tolerance and financial goals is always a wise move. Whether your circumstances have changed, or your priorities have shifted, we can help assess your options and make sensible adjustments, if necessary.

Using your allowances

Now’s a good time to check in on your ISA and pension contributions. Using your annual ISA allowance can help shield your savings and investments from Income Tax and Capital Gains Tax (CGT). Pension contributions also offer valuable tax relief and reviewing them before any potential policy changes may make sense.

If you’re considering selling assets, such as shares or property you don’t live in, make use of your CGT exemption, which was halved last year. With further changes to Inheritance Tax (IHT) ahead, reviewing any current estate planning strategies – including making use of annual gifting allowances – could help reduce future liabilities on your estate.

Stay one step ahead this summer

While we don’t have a crystal ball about potential changes, we can make sure your financial strategies are working hard for you. We’re always keeping a close eye on developments which may impact your finances and can help you adapt your plans accordingly. By proactively addressing these areas together, you can position yourself to better withstand fiscal changes and optimise your financial wellbeing in the process.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. The Financial Conduct Authority (FCA) does not regulate Will writing, tax and trust advice and certain forms of estate planning.

The UK economy grew modestly in Q2, recovering slightly after April’s sharp GDP contraction of 0.3%

The Bank of England held interest rates at 4.25% but signaled likely cuts from August

Retail sales slumped by 2.7% in May, with supermarkets and clothing stores citing weak consumer demand

Survey points to modest second-quarter growth

Data released last month by the Office for National Statistics (ONS) showed that UK economic output slowed sharply in April, while more recent survey evidence suggests activity remained relatively lacklustre across the rest of the second quarter.

According to the latest gross domestic product (GDP) statistics, UK output fell by 0.3% in April, the largest recorded monthly decline since October 2023. This performance was worse than economists had been expecting, with the consensus forecast from a Reuters poll predicting a 0.1% contraction.

ONS said the services sector was the main contributor to this decline, with legal firms and property companies faring particularly badly following a strong March which saw homebuyers rush to complete house purchases ahead of an increase in Stamp Duty rates on 1 April. In addition, car manufacturing weakened significantly, largely due to the introduction of President Trump’s initial tariffs on vehicle exports to the US.

Monthly GDP figures can be relatively volatile though and ONS did note that across the three months to April the economy actually grew by 0.7%. Survey evidence also points to a modest recovery in private sector business output since April’s sharp fall.

The flash headline growth indicator from the closely-watched S&P Global/CIPS UK Purchasing Managers’ Index (PMI), for instance, rose to 50.7 in June, up from 50.3 in May. In both months, the index was therefore just above the 50.0 threshold denoting growth in activity, leaving data spanning the whole of the April-June period consistent with a 0.1% quarterly rate of economic expansion.

Commenting on the preliminary PMI data, S&P Global Market Intelligence’s Chief Business Economist Chris Williamson said the UK economy remained in a “sluggish state” at the end of the second quarter. However, he also noted that business conditions had improved since April’s downturn and suggested this had quelled recession fears.

BoE keeps rates steady but hints at more cuts

While last month did see the Bank of England (BoE) maintain interest rates at their current level of 4.25%, the Bank’s Governor again suggested they remain on a downward trajectory, with economists typically expecting the next cut to be announced in August.

At its latest meeting, which concluded on 18 June, the BoE’s nine-member Monetary Policy Committee (MPC) voted to leave Bank Rate on hold by a 6–3 majority: all three of the dissenting voices, however, preferred to see an immediate quarter-point reduction. While the minutes to the meeting did stress that interest rates ‘were not on a pre-set path,’ they also hinted at more cuts once risks to inflation have ‘dissipated further.’

On the same day that the MPC meeting ended, ONS published the latest official inflation statistics, which revealed that May’s annual headline CPI rate was unchanged at 3.4%. This did, though, leave the CPI rate significantly above the Bank’s 2% target at its highest level in more than a year.

In a speech delivered around a week after the release of the inflation data, BoE Governor Andrew Bailey stated that continued efforts were needed to push inflation lower. However, Mr Bailey also noted growing evidence that April’s rise in employment costs was hitting pay and jobs, and that this should contribute to slowing inflation; and he once again reiterated his view that interest rates remain on “a gradual downward path.”

Most economists now expect the Bank to sanction another rate reduction after the MPC’s next meeting, which is scheduled for 7 August. A Reuters survey conducted last month, for instance, found that almost all of the 59 economists polled were forecasting a quarter-point cut in August, with a large majority predicting a further similar-sized reduction at some point during the final three months of the year.

Markets

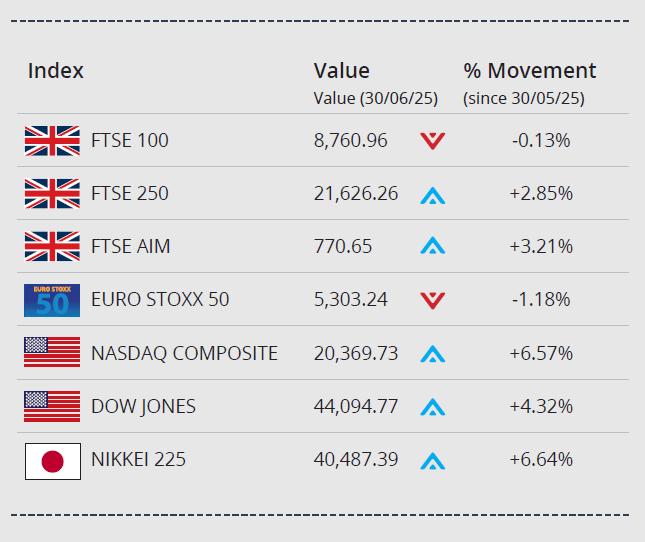

As June drew to a close, US stocks lifted amid signs of progress in trade talks, closing out a volatile H1. Hopes rose at month end that the US and its trading partners are closing in on deals as 9 July deadline approaches. Investors are closely watching Senate negotiations over President Trump’s proposed $4.5trn tax cut bill.

In the US, the Dow Jones closed the month up 4.32% on 44,094.77, while the tech-orientated NASDAQ closed June up 6.57% on 20,369.73.

In the UK, the FTSE 100 index closed June on 8,760.96, a small loss of 0.13%. The mid-cap focused FTSE 250 closed the month up 2.85% on 21,626.26, while the FTSE AIM closed on 770.65, a monthly gain of 3.21%.On the continent, the Euro Stoxx 50 closed the month 1.18% lower on 5,303.24. In Japan, the Nikkei 225 ended the month on 40,487.39, a monthly gain of 6.64%.

On the foreign exchanges, the euro closed the month at €1.16 against sterling. The US dollar closed at $1.37 against sterling and at $1.17 against the euro.

Gold closed the month trading around $3,306 a troy ounce, a small monthly gain of 0.45%. The price edged higher at month end, supported by dollar weakness, amid Senate negotiations over Trump’s tax package. Brent Crude closed June trading at around $67 a barrel, a monthly gain of over 11%. The oil price has been impacted by geopolitical uncertainty. The conflict in the Middle East hasn’t significantly disrupted supply to date.

Welfare concessions create Budget challenge

Although recently released ONS data did reveal that the UK budget deficit is currently on track to meet official forecasts, government concessions regarding the Welfare Bill inevitably look set to make the Chancellor’s Budget balancing act more challenging.

The latest public sector finance statistics showed government borrowing in May totalled £17.7bn; this was £700m higher than May last year and the second highest amount ever recorded for that particular month. It did, however, leave borrowing after two months of the current fiscal year, £2.9bn below the Office for Budget Responsibility’s latest forecast, which was produced for the Spring Statement in March. ONS noted that revenue from Income Tax and National Insurance (NI) contributions rose, partly due to April’s hike in employer NI rates.

While below forecast year-to-date borrowing figures would certainly have been welcome news for the Chancellor, the subsequent enforced U-turn on disability benefits has created a significant problem. Estimates suggest the concessions will reduce the potential savings from the Welfare Bill by around £3bn in 2029-30. This is therefore expected to make it more difficult for the Chancellor to meet her self-imposed fiscal rules without raising taxes as she makes preparations for the government’s second Budget due to be delivered this Autumn.

Retail sales fall sharply

The latest official set of retail sales statistics revealed a significant drop in sales volumes during May, while more recent survey data points to a potentially disappointing performance in June and July too.

Figures released last month by ONS showed that retail sales volumes fell by 2.7% in May; this represents the sharpest monthly fall since December 2023. While analysts had been predicting weaker demand after consumers spent heavily during the previous month, May’s decline was much larger than economists had been forecasting.

Commenting on May’s weak performance, ONS said it was largely due to a ‘dismal month’ for supermarkets, with feedback from food retailers talking of inflation and customer cutbacks, alongside reduced sales of alcohol and tobacco products. ONS also noted that both clothing and household goods stores had reported ‘slow trading.’

Evidence from the latest CBI Distributive Trades Survey also suggests retailers feel trading conditions remained tough entering the summer months, with its annual retail sales gauge dropping to -46 in June from -27 in May, while retailers’ expectations for sales in the month ahead (July) fell to -49. The CBI also noted that ‘many’ surveyed firms reported that ‘consumer caution continues to hold back sales.’

All details are correct at the time of writing (01 July 2025)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from, taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.

Realistic pricing is essential as the housing market faces seasonal price dips and increased regional competition

UK consumer confidence dips due to inflation and job concerns, leading to cautious spending and economic pressure

Early summer heat boosts spending, especially among Millennials, despite growing reliance on credit and uneven financial planning

“Realistic pricing will remain key in the coming months”

Average asking prices dipped by 0.3% in June, according to Rightmove’s June 2025 House Price Index. The dip suggests an unusual seasonal decline as sellers respond to heightened competition and affordability pressures. The £1,277 drop brings the average new seller asking price to £378,240, reversing the record highs seen in April and May.

Rightmove noted that prices typically rise by 0.4% in June, making last month’s fall notable. Regional differences are significant. Higher-priced areas such as London and the South have seen larger reductions, driven by increased supply and Stamp Duty costs. By contrast, more affordable regions including the North West, Wales and Yorkshire & The Humber have continued to see modest price growth.

Buyer demand remains resilient, up 3% year-on-year, while new listings are 11% higher than this time last year. With increased choice, the market is highly price-sensitive and properties priced correctly continue to attract strong interest. Rightmove data shows homes that attract an enquiry on the first day of marketing are 22% more likely to find a buyer than homes taking more than two weeks to receive their first enquiry.

“Agents have been telling us that sellers need to set a competitive price to have a better chance of finding a buyer in the current market, and it looks like many are listening,” said Colleen Babcock, Property Expert at Rightmove, adding “Realistic pricing will remain key in the coming months.”

Rising costs and job worries dent UK consumer confidence

UK household confidence weakened in June, with concerns over inflation and job security weighing on sentiment. S&P Global’s latest consumer sentiment index fell to 45, down slightly from 45.2 in May, marking a two-month low. The index for household spending dropped from 38.2 to 37.4, while the measure of job security slipped below the neutral 50 mark to 49.2. Readings below 50 indicate a deterioration in confidence.

The data suggests households are holding back on major purchases, choosing to focus on essentials instead. With an increasing reliance on credit and little sign of inflation pressures easing, consumers appear to be taking a more cautious approach. The findings raise questions over the strength of the UK’s consumer-led recovery, as households continue to feel the squeeze.

“Pessimism among UK households shows no signs of improving,” said Maryam Baluch, Economist at S&P Global Market Intelligence. “Concerns about making ends meet have intensified due to high prices and job insecurity… which will limit willingness to spend and instead encourage greater financial caution, dampening economic growth.”

Heat triggers spending as summer starts early

Britons dipped into their summer budgets earlier than usual, after warmer spring weather prompted a rise in seasonal spending. Research from TSB suggests a third of people surveyed started spending sooner this year.

While 70% of Brits save in advance for summer, only a fifth do so every month and just 1% start more than six months ahead. Millennials are the most financially prepared, with 47% actively planning and saving, they’re also expected to be the biggest spenders, with 28% anticipating summer outlays of between £1,000 and £2,000. Older generations are more likely to enjoy the season without much financial planning.

“With the UK summer off to a scorching start earlier than usual this year, consumer spending has been heating up too,” said Surina Somal, Everyday Banking Director at TSB. “Millennials are the biggest spenders, while younger people are more likely to rely on credit, even after saving in advance.”

Government proposes Council Tax billing changes

The government has proposed changing default Council Tax billing from 10 months to 12 months. Currently, Council Tax is automatically set up to be paid in 10 monthly instalments, from 1 April to 1 January, with no payments in February and March. However, under proposals published in June, the government has suggested 12 monthly payments become the default. Ministers said the change will assist households in managing their finances – although households will still be able to choose to pay over 10 months. The proposal is one of several up for debate in a Council Tax consultation published by the government in June. The consultation sets out how the government intends to modernise the administration of Council Tax ‘to deliver a fairer and more efficient system for taxpayers and local government.’

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (2 July 2025)

The UK property market experienced a boost in 2024, with nearly 50% of homes listed receiving offers or selling

Cities like Sunderland, Leicester, and Liverpool saw notable increases in buyer activity, while London’s growth was subdued

Rising buyer confidence, stabilising mortgage rates and positive market conditions are expected to keep demand strong

The UK property market saw a significant rise in activity in 2024, with nearly half of all homes listed for sale either receiving an offer or being sold subject to contract1.

The data shows that Sunderland led the way, recording a 10% increase in homes finding buyers compared to the start of the year. Leicester followed closely with a 9% rise, while Liverpool (8%), Newcastle (7%) and Leeds (6%) also saw notable growth. Other cities experiencing strong demand included Manchester, Sheffield and Bristol. In Scotland, Aberdeen saw buyer activity levels increase by just 0.2%, the lowest increase of all cities.

Capital lags behind

London, however, failed to break into the top ten, with a relatively modest 3.3% increase in market activity. Despite this, the capital’s housing market remained active, though less dynamic than other major cities.

Increased confidence

The data highlights a broader trend of rising buyer demand across the country. Market conditions have continued to improve, with increased confidence from both buyers and sellers. Factors such as stabilising mortgage rates and growing consumer confidence have likely contributed to the positive momentum.

With strong demand continuing into this year, many cities are expected to maintain their upward trajectory, keeping the housing market competitive in the coming months.

1GetAgent, 2025

As a mortgage is secured against your home or property, it could be repossessed if you do not keep up mortgage repayments.

The disparities in wealth accumulation between the generations are striking

Today, younger generations hold just 4% of total UK wealth

Almost half of UK adults worry they won’t have enough saved for retirement

Throughout our lives, we both give and receive support across generations, whether within our families or as part of society. This concept, known as the intergenerational contract, ensures that different generations support each other based on their needs and resources. However, with shifting economic conditions and demographic changes, this balance is increasingly under strain.

In addition, the UK’s population is ageing rapidly. By 2040, nearly a quarter of people will be aged 65 or older, compared to just under one in five today1.

Striking disparities

The disparities in wealth accumulation between generations are striking. Over the last two decades, UK household wealth has doubled relative to incomes, but older generations have benefited disproportionately. Between 2010/2011 and 2019/20, median total wealth for those aged 65 to 69 rose by 46% (£112,597), while those in their late 30s saw only a 9% increase (£6,751). Today, younger generations hold just 4% of total UK wealth, down from 7.5% in 2010. Despite this, seven in ten adults receive no financial support from their families.

Concerns about financial security

A recent survey2 highlights growing concerns about financial security. Almost half (47%) of UK adults worry they won’t have enough saved for retirement, rising to 60% among those aged 25 to 49.

With nearly a third (29%) of people fearing they won’t have family members to rely on for support, it is crucial to think about how wealth is shared across the generations.

Secure your family’s financial future

If you’re concerned about intergenerational wealth and how best to support your loved ones, talk to us about strategies for effective wealth transfer and long-term financial planning. By making informed decisions now, you can help create a more secure financial future for the generations to come.

1&2ILC 2025

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

The Bank of England held Bank Rate at 4.25%, citing economic uncertainty and softening in labour data

UK inflation remains stable, though food prices, especially chocolate, continue rising faster than other goods

Numbers of interest-only mortgages drop sharply, suggesting improved lending standards and lower exposure to risky loans

“The world is highly unpredictable”

Last week, the Bank of England (BoE) retained Bank Rate at 4.25%. The BoE’s Monetary Policy Committee (MPC) was split, with three members voting for a 0.25 percentage point cut to 4% and six members supporting no change.

Despite the decision, BoE Governor Andrew Bailey insisted rates are on a “gradual downward path” before adding, “The world is highly unpredictable. In the UK we are seeing signs of softening in the labour market. We will be looking carefully at the extent to which those signs feed through to consumer price inflation.”

Tensions between Israel and key oil producer Iran, have sparked fears that energy prices could climb, fuelling inflation and influencing future interest rate decisions. BoE Deputy Governor Clare Lombardelli said ongoing “uncertainty facing the economy” was a key reason for holding interest rates steady this month. Calling developments in the Middle East “deeply worrying,” she added, “As you’d expect, we are monitoring carefully those events and the impact.” The next MPC Bank Rate decision is due on 7 August.

In fact, oil prices experienced a sharp decline on Tuesday following the announcement of a ceasefire between Israel and Iran, alleviating concerns over potential disruptions in the Middle East’s oil supply.

Inflation “little changed”

New data from the Office for National Statistics (ONS) showed the Consumer Prices Index (CPI) rose by 3.4% in the 12 months to May 2025, compared with 3.5% in the 12 months to April. The rate is expected to rise to 3.5% again later this year, before falling back to around 2.1% next year.

During May, food, furniture and household goods prices ticked up. Notably, food price inflation increased from 3.4% in April to 4.4%, with chocolate prices in particular rising at a record rate. Air fares fell 5.0% in the month, compared to a large increase of 14.9% between April and May in 2024.

And in the US…

As anticipated, the US Federal Open Market Committee announced no change in its monetary policy last week. The Federal funds borrowing rate remains in its current range of 4.25-4.50%, holding steady since President Trump took office in January. The Federal Reserve last cut rates in December 2024, reducing them by 0.25 percentage points. During the press conference, Fed Chairman Jerome Powell said the Reserve are “well positioned to wait and learn more about the likely course of the economy before considering any adjustments to our policies.”

Interest-only mortgage stock reduces

According to new data from UK Finance, the number of interest-only homeowner mortgages in the UK fell by 17% last year, continuing a steady decline since 2012. The total number of these loans has dropped by 78% over the past 12 years, with their overall value falling by 61%.

By the end of last year, there were 541,000 pure interest-only mortgages outstanding – 18.5% less than in 2023. Partial interest-only loans totalled 174,000, marking a 13% annual decrease. High loan-to-value (LTV) loans (above 75%), declined by 25.7%, now making up just 5% of the total, compared to 36% in 2012. This suggests improved portfolio quality and stronger risk management.

The number of interest-only loans due to mature by 2027 fell significantly, down 35.8% to 120,000, driven by successful transitions and early repayments.

Director of Mortgages at UK Finance, Charles Roe, commented, “It is particularly encouraging that the number of interest-only loans at higher loan-to-value ratios has fallen sharply… with a similar movement in those loans set to mature over the next two years.”

Consumer confidence

The GfK Consumer Confidence Index rose by 2 points to -18 in June 2025, supported by improvements in how consumers view the general economy, with this specific measure rising by five points in the month to -28, although 17 points lower than the June 2024 reading. Meanwhile, the major purchase index reading was unchanged at -16 this month, 7 points higher than this time last year.

Neil Bellamy, Consumer Insights Director at GfK, noted that due to the daily challenge of inflation, “confidence is still fragile” and islikely to be exacerbated by rising fuel prices due in part to an escalation of the Middle East conflict. Combined with “ongoing uncertainty as to the full impact of tariffs, there is still much that could negatively impact consumers.”

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (25 June 2025)

May 2025 saw the busiest agreed home sales since 2022, led by post-Stamp Duty change recovery

Prime Central London prices fall 2.2% annually as tax changes hit international demand

Government pledges £39bn over 10 years for affordable housing in largest investment in 50 years.

May sales hit post-2022 high as housing market regains momentum

Rightmove says May 2025 was the busiest month for agreed sales since March 2022.

The rush to complete before April’s Stamp Duty changes caused a spike in March, followed by a 4% dip in buyer demand and the slowest annual May price growth since 2016. Despite this pause, home-movers have quickly returned. Sales agreed were up 6% year-on-year across Great Britain, with Wales leading at +15% and London showing more modest growth at +1%. May’s figures also mark the most active May since 2021, suggesting growing confidence among buyers and sellers adjusting to the new tax and borrowing landscape.

Rightmove’s earlier data pointed to a more stable market with the post-deadline adjustment period giving way to renewed momentum. Buyers appear more willing to press ahead, even with higher costs, suggesting resilient housing demand across much of the country.

Price cuts return in Prime Central London as demand softens

Sellers in Prime Central London are reducing prices to tempt buyers, following tax changes.

Knight Frank reports average prices in Prime Central London fell 2.2% in the year to May, the sharpest annual decline since August 2024. Sales activity has also dipped, with transactions in London’s prime markets down 7% over the past six months compared with the previous year. Lack of demand is being blamed on recent changes to the UK’s non-dom tax regime and the introduction of a higher Stamp Duty on additional properties.

However, the picture is more stable in Prime Outer London, where buyers are more likely to be domestic and driven by need rather than investment. Prices there rose 1.1% over the same 12-month period. The growing divergence between central and outer prime markets suggests changes to tax policy are having a more pronounced impact on discretionary, internationally focused buying behaviour.

Spending review – the impact on housing

Chancellor Rachel Reeves has announced a tenyear, £39bn investment in affordable and social housing across England as part of the 2025 Spending Review. The Chancellor called the investment “the biggest cash injection into social and affordable housing in 50 years.”

With plenty of scepticism about Labour’s ability to deliver on a manifesto promise to build 1.5 million homes in five years, new analysis from JLL suggests they could get closer than originally thought if they can squeeze 500,000 homes out of the cash injection.

Nick Whitten, EMEA Head of Living Research at JLL, said, “A £39bn pledge for new affordable housing over the next decade is the largest government commitment we’ve seen in half a century – and one that has to be commended at a time when the public purse is more than a little stretched. But while the ambition is clear, the reality is complex.”

Festival hotspots come with a housing premium

New Yopa research suggests living near major UK music festivals comes with property premium.

Analysis of 20 festival postcodes found average house prices of £382,072, 41% higher than the UK average. The steepest increase is found near Leeds Festival. Homes in the LS22 postcode average £466,244, a full 91% higher than the wider Leeds area. Creamfields isn’t far behind, with WA4 prices sitting 89% above the Halton average.

Other festival locations also carry notable uplifts. House prices in CA10, home to Kendal Calling, are 40% above the Westmorland and Furness average, while Liverpool’s L17 postcode, which hosted Radio 1’s Big Weekend, is 30% higher than the city average. Reading Festival bucks the trend, with RG1 house prices 20% below the wider local average. Still, Yopa’s findings suggest that, for many, living near a festival site means paying more for having music on your doorstep.

All details are correct at the time of writing (18 June 2025)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.

City of London investment triples year-on-year, led by State Street’s £382m office acquisition

The retail sector rebounded strongly in April, but inflation and falling confidence weigh on outlook

The Scottish property market is steady, with largest average deal sizes seen in nearly three years

City investment rebounds with biggest deal in over a year as recovery continues

London City’s investment market continued its recovery in April according to Savills.

Its City Investment Watch reported £485.9m transacted across four deals in April, bringing total year-to-date volume to £1.35bn across 20 transactions. This was triple the total in April 2024, although still 28% below the five-year average. These bigger deals are crucial, typically accounting for around 70% of the City’s annual turnover and the return of larger deals is helping to lift volumes.

The standout was State Street’s £382m purchase of 100 New Bridge Street, the City’s largest deal since March 2023. The 194,000 sq. ft development is due to complete in early 2026 and will become State Street’s new London headquarters. Savills is currently tracking over £1bn under offer, suggesting further signs of confidence in the market ahead.

Retail investment bounces back in April but confidence remains fragile

The retail sector rebounded sharply in April according to Colliers.

Retail investment volumes rose from a revised £380m in March to £1.1bn in April, well above the five-year monthly average of £680m, according to Colliers’ May Property Snapshot. The strong month lifted the year-to-date total to £2.4bn, broadly in line with 2024. One of the biggest transactions was Farren Investments’ £114m purchase of Lakeside Retail Park in Grays at a 6% yield.

On the occupier side, April brought a modest recovery in sales volumes, up 1.2% on the month and 5% year-on-year. Volumes are now slightly above pre-pandemic levels. However, higher retail price inflation and a fall in consumer confidence to a 17-month low highlight the fragile backdrop. Retail rents rose 2% year-on-year, while nine retailers have entered administration in 2025, impacting 283 stores across the country.

Scottish property investment steadies as average deal size hits three-year high

Scotland’s commercial property market saw a steady first quarter, with investment volumes totalling £430m, according to Colliers.

While down from £520m in Q4 2024 and 7% below the five-year average, Q1 2025 volumes were ahead of the same period last year. A total of 27 deals were completed and the average lot size reached £16m, the highest in nearly three years. Offices and apartments, including purpose-built student accommodation, accounted for 70% of activity.

The largest transaction was Pontegadea’s £75m acquisition of a core office at Capital Square in Edinburgh, reflecting a net initial yield of 5.75%. Glasgow led the quarter with nearly £220m in deals, followed by Edinburgh at £170m and Aberdeen at £120m. While short-term risks persist due to global uncertainty, Colliers expects that falling debt costs and likely interest rate cuts will support a market recovery later in the year.

Hybrid tensions drive office ‘rightsizing’ as businesses seek better space use

Knight Frank’s 2025 Your Space survey reveals a corporate real estate sector still in transition.

The survey gathered insights from 300 global corporate real estate leaders overseeing more than 650 million sq. ft of space. As hybrid work patterns have disrupted office use, firms are responding by ‘rightsizing’ rather than retreating. More than a third of senior leaders reported being dissatisfied with how much of their workplace was being used, with inconsistent attendance leaving large areas underutilised.

Improving how offices are used and matching space to how people work were top challenges, with 55% of respondents agreeing rightsizing their property portfolio was their biggest concern. Half expect their real estate footprint to grow over the next three to five years, potentially adding 104 million sq. ft globally, while just 20% anticipate a reduction. Companies are also building flexibility into their strategies through shorter leases, modular formats and diversified locations.

All details are correct at the time of writing (18 June 2025)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.

The Spending Review included: NHS to receive £29bn a year extra and £39bn over 10 years for social housing

GDP dropped by 0.3% in April, highlighting ongoing economic fragility and the biggest drop since October 2023

President Trump signed an executive order to reduce tariffs on UK cars being shipped to the US

“We are renewing Britain”

Last week, Rachel Reeves presented her Spending Review to set out day-to-day spending for the next three years and capital spending plans for the next four years. Stating her focus was on the nation’s health, security and economic growth,the Chancellor took to the dispatch box saying, “We are renewing Britain… but I know too many people in too many parts of our country are yet to feel it.”

One of the most anticipated announcements was on the National Health Service, which Reeves described as “our most treasured public service.” She confirmed that spending on the NHS will rise by 3% a year after inflation – “an extra £29bn per year for the day-to-day running of the health service.” Increasing the NHS technology budget by 50%, she pledged £10bn of investment to “bring our analogue health system into the digital age, including through the NHS app.”

On housing, Reeves allocated £39bn to fund social and affordable housing over the next ten years, saying this was “the biggest cash injection into social housing in 50 years.” The core schools’ budget was increased by £2bn in real terms over the Review period. For training and upskilling, £1.2bn will go towards supporting young people into apprenticeships and training schemes.

Funding of £7bn will be made available for 14,000 new prison places and there will be an increase in police spending averaging 2.3% each year. Border security funding is set to be increased, with up to £280m extra a year by the end of the Review period.

Some elements shared before the Review, included:

An increase in defence spending – to 2.5% of GDP by 2027 (2.3% currently). A £5bn a year uptick

An extension to free school meals for 500,000 more children (whose parents receive Universal Credit, irrespective of their income)

A U-turn on Winter Fuel Payments – now to be paid to three quarters of pensioners in England and Wales in 2025

An increase in science and technology spending – £86bn pledged by the end of the Parliament

An extension to train, bus and tram investment – £15.6bn made available for improvements

An investment in the Sizewell C nuclear power station – £14.2bn to construct this plus £2.5bn to build the UK’s first Small Modular Reactors.

Chief Executive of the Confederation of British Industry (CBI) Rain Newton-Smith said the Review, “Signals a downpayment on hardwiring the growth mission into government priorities. Against a challenging backdrop, the choice to prioritise investment in clean energy, R&D, as well as delivering a much-needed boost to housing, transport and infrastructure is the smart play that will raise the long-term ceiling of the economy.”

She continued, “The litmus test will be following through on delivery in partnership with industry at pace. That must be underpinned by a comprehensive strategy for driving investment in adult skills and addressing high energy costs, which were missing from today’s announcement.”

The Spending Review was set against the backdrop of employment data from the Office for National Statistics (ONS) showing a weakening labour market – available jobs fell by 63,000 between March and May 2025 and the unemployment rate ticked higher. There was a reduction in the number of payrolled employees in May, with early estimates indicating 30.2 million, a fall of 0.9% from May 2024.

April GDP takes a slide

ONS revealed on Thursday that monthly real gross domestic product (GDP) is estimated to have fallen by 0.3% in April 2025, marking the biggest monthly drop since October 2023 against a predicted 0.1% reduction. This follows growth of 0.2% recorded in March. Real GDP is estimated to have grown by 0.7% in the three months to April 2025, compared with the three months to January 2025. Commenting on the data, Keir Starmer said he was “not satisfied with growth” and that the downgraded forecast “just spurs them on.”

Parts of UK-US tariff deal confirmed

On Monday, President Trump signed an executive order to reduce tariffs on UK cars being shipped to the US, which will bring into force parts of a tariff deal agreed between the two countries last month. Speaking at the G7 summit in Canada, the Prime Minister called the move a “very important day” for both countries.

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (18 June 2025)