| UK inflation remained at an 18-month high of 3.8% in August, driven by food prices. Above the BoE 2% target | UK GDP growth fell to 0.2% in the three months to July and output failed to grow at all in July | In the UK jobs market payrolls fell for the seventh consecutive month and wage growth slowed to the lowest rate since May 2022 |

Inflation stays at 18-month high

Data released last month by the Office for National Statistics (ONS) showed that a surge in food prices kept the headline rate of inflation at its highest level since January 2024.

The latest official inflation statistics revealed that the Consumer Prices Index (CPI) 12-month rate – which compares prices in the current month with the same period a year earlier – remained unchanged in August at 3.8%. This reading was in line with the consensus view from a Reuters poll of economists.

ONS said inflation across the food and non-alcoholic drinks sector rose for a fifth consecutive month, with prices 5.1% higher than a year earlier, as the cost of beef, butter, milk and chocolate all continued to surge. The increase in food costs, however, was offset by slowing price growth in other areas, most notably air fares.

The latest data leaves inflation significantly above the Bank of England’s 2% target and, a day after release of the consumer price statistics, the Bank’s Monetary Policy Committee (MPC) voted to leave Bank Rate on hold at 4.0%, as analysts had expected.

Speaking after announcing the decision, Bank Governor Andrew Bailey warned that the UK was not yet “out of the woods” when it came to inflation. He also reiterated his view that any future rate cuts would need to be made “gradually and carefully”, adding that, while he did expect further reductions, their timing and scale was now “more uncertain”.

The MPC is due to meet twice more this year, with the next decision scheduled for 6 November. Although a Reuters poll conducted last month did find that a majority of economists do still expect one more rate cut this year, it does increasingly appear to be a close call, with a growing proportion of respondents predicting no further reductions until the first quarter of 2026.

Data points to weaker growth momentum

Official figures published last month revealed a further slowdown in economic output at the outset to the second half of the year, while survey data points to a more recent loss of economic momentum across the private sector.

According to the latest ONS statistics, the UK economy grew by 0.2% during the three months to July. This figure, however, does represent a notable slowdown from a relatively robust first-quarter growth rate of 0.7% and a 0.3% expansion recorded across the second quarter of the year.

The data also revealed that the economy actually failed to grow at all in July. While the services sector did witness some growth, edging up by 0.1% on the month, this was offset by a 1.3% decline in manufacturing output, the sector’s sharpest monthly contraction for a year.

Survey evidence also suggests July’s slowdown is likely to be the start of a more restrained period of growth. Last month’s preliminary headline figure from the closely-monitored S&P Global UK Purchasing Managers’ Index (PMI), for instance, fell to a four-month low of 51.0 in September, down from a final reading of 53.5 in August. While these figures do suggest some expansion in private sector output across both of the final two months of the third quarter, the implied rate of growth is only relatively modest, particularly in relation to September.

Commenting on the findings, S&P Global Market Intelligence’s Chief Business Economist Chris Williamson said the survey brought “a litany of worrying news”, including “weakening growth”. And he added, “Amid talk of further tax rises being needed in the Budget later this year, it’s not surprising to see that business expectations have worsened again in September, and in the absence of an improvement in confidence, it’s unlikely that the economy will make any strong gains in the months ahead.”

Markets

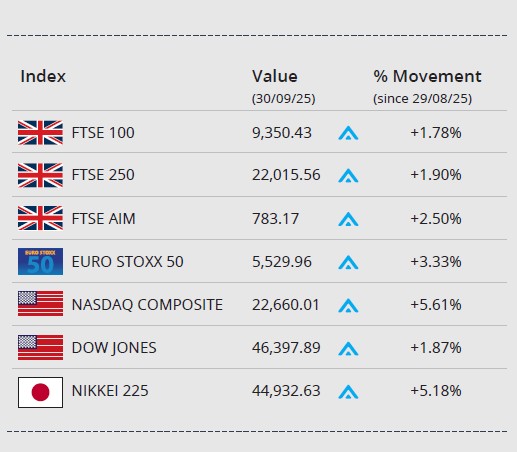

At the end of September, global markets delivered largely positive performances, with equities across major regions advancing and safe-haven assets strengthening. Gains were seen in UK, US, European and Japanese indices, while gold surged and oil prices stalled amid geopolitical tensions.

On home shores, the blue-chip FTSE 100 closed the month on 9,350.43, a gain of 1.78%. The mid-cap FTSE 250 gained 1.90% in September to end on 22,015.56, while the small-cap orientated FTSE AIM registered a 2.50% gain to close September on 783.17.

In the US, the Dow Jones closed the month on 46,397.89, an uptick of 1.87% in the month. The tech-orientated NASDAQ closed the month up 5.61% on 22,660.01, the best third quarter since 2020 and best September performance since 2010. On the continent, the Euro Stoxx 50 gained 3.33% during September to end on 5,529.96. In Japan, the Nikkei 225 gained 5.18% to close the month on 44,932.63.

On the foreign exchanges, the euro closed the month at €1.14 against sterling. The US dollar closed at $1.34 against sterling and at $1.17 against the euro.

The gold price rose 10.30% during September, closing at around $3,870 a troy ounce, as ongoing economic uncertainty and lower interest rates contributed to the safe haven’s latest rally. Brent Crude closed the month at around $66 a barrel, recording no gain on the month. The price faltered at month end as traders continue to worry about oversupply, as well as new developments in the Israel-Gaza conflict.

Jobs market loses a little more steam

The most recent batch of labour market data provided further evidence of a softening in the UK jobs market with the number of workers on firms’ payrolls falling for a seventh consecutive month and pay growth edging lower.

Statistics released last month by ONS showed demand for workers continued to wane over the summer, with the number of payrolled employees in the May – July period 51,000 lower than the level recorded in the previous quarter. Early estimates suggest the number decreased by a further 8,000 in August.

The data release also revealed a slowdown in wage growth with average weekly earning, excluding bonuses, rising at an annual rate of 4.8% in the three months to July, down from 5.0% in the previous three-month period. This represents the slowest rate of pay growth since May 2022.

ONS said its latest set of statistics showed the labour market ‘continues to cool’ with firms noting ‘fewer jobs’ were available. The statistics agency, however, also acknowledged signs that the rate of decline may now ‘be slowing’. For instance, the number of vacancies in the June – August period actually rose slightly from the previous month’s figure, the first increase on this metric since February last year.

August retail sales beat expectations

While survey data released last month continued to highlight a relatively tough retail environment, the latest official statistics did report stronger-than-expected growth in sales volumes.

Figures published recently by ONS showed that total retail sales volumes rose by 0.5% in August. This followed a similar-sized increase in July and was slightly higher than the 0.3% consensus prediction from a Reuters poll of economists. ONS noted that sunny weather had provided a boost to sales during August.

The data, however, also revealed that sales in the three months to August actually declined by 0.1%, compared to levels recorded across the previous three-month period. In addition, evidence from the latest CBI Distributive Trades Survey found that retailers typically judged September’s sales to be ‘poor’ by seasonal norms, while respondents said they expect the situation to worsen in October as weak consumer demand continues to weigh on sales.

Last month’s GfK consumer confidence survey also points to potentially tougher conditions for the retail sector with its headline index falling to -19 in September from -17 in August as all five measures of sentiment dipped. A GfK spokesperson added, “With tax rises expected in the November budget, the risk is that confidence inevitably falls”.

All details are correct at the time of writing (01 October 2025)

It is important to take professional advice before making any decision relating to your personal finances. Information within this document is based on our current understanding and can be subject to change without notice and the accuracy and completeness of the information cannot be guaranteed. It does not provide individual tailored investment advice and is for guidance only. Some rules may vary in different parts of the UK. We cannot assume legal liability for any errors or omissions it might contain. Levels and bases of, and reliefs from, taxation are those currently applying or proposed and are subject to change; their value depends on the individual circumstances of the investor. No part of this document may be reproduced in any manner without prior permission.