| London’s data centre demand is set to hit record highs in 2025, driven by hyperscalers and AI providers | Retail property investment rebounded strongly in Q2, with high-street demand at its highest since 2021 | UK commercial property remains mixed, with stronger growth in Central London offices and industrial rental markets |

Take-up of data centres in London is forecast to hit new highs in 2025, according to CBRE.

The capital is expected to see take-up of 183MW (mega watts) of power capacity this year, 58% more than in 2024 and double the 2021 total. This spike is largely driven by hyperscalers, but requirements from artificial intelligence (AI) providers are also beginning to dominate the demand for capacity.

Electricity is more expensive in the UK than in other European countries, however investors continue to be attracted to London due to its established ecosystem. Currently, around 80% of all UK data centres are found in the capital and its surrounding areas.

Providers in London are struggling to keep up with the demand for data centres. Nearly all the new space expected this year will be accounted for before it is complete. As a result, the capital’s vacancy rate is anticipated to fall to 8% by the end of 2025.

Retail investment makes a strong comeback

The retail property sector saw a bounce back in investor interest in Q2.

According to Rightmove, retail investment demand was 35% higher between April and June than the same period last year. This marks a positive shift for the sector, which had seen a lull in interest from investors since 2022, with demand down 15% year-on-year in Q2 2024. The rebound is driven by high-street investment demand, which has gone up by 56% annually to the highest level since 2021.

Meanwhile, supply levels in the retail sector have been decreasing since the beginning of 2024, now 4% lower than a year ago. This limited availability may have helped to increase demand for retail properties on the market.

Andy Miles at Rightmove commented, “Rate cuts are helping investment into commercial property and after a period of decline it appears that retail and office spaces are becoming more attractive to invest in.”

RICS’ sector overview

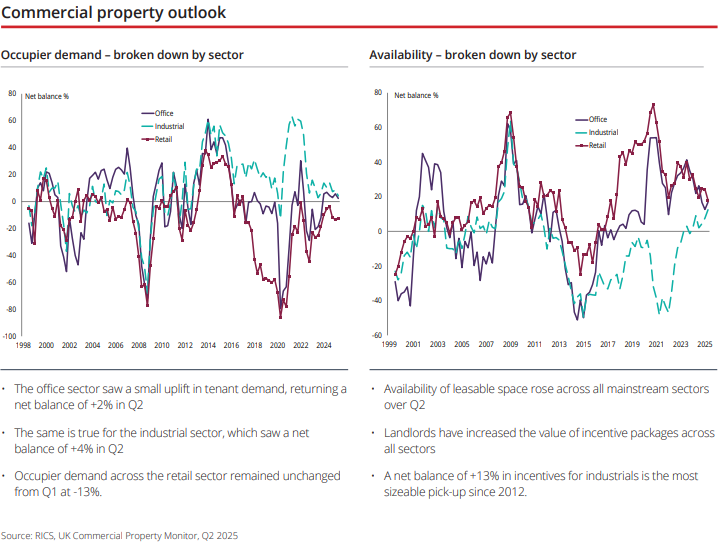

The latest analysis from the Royal Institution of Chartered Surveyors (RICS) shows that overall, the UK commercial property market was largely stagnant in Q2 2025.

Occupier demand dipped slightly when compared with the previous quarter, with net balance figures showing marginal changes of +2% for offices and +4% for industrial property.

Conditions for the office sector are much more positive in Central London, where occupier demand is stronger than the national average. Meanwhile, vacancies rose in sectors across the country, prompting landlords to offer incentives to bring in tenants.

Looking ahead, RICS survey respondents were divided on what’s to come, with 35% believing the market is moving upwards and the same proportion expecting it to take a downturn. However, most did agree that the office and industrial sectors will see growth in rental prices in the coming year.

Scottish market update

Scotland’s commercial property market showed some resilience in Q2, even as the wider economy contracted.

According to the Scottish Government, onshore GDP fell by 0.2% in May due to fluctuating business confidence. Meanwhile, Colliers reported that investment volumes fell from £560m in Q1 to £370m in Q2, about 22% lower than the five-year quarterly average but similar to Q2 2024 levels. There were some positive signs, as investment transaction volumes were 20% higher in H1 2025 than in the same period in 2024.

So far this year, the office sector has accounted for the largest share of investment activity (25%). Despite this, office investment slowed to £100m, the lowest quarterly figure in over a year. The largest deal came from property investment firm, Pontegadea, which bought Capital Square in Edinburgh for £75m. Meanwhile, prime yields in city centres remained steady in Edinburgh (6.50%) and Glasgow (6.75%).

All details are correct at the time of writing (20 August 2025)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission