A third of homeowners are currently making overpayments on their mortgage

40% of homeowners don’t have the confidence to overpay their mortgage

Most lenders allow you to make overpayments of up to 10% of your mortgage balance each year without incurring any penalties

UK homeowners could collectively save £2.3bn on mortgage interest each year by making overpayments, but they need help to make the first move.

According to recent research1, homeowners could be making combined annual overpayments worth £5.3bn, but 40% say they lack the confidence to take the plunge. As a result, only a third are currently making overpayments on their mortgages.

Pay your own way

Most lenders allow you to make overpayments of up to 10% of your mortgage balance each year without incurring any penalties. When you make an overpayment, it doesn’t just reduce the total interest paid but also the overall term.

An overpayment could be a large one-off sum or a small regular payment: even as little as £50 a month can add up, as the research revealed. Based on an average mortgage of £195,000 (unspecified term), a homeowner could save a total of nearly £7,000 in interest and cut their loan by one year and 10 months by paying £50 extra per month.

In your best interests

Thousands of homeowners could be tapping into these benefits, but a third of the people not making overpayments say they are being held back due to ‘friction or a lack of understanding’ about the impact.

With some mortgages now lasting up to 40 years, 69% of first-time buyers are keen to reduce their debt, term or interest. Although overpayments could help them achieve this goal, it’s important to consider other financial commitments. We can help you determine if mortgage overpayments may be suitable for you.

1Monzo, 2025

As a mortgage is secured against your home or property, it could be repossessed if you do not keep up mortgage repayments. Financial protection policies typically have no cash-in value at any time and cover will cease at the end of the term. If premiums stop, then cover will lapse.

Only 30% of those aged 30 to 34 and 34% of those aged 35 to 39 have enough life cover to protect their family

Households often insure mortgages but neglect cover for children and dependents

The ‘squeezed middle’ must prioritise protection to avoid future shortfalls

People in their 30s and 40s are falling into the ‘protection gap,’ new research1 suggests, but getting the right cover for your needs is achievable.

Squeezed middle

Only 30% of those aged 30 to 34 and 34% of those aged 35 to 39 have enough life cover to protect their family, the figures show. People in these age ranges are often referred to as the ‘squeezed middle,’ due to the combination of paying for a mortgage, children and other dependants.

Protecting dependants

Although the fact they face many other pressures can help explain why people in the ‘squeezed middle’ may be neglecting protection, these same factors also make the need for robust safety nets especially important. Alarmingly, the survey found that just 26% of couples with children have adequate cover.

Likewise, only 36% of households with a mortgage have enough cover. The research also noted that, in many cases, it is not the mortgage itself that is not adequately insured; instead, many households seem to pay for life insurance to cover mortgage costs but then stop short of considering support for their children.

Don’t risk a shortfall

When it comes to protection, it’s certainly true that it’s better to be safe than sorry. The ‘squeezed middle’ face many pressures and often end up making sacrifices, but having the peace of mind and financial security that protection offers should not be one of them. We can source suitable cover for your circumstances.

1HL, 2025

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. Financial protection policies typically have no cash-in value at any time and cover will cease at the end of the term. If premiums stop, then cover will lapse. As a mortgage is secured against your home or property, it could be repossessed if you do not keep up mortgage repayments.

The Autumn Budget is on 26 November, with speculation over new taxes as borrowing costs hit 25-year highs

The UK services sector grew strongly in August, reaching its highest activity level since April 2024, easing earlier concerns

Retail sales rose 0.6% in July, but mortgage borrowing dipped, signalling subdued growth risks for the economy

“Britain’s economy isn’t broken, but I do know that it’s not working well enough for working people”

Chancellor Rachel Reeves has confirmed that the Autumn Budget will take place on Wednesday 26 November, nearly a month later than last year’s Budget. Many economists have warned that tax rises or spending cuts are likely to be announced.

Reeves is currently under mounting pressure to address the gap in the public finances while adhering to Labour’s promise not to increase taxes on ‘working people,’ including VAT, Income Tax and National Insurance. Last week, long-term borrowing costs reached their highest level since 1998, making it increasingly expensive to service government debt.

The Chancellor has self-imposed borrowing rules that she needs to align with; to cover day-to-day costs using tax revenues instead of borrowing by 2029/30 (the stability rule) and to reduce net financial debt as a share of the economy (the investment rule). These goals leave Reeves with a relatively small financial buffer.

The Office for Budget Responsibility (OBR) will deliver a new baseline forecast later this month, assessing long-term productivity. It will also advise the Treasury on what action needs to be taken to adhere to the fiscal rules. There is speculation that the Budget could bring a new tax on landlords, a windfall tax on bank profits or reform to the Council Tax system.

In a speech last week, Reeves said, “Britain’s economy isn’t broken, but I do know that it’s not working well enough for working people. Bills are too high and you feel that you’re putting more in, but you’re getting less out, and that has to change.”

Last week was a busy one in Westminster, on Friday Angela Rayner resigned from her role as Deputy Prime Minister and Housing Secretary after investigations found that she underpaid Stamp Duty. This prompted a reshuffle of the Cabinet, with David Lammy appointed as the new Deputy PM. Ms Rayner was also the Labour Party’s Deputy Leader, so a deputy leadership election is underway; nominations will close on Thursday 11 September, voting will start on 8 October and close on 23 October, before a result is announced on 25 October.

Services sector enjoys ‘solid upturn’

In August, UK services saw a spike in activity, with the sector scoring 52.5 in the S&P Global Purchasing Managers’ Index. This is the highest level since April 2024 and up from 51.8 in July. Any reading above 50.0 indicates growth, so the results will be welcome news for businesses in the service sector, which includes hospitality, property, healthcare and education.

Responses to the survey suggest that concerns about US tariffs have eased, but there is uncertainty surrounding further tax rises in the UK. Economics Director at S&P, Tim Moore, commented, “August data highlights a welcome acceleration of output growth and a swift rebound in order books after July’s dip, leaving the UK service economy on a much stronger footing as the end of summer comes into view.”

Retail sales rose in July

According to the Office for National Statistics (ONS), retail sales volumes increased by 0.6% in July, exceeding analysts’ expectations. Key drivers of growth were online retailers and clothing stores – this has been attributed to good weather, new products and the Women’s Euros tournament. Despite this monthly rise, sales volumes in the three months to July 2025 fell by 0.6% when compared with the three months to April. This comes after a slowdown in spending for supermarkets, sports shops and household goods stores, despite these subsectors having a strong start to the year.

Dip in mortgage borrowing

Mortgage borrowing decreased in July according to the Bank of England’s Money and Credit report. Mortgage debt by individuals fell by £0.9m to £4.5bn, a marked difference from June which saw a £3.2bn increase to £5.4bn. Meanwhile, there was a small rise in net mortgage approvals for house purchases, which rose by 800 to 65,400, although remortgage approvals decreased by 2,700 to 38,900.

Chief UK Economist at Capital Economics, Paul Dales, said, “These figures broadly support our view that the economy will grow at a subdued pace over the second half of this year, with possible tax rises in the Budget being an extra downside risk.”

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have.

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (10 September 2025)

Nearly 4 in 10 people in the UK are not on track for even a basic retirement lifestyle

Understanding retirement income targets is key to building financial resilience

Personal pensions offer flexibility, tax relief and control – ideal for employed and self-employed people.

Building financial empowerment is all about the confidence that comes from knowing you are in control of your finances. As more savers risk falling behind on their retirement goals, proactive pension saving is in the spotlight.

Retirement plans

With cost-of-living pressures weighing on many households, building a retirement fund has understandably taken a back seat for many savers. As a result, according to a new survey1, 39% of Brits are not on track for a ‘minimum retirement lifestyle,’ up from 35% in 2023.

Feel empowered

The first step to taking control of your pension goals is to understand how much you will need in your retirement. As a general guide, the Pension and Lifetime Savings Association (PLSA) estimates that a single person would need £13,400 a year for a minimum lifestyle standard in retirement (£21,600 for a couple). Note that this is for people living outside London and excludes housing costs. For a moderate lifestyle, these figures increase to £31,700 (single person) and £43,900 per annum (couple).

Know your options

Effective planning, starting early and contributing regularly allows your pension pot to build over time. For employees, saving into a defined contribution pension can help your pension pot build up, as your employer also makes contributions. It’s worth checking if you could pay more than the minimum amount. Self-employed workers have fewer options, which is why two in five say they aren’t saving enough for retirement, and 23% are not saving anything at all. Personal pensions are an option for everyone, and like all pensions, offer tax relief, long-term savings growth potential, financial security in retirement and control over investment choices.

Take the first step

Feeling empowered to make informed decisions leads to proactive steps towards a financially resilient future. While challenges remain, your retirement is too important to neglect – it’s time to take control and feel empowered! You can’t afford not to.

1Scottish Widows, 2025

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. A pension is a long-term investment not normally accessible until 55 (57 from April 2028). The value of your investments (and any income from them) can go down as well as up.

40% of life insurance policies in the UK are joint rather than individual

Joint life insurance policies can prove problematic when a relationship breaks down

Dual life cover offers separate, flexible protection for both partners

You’ve opened a joint bank account. You’ve signed up for a joint mortgage. So, a joint life insurance policy might seem like an obvious next step. According to research1, 40% of life insurance policies in the UK are joint rather than individual.

Joint policies provide life insurance cover for two people but pay out only once, typically after the first death. The policy is then terminated, which can leave the surviving partner without cover. Depending on their age and medical history, taking out a replacement individual policy could be challenging.

Breaking up is hard to do

Joint life insurance policies can also prove problematic when a relationship breaks down, as both parties need to consent to a change or cancellation.

They can also inadvertently become tools for economic control or abuse, limiting one partner’s financial independence and life choices. According to research2, 40% of UK adults may have suffered some form of financial or economic abuse.

A new lease of life for insurance

Dual life insurance cover is an alternative to individual and joint policies. Although the application process and quote are combined, the cover for each partner is separate, which means policies can be retained even if a relationship breaks down or one person dies. If both policyholders die, this can result in two payouts, offering greater financial security to any dependants.

1Money Expert, 2025, 2Aviva, 2025

Financial protection policies typically have no cash-in value at any time and cover will cease at the end of the term. If premiums stop, then cover will lapse.

UK GDP growth outperformed expectations in Q2, but fragile demand raises concerns over sustainability into autumn

Bank of England cut rates to 4%, yet divisions among policymakers signal slower easing ahead

Inflation climbed to 3.8% in July, with rising transport, food and energy costs fuelling pressure

UK growth rate beats expectations

Second quarter data released last month by the Office for National Statistics (ONS) confirmed that UK economic growth did slow between April and June after an unusually strong expansion during the first three months of the year.

According to the latest official statistics, UK economic output rose by 0.3% across the whole of the second quarter. However, while this figure did represent a significant slowdown from a first quarter growth rate of 0.7%, it was notably higher than economists had been predicting with the consensus forecast from a Reuters poll pointing to growth of just 0.1%.

This stronger than expected performance was partly due to upward revisions to data in the first month of the quarter, with updated figures showing that, rather than contracting by 0.3%, output in April actually fell by a more modest 0.1%. The economy also performed better than analysts had been expecting in the quarter’s final month – output in June was estimated to have risen by 0.4%, driven by growth across all three main sectors of the economy.

Survey evidence also points to a more recent pick-up in activity. Last month’s preliminary headline growth indicator from the closely-watched S&P Global UK Purchasing Managers’ Index (PMI), for instance, rose to 53.0 in August, up from a final reading of 51.5 in July. This was the highest figure since August last year and left the index comfortably above the 50 threshold that denotes growth in private sector output.

Commenting on the findings, S&P Global Market Intelligence’s Chief Business Economist Chris Williamson said the data indicated that “the pace of economic growth has continued to accelerate over the summer after a sluggish spring.” He did though add a note of caution by stating that the survey’s measure of order books highlight both an “uneven and fragile” demand environment.

Interest rates cut after narrow vote

On 7 August, the Bank of England (BoE) sanctioned a further quarter-point cut in interest rates, taking the cost of borrowing down to its lowest level for more than two years.

The decision, however, did require an unprecedented second vote after a first round of voting revealed a three-way split amongst policymakers on the BoE’s nine-member Monetary Policy Committee (MPC) – four of the members preferred to leave rates unchanged; four favoured a 0.25 percentage point reduction and one backed a half-point cut. The second vote produced a 5-4 majority in favour of cutting rates by 0.25 percentage points taking Bank Rate down to 4%, its lowest level since March 2023.

Speaking after announcing the committee’s decision, BoE Governor Andrew Bailey reiterated his view that the path for interest rates “continues to be downward” but added that it was important rates were not lowered “too quickly or by too much.” He also admitted that the decision to cut rates in August had been “finely balanced” and that the course of future cuts has become “more uncertain.”

The tightness of the MPC vote and clear differences in policymakers’ opinions did result in some economists suggesting the pace of any future rate cuts may slow over the coming months. Investors also interpreted the decision this way, trimming their bets on the possibility of another cut this year, with interest rate futures contracts only fully pricing in a reduction to 3.75% during the first quarter of 2026.

A Reuters poll conducted in mid-August though did show that a majority of economists currently still expect the Bank to cut rates one more time this year, with November viewed as the most likely date. The next MPC meeting is due to conclude on 17 September with the committee’s decision scheduled to be announced the following day.

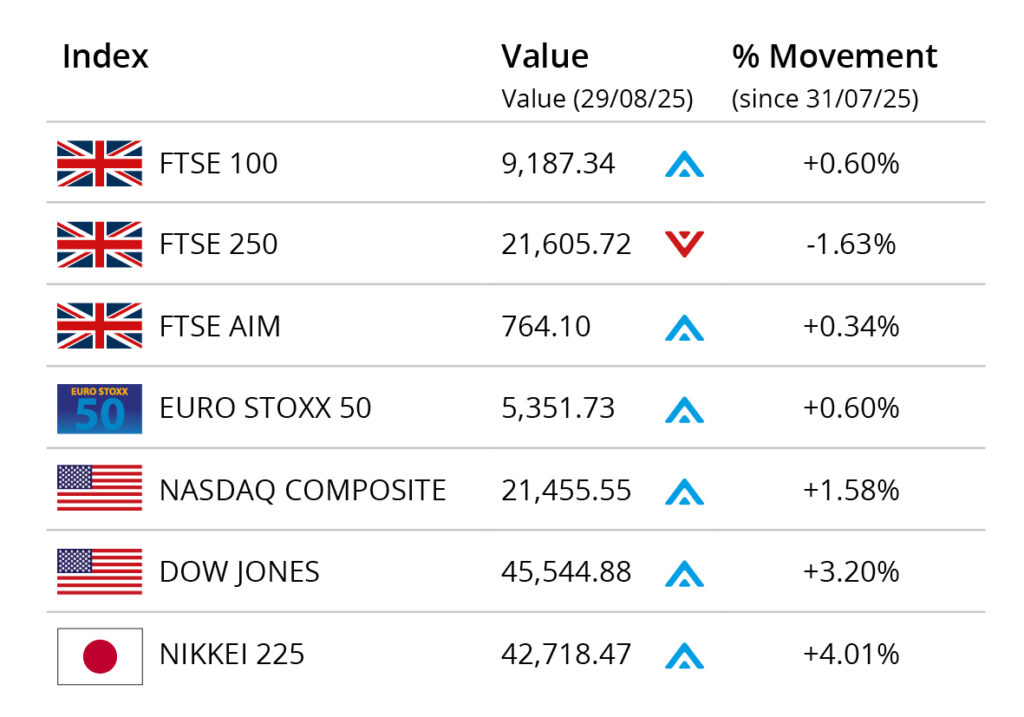

Markets

At the end of August, the FTSE 100 and European indices faltered, with US indices also weaker, as markets digested an update on consumer inflation in the States which showed prices remained stubbornly above the Federal Reserve’s target.

On home shores, the blue chip FTSE 100 closed the month on 9,187.34, a small gain of 0.60%. The mid-cap FTSE 250 lost 1.63% in August to end on 21,605.72, while the small-cap orientated FTSE AIM registered a small 0.34% gain to close August on 764.10.

In the US, the Dow Jones closed the month on 45,544.88, an uptick of 3.20% in the month, while the tech-orientated NASDAQ closed the month up 1.58% on 21,455.55. On the continent the Euro Stoxx 50 rose just 0.60% during August to 5,351.73. In Japan, the Nikkei 225 gained just over 4% to close the month on 42,718.47, with the US trade agreement and corporate reform providing support.

On the foreign exchanges, the euro closed the month at €1.15 against sterling. The US dollar closed at $1.35 against sterling and at $1.16 against the euro.

The gold price rose 4.82% during August, closing at around $3,509 a troy ounce. The price reached highs at month end, supported by heightened expectations of a September rate cut, as traders digested US economic data. Brent Crude closed the month at around $66 a barrel, recording a loss of over 6%. The price faltered at month end as traders digested weaker demand in the US and an autumn supply boost from OPEC and its allies.

Inflation rises to 18-month high

Official consumer price statistics released last month revealed another jump in the headline rate of inflation, while survey data points to a further, more recent rise in food inflation.

The latest ONS data showed that the Consumer Prices Index (CPI) 12-month rate – which compares prices in the current month with the same period a year earlier – stood at 3.8% in July. This was up from 3.6% in June and slightly higher than the consensus prediction from a Reuters poll of economists.

ONS said transport costs, particularly air fares, were the largest upward contributor to July’s rise. In addition, the cost of food and non-alcoholic drinks increased for the fourth month in a row, with prices in this sector rising to 4.9% in the year to July, the highest recorded figure since February 2024.

Survey data subsequently published by the British Retail Consortium also found that food prices continued to rise in August, while Ofgem’s recent decision to increase its gas and electricity price cap by a slightly higher than expected 2% from October will further add to consumer cost pressures. The BoE updated its inflation forecast early last month with the headline rate now expected to peak at 4% in September.

Government borrowing lower than expected

Although the latest public sector finance statistics revealed that UK government borrowing came in below expectations, the Chancellor is still expected to have to raise taxes in the Autumn Budget to meet her self-imposed fiscal rules.

Data released last month by ONS showed government borrowing in July totalled £1.1bn; this was £2.3bn less than the same month last year and the lowest July figure for three years. The better-than-expected data was helped by an increase in self-assessed Income Tax receipts, as well as a rise in National Insurance (NI) payments due to April’s employer NI rate hike.

July’s figure took cumulative borrowing across the first four months of the financial year to £60bn. While this was £6.7bn higher than in the same period last year, it was broadly in line with the Office for Budget Responsibility’s latest forecast produced in March.

Economists, however, still expect that the Chancellor will need to raise taxes this autumn if she is to meet her borrowing rules. Analysis released early last month by the National Institute of Economic and Social Research, for instance, estimated that the government is likely to miss its budget target for 2029/30 by over £40bn.

All details are correct at the time of writing (01 September 2025)

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for information only. We cannot assume legal liability for any errors or omissions it might contain. No part of this document may be reproduced in any manner without prior permission.

A dressing room can boost your home’s value by up to £40,000

Over 65’s hold £2.9trn in mortgage-free property wealth in the UK

House purchases now take 124 days on average – 41% longer than expected

Dressing rooms – the new must-have

Once seen as a luxury, dressing rooms are gaining popularity among everyday homeowners inspired by celebrities and influencers. Offering convenience and a hotel-like aesthetic, they’re becoming a sought-after feature that could boost your property’s value by up to £40,0001. Though converting a bedroom may seem wasteful, buyers now prioritise space and features over bedroom count. Experts say a stylish dressing room can make a home stand out in today’s competitive market.

Property wealth held by over 65s reaches £2.9trn

Recent research2 has revealed that more than 10 million over 65s own their homes outright, bringing property wealth owned by this age group to over £2.9trn. Around 37% of this wealth is in London and the South East. Will Hale, from Key commented, “Over 65s have considerable wealth tied up in their homes and are literally sitting on money that could give them a more comfortable or fulfilling retirement. Alternatively, this wealth could be used to provide a living inheritance and offer family members cash at a point in their lives when they need it most, for example when children or grandchildren are looking to get on the housing ladder.” Unlocking home equity is one way to boost retirement funds or help support younger generations with property deposits. Equity release isn’t suitable for everyone, it is important to take specialist advice.

Delays in house sales

The house buying process is reported to be taking 41% longer than anticipated3. Buyers expect to exchange contracts in 88 days, but it takes 124 days on average. In England and Wales, exchanges take 38 days longer than believed, and in Scotland, 32 days longer. The report concludes that digital transformation is needed to speed up the process.

1Benham and Reeves, 2025, 2Key, 2025, 3OPDA, 2025

As a mortgage is secured against your home or property, it could be repossessed if you do not keep up mortgage repayments. Think carefully before securing other debts against your home. Equity released from your home will be secured against it.

12% of HNWI’s are financially supporting both children and ageing parents

Many dip into pensions or restructure finances to fund family gifts

Balancing generosity with personal financial security is essential for long-term freedom

The ‘Bank of Mum and Dad’ (BOMAD) is well known to many aspiring or recent house buyers – but have you heard of BOSAD?

New research1 has found that, as well as supporting their own children, one in eight high earners are also taking on the role of ‘Bank of Son and Daughter’ to support their parents through rising costs and financial pressures.

Both BOMAD and BOSAD

The research reveals the interesting evolution of wealth through some families. As well as 73% of high-net-worth individuals (HNWIs) who financially support adult children, some 68% have helped their ageing parents or grandparents. Sandwiched in the middle, 12% of HNWIs are financially supporting both generations at the same time.

Prioritising number one?

By making average gifts of £7,500 per year, many kind-hearted family members are helping parents or children who might otherwise struggle with rising costs. However, this generosity can come at the expense of their own financial goals.

More than one in seven HNWIs have had to restructure their finances in order to finance their gifting, while one in eight have even dipped into their own pension savings. Meanwhile, three in 10 have had to sell or use investments and 18% say they have cut back on lifestyle spending to support others.

Getting the balance right

Helping family members meet their financial challenges without compromising your own financial future is a tricky tightrope to walk. To maximise your support for loves ones, while ensuring your own financial security, get in touch; we can talk through the various scenarios.

1Saltus Wealth Index, 2025

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated. The Financial Conduct Authority (FCA) does not regulate Will writing, tax and trust advice and certain forms of estate planning.

Retail sales volumes fell for the eleventh straight month, with weak demand and rising costs pressuring sector confidence

FCA scam reports surged to nearly 5,000 in early 2025, with fraudsters impersonating regulators to steal money

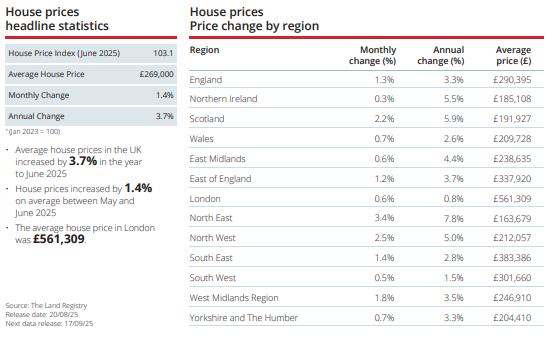

UK house price growth slowed to 2.1% in August, as affordability challenges continue to weigh on buyers

“Retailers endured another tough month in August”

Retail sales volumes fell for the eleventh consecutive month in August, according to the latest survey from the Confederation of British Industry (CBI). The monthly retail sales gauge was at-32%, marking little change from -34% in July. However, the pace of decline is expected to slow down in September, with the outlook improving to -16%.

Retail sales were judged to be ‘poor’ for this time of year (-19%) and are set to remain below the seasonal average this month (-20%). It’s therefore not surprising that sentiment among retailers is low; their business situation is expected to keep deteriorating in the coming quarter (-10%), although not as much as last quarter (-29%).

Retail employment decreased at a steady pace in August (-14%) but is expected to drop further in September at -19%. Average prices increased at the fastest pace since November 2023 (+65%) but this is anticipated to slow to +43% in September.

“Retailers endured another tough month in August” said Martin Sartorious, Principal Economist at CBI. He added, “Weak demand and higher labour costs continue to put pressure on margins, dampening sentiment across the retail and wider distribution sector. This downbeat outlook is reflected in firms’ plans to scale back investment and hiring.”

Fake FCA scams reach nearly 5,000

The Financial Conduct Authority (FCA) received 4,465 reports of fraudsters impersonating the regulator in the first half of 2025, so has advised people to stay vigilant.

According to reports, scammers often encourage people to share sensitive information by claiming that the FCA has recovered funds from a crypto wallet that was opened illegally in their name. Another method targets vulnerable victims, persuading them to hand over funds by claiming that the FCA can help them recover lost money.

Steve Smart at the FCA has reminded consumers, “We will never ask you to transfer money to us or for sensitive banking information such as account PINs and passwords. If in doubt, always check.”

Car production rises but commercial vehicles decline

Figures from the Society of Motor Manufacturers and Traders (SMMT) show that UK car production increased by 5.6% in July, reaching 69,127 units, a second consecutive monthly rise. However, commercial vehicle output dropped significantly (-81.1% year-on-year) following a bumper July in 2024. Overall, total vehicle production was down -10.8% to 72,006 units.

Car sales to the US increased by 6.8%, after three months of decline. SMMT commented on this reversal, ‘The US remains the largest single national market for British built cars, underscoring the importance of the UK-US trade deal and July’s performance illustrates the impact of this deal which came into force on 30 June.’

Savings product choice hits record high

According to a report from Moneyfacts, the number of savings products and savings providers on the market has hit a record high. The quantity of savings deals now stands at 2,274 and there are 154 savings providers to choose from. For the first time since April, average fixed bond and ISA rates are now all below 4%. The Moneyfacts Average Savings Rate decreased to 3.50%, down from 3.92% in August 2024 and 4.14% in 2023.

House prices

The latest figures from Nationwide show that house price growth slowed to 2.1% in August, down from 2.4% in July. This subdued growth is due to persisting affordability challenges, with buyers experiencing difficulties in raising a deposit; house prices are still high in comparison to the typical income. Robert Gardner, Nationwide’s Chief Economist commented, “Affordability should continue to improve gradually if income growth continues to outpace house price growth as we expect. Borrowing costs are likely to moderate a little further if Bank Rate is lowered again in the coming quarters. This should support buyer demand, especially since household balance sheets are strong and labour market conditions are expected to remain solid.”

Here to help

Financial advice is key, so please do not hesitate to get in contact with any questions or concerns you may have

The value of investments can go down as well as up and you may not get back the full amount you invested. The past is not a guide to future performance and past performance may not necessarily be repeated.

All details are correct at time of writing (3 September 2025)

Bank Rate cut to 4% (lowest in over two years) but mortgage rates remain stable

UK house price growth forecast has been lowered to 1% in 2025 as high supply prompts more competitive pricing

Homes gained 20% in value since 2020, with northern regions leading growth while parts of London face declines

Another reduction to Bank Rate

In its August meeting, the Bank of England (BoE) voted to reduce Bank Rate from 4.25% to 4%. This is the fifth cut since August 2024 and the lowest level in over two years.

The decision may have come as a surprise to some, as inflation rose to 3.6% in June and 3.8% in July according to the Office for National Statistics. The BoE expects inflation will increase to around 4% in September (double its target of 2%) but believes that the spike will be temporary.

The reduction in Bank Rate may present opportunities for borrowers on tracker mortgages and those with fixed deals that are coming to an end. However, mortgage rates might not see a significant change. Richard Donnell at Zoopla explained, “The price of fixed rate mortgages already factors in the future path of base rates meaning average mortgage rates are likely to remain broadly where they are today.”

Housing market update

The housing market has had some setbacks this year, but buyer activity is slowly improving.

Savills has revised its forecast for UK house price growth in 2025 from 4% to 1%, following a ‘cautious start to the year and the potential for more buyer jitters in the run up to the Autumn Budget given the state of public finances.’

Housing supply currently remains high, as buyers have the most choice in over 10 years, according to Rightmove. This has prompted sellers to rethink their pricing, with TwentyCi reporting 21% more price adjustments between May and July than the same period last year. As a result of this competitive pricing, sales agreed are up 8% annually according to Zoopla. It will take some time before this improved activity has a knock-on effect on house price growth due to stock being high.

UK homes gain 20% in 5 years

Research from Zoopla has found that the average home has increased in value by 20% since the pandemic, amounting to an average gain of £55,800.

One million homes have increased by 50% or more, gaining £117,400 on average. More than half of these properties can be found in the North West, Wales, and Yorkshire and the Humber. These areas have become more popular among buyers in recent years as they offer more affordable options and are suited to lifestyle changes made since the pandemic.

In more expensive regions, including the south of England, the growth is more modest – half (51%) of properties have increased in value by 20%. Meanwhile, London has experienced difficulties, with 13% of homes dropping in value by 5% or more. Kensington and Chelsea, and Westminster have been the hardest hit, as nearly half of properties in these boroughs are now below their pre-pandemic price.

How’s the Scottish housing market faring?

Data from Registers of Scotland shows that residential transactions increased by 7% annually in Q1 2025, the fourth consecutive quarter of growth.

The rise contributed to higher Land and Buildings Transaction Tax revenue, which the Scottish Government estimated to be £484.7m in 2024/25, up 14.8% on the previous tax year.

According to UK Finance, in 2024/25 the number of mortgages advanced to Scottish first-time buyers (FTBs) increased by 17.0% year-on-year. In Q1, the average loan-to-value ratio was 82.4% for FTBs and 69.6% for home movers.

As for the rental market, data from letting agents shows that there has been a decline in new-let private rental growth in recent years. The annual growth rate recorded in Citylets Rental Index was 4.4% in Q1 2025, significantly lower than the peak of 13.7% in Q3 2023.

All details are correct at the time of writing (20 August 2025)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission